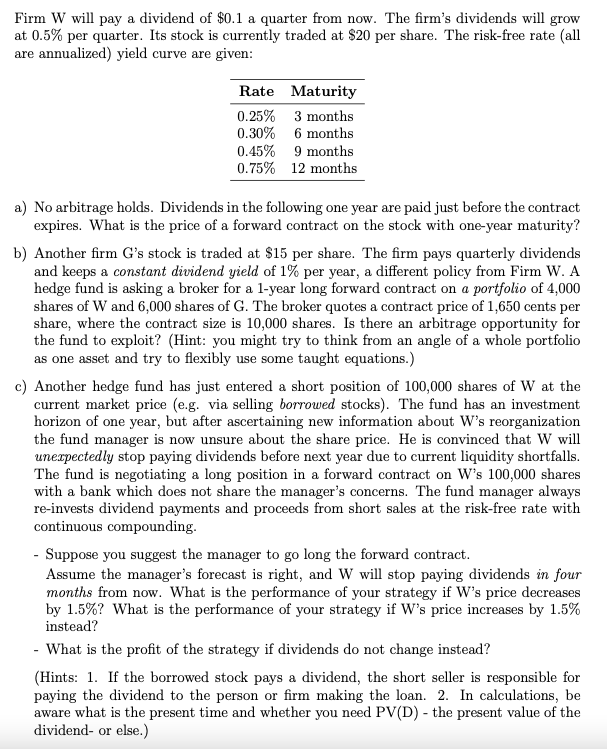

Firm W will pay a dividend of $0.1 a quarter from now. The firm's dividends will...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

a To calculate the price of a forward contract on the stock with oneyear maturity we need to consider the present value of all future dividends and th... View the full answer

Related Book For

Corporate Finance Core Principles And Applications

ISBN: 9781260571127

6th Edition

Authors: Stephen Ross, Randolph Westerfield, Jeffrey Jaffe, Bradford Jordan

Posted Date: