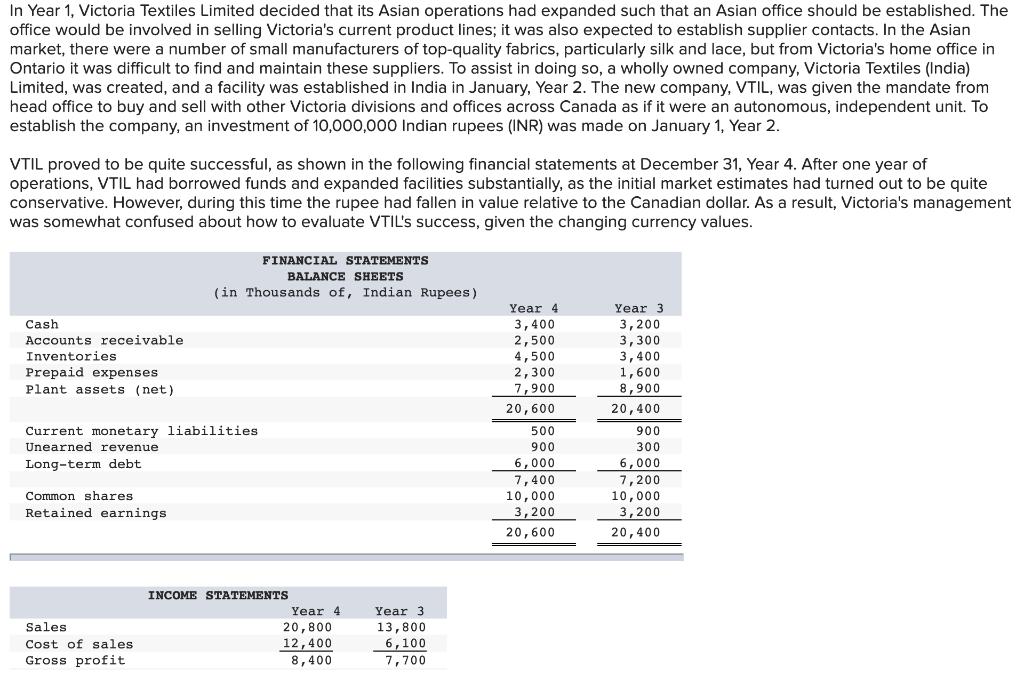

In Year 1, Victoria Textiles Limited decided that its Asian operations had expanded such that an...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

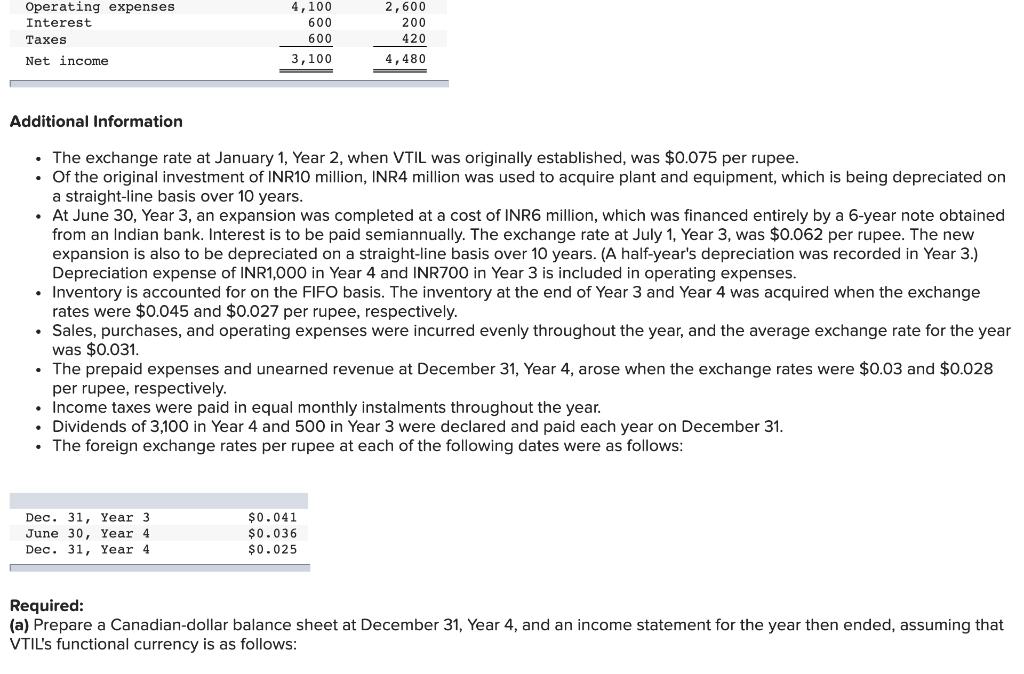

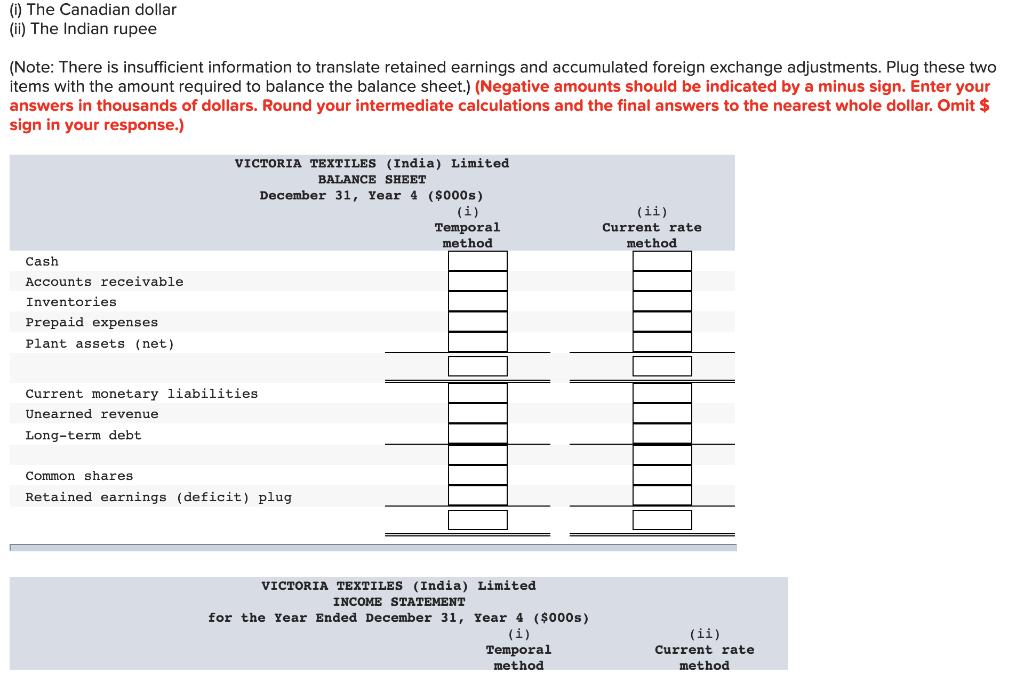

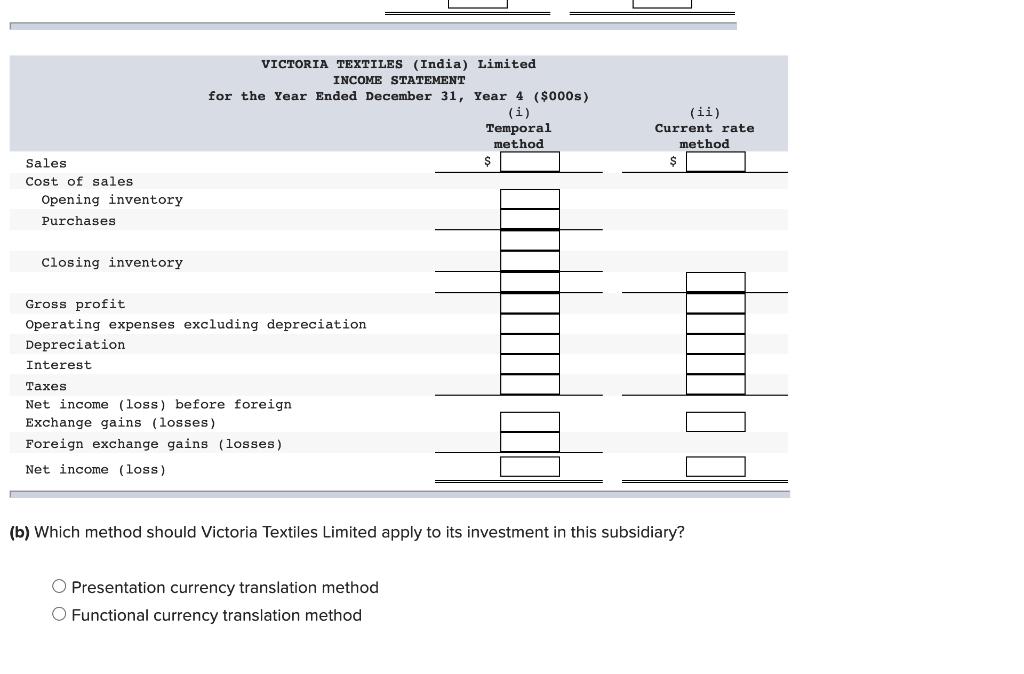

In Year 1, Victoria Textiles Limited decided that its Asian operations had expanded such that an Asian office should be established. The office would be involved in selling Victoria's current product lines; it was also expected to establish supplier contacts. In the Asian market, there were a number of small manufacturers of top-quality fabrics, particularly silk and lace, but from Victoria's home office in Ontario it was difficult to find and maintain these suppliers. To assist in doing so, a wholly owned company, Victoria Textiles (India) Limited, was created, and a facility was established in India in January, Year 2. The new company, VTIL, was given the mandate from head office to buy and sell with other Victoria divisions and offices across Canada as if it were an autonomous, independent unit. To establish the company, an investment of 10,000,000 Indian rupees (INR) was made on January 1, Year 2. VTIL proved to be quite successful, as shown in the following financial statements at December 31, Year 4. After one year of operations, VTIL had borrowed funds and expanded facilities substantially, as the initial market estimates had turned out to be quite conservative. However, during this time the rupee had fallen in value relative to the Canadian dollar. As a result, Victoria's management was somewhat confused about how to evaluate VTIL's success, given the changing currency values. Cash Accounts receivable Inventories Prepaid expenses Plant assets (net) Current monetary liabilities. Unearned revenue Long-term debt. Common shares. Retained earnings. FINANCIAL STATEMENTS BALANCE SHEETS (in Thousands of, Indian Rupees) Sales Cost of sales Gross profit INCOME STATEMENTS Year 4. 20,800 12,400 8,400 Year 3 13,800 6,100 7,700 Year 4 3,400 2,500 4,500 2,300 7,900 20,600 500 900 6,000 7,400 10,000 3,200 20,600 Year 3 3,200 3,300 3,400 1,600 8,900 20,400 900 300 6,000 7,200 10,000 3,200 20,400 Operating expenses. Interest Taxes Net income 4,100 600 600 3,100 Additional Information • The exchange rate at January 1, Year 2, when VTIL was originally established, was $0.075 per rupee. Of the original investment of INR10 million, INR4 million was used to acquire plant and equipment, which is being depreciated on a straight-line basis over 10 years. • At June 30, Year 3, an expansion was completed at a cost of INR6 million, which was financed entirely by a 6-year note obtained from an Indian bank. Interest is to be paid semiannually. The exchange rate at July 1, Year 3, was $0.062 per rupee. The new expansion is also to be depreciated on a straight-line basis over 10 years. (A half-year's depreciation was recorded in Year 3.) Depreciation expense of INR1,000 in Year 4 and INR700 in Year 3 is included in operating expenses. . Inventory is accounted for on the FIFO basis. The inventory at the end of Year 3 and Year 4 was acquired when the exchange rates were $0.045 and $0.027 per rupee, respectively. • Sales, purchases, and operating expenses were incurred evenly throughout the year, and the average exchange rate for the year was $0.031. The prepaid expenses and unearned revenue at December 31, Year 4, arose when the exchange rates were $0.03 and $0.028 per rupee, respectively. 2,600 200 420 4,480 Dec. 31, Year 3 June 30, Year 4 Dec. 31, Year 4. Income taxes were paid in equal monthly instalments throughout the year. • Dividends of 3,100 in Year 4 and 500 in Year 3 were declared and paid each year on December 31. . The foreign exchange rates per rupee at each of the following dates were as follows: $0.041 $0.036 $0.025 Required: (a) Prepare a Canadian-dollar balance sheet at December 31, Year 4, and an income statement for the year then ended, assuming that VTIL's functional currency is as follows: (i) The Canadian dollar (ii) The Indian rupee (Note: There is insufficient information to translate retained earnings and accumulated foreign exchange adjustments. Plug these two items with the amount required to balance the balance sheet.) (Negative amounts should be indicated by a minus sign. Enter your answers in thousands of dollars. Round your intermediate calculations and the final answers to the nearest whole dollar. Omit $ sign in your response.) Cash. Accounts receivable Inventories Prepaid expenses Plant assets (net) VICTORIA TEXTILES (India) Limited BALANCE SHEET December 31, Year 4 ($000s) Current monetary liabilities Unearned revenue Long-term debt Common shares Retained earnings (deficit) plug (i) Temporal method VICTORIA TEXTILES (India) Limited INCOME STATEMENT for the Year Ended December 31, Year 4 ($000s) (i) Temporal method (ii) Current rate. method (ii) Current rate method Sales Cost of sales. Opening inventory Purchases Closing inventory VICTORIA TEXTILES (India) Limited INCOME STATEMENT for the Year Ended December 31, Gross profit Operating expenses excluding depreciation Depreciation Interest Taxes Net income (loss) before foreign Exchange gains (losses) Foreign exchange gains (losses) Net income (loss) Year 4 ($000s) (i) O Presentation currency translation method O Functional currency translation method Temporal method $ (ii) Current rate method $ (b) Which method should Victoria Textiles Limited apply to its investment in this subsidiary? In Year 1, Victoria Textiles Limited decided that its Asian operations had expanded such that an Asian office should be established. The office would be involved in selling Victoria's current product lines; it was also expected to establish supplier contacts. In the Asian market, there were a number of small manufacturers of top-quality fabrics, particularly silk and lace, but from Victoria's home office in Ontario it was difficult to find and maintain these suppliers. To assist in doing so, a wholly owned company, Victoria Textiles (India) Limited, was created, and a facility was established in India in January, Year 2. The new company, VTIL, was given the mandate from head office to buy and sell with other Victoria divisions and offices across Canada as if it were an autonomous, independent unit. To establish the company, an investment of 10,000,000 Indian rupees (INR) was made on January 1, Year 2. VTIL proved to be quite successful, as shown in the following financial statements at December 31, Year 4. After one year of operations, VTIL had borrowed funds and expanded facilities substantially, as the initial market estimates had turned out to be quite conservative. However, during this time the rupee had fallen in value relative to the Canadian dollar. As a result, Victoria's management was somewhat confused about how to evaluate VTIL's success, given the changing currency values. Cash Accounts receivable Inventories Prepaid expenses Plant assets (net) Current monetary liabilities. Unearned revenue Long-term debt. Common shares. Retained earnings. FINANCIAL STATEMENTS BALANCE SHEETS (in Thousands of, Indian Rupees) Sales Cost of sales Gross profit INCOME STATEMENTS Year 4. 20,800 12,400 8,400 Year 3 13,800 6,100 7,700 Year 4 3,400 2,500 4,500 2,300 7,900 20,600 500 900 6,000 7,400 10,000 3,200 20,600 Year 3 3,200 3,300 3,400 1,600 8,900 20,400 900 300 6,000 7,200 10,000 3,200 20,400 Operating expenses. Interest Taxes Net income 4,100 600 600 3,100 Additional Information • The exchange rate at January 1, Year 2, when VTIL was originally established, was $0.075 per rupee. Of the original investment of INR10 million, INR4 million was used to acquire plant and equipment, which is being depreciated on a straight-line basis over 10 years. • At June 30, Year 3, an expansion was completed at a cost of INR6 million, which was financed entirely by a 6-year note obtained from an Indian bank. Interest is to be paid semiannually. The exchange rate at July 1, Year 3, was $0.062 per rupee. The new expansion is also to be depreciated on a straight-line basis over 10 years. (A half-year's depreciation was recorded in Year 3.) Depreciation expense of INR1,000 in Year 4 and INR700 in Year 3 is included in operating expenses. . Inventory is accounted for on the FIFO basis. The inventory at the end of Year 3 and Year 4 was acquired when the exchange rates were $0.045 and $0.027 per rupee, respectively. • Sales, purchases, and operating expenses were incurred evenly throughout the year, and the average exchange rate for the year was $0.031. The prepaid expenses and unearned revenue at December 31, Year 4, arose when the exchange rates were $0.03 and $0.028 per rupee, respectively. 2,600 200 420 4,480 Dec. 31, Year 3 June 30, Year 4 Dec. 31, Year 4. Income taxes were paid in equal monthly instalments throughout the year. • Dividends of 3,100 in Year 4 and 500 in Year 3 were declared and paid each year on December 31. . The foreign exchange rates per rupee at each of the following dates were as follows: $0.041 $0.036 $0.025 Required: (a) Prepare a Canadian-dollar balance sheet at December 31, Year 4, and an income statement for the year then ended, assuming that VTIL's functional currency is as follows: (i) The Canadian dollar (ii) The Indian rupee (Note: There is insufficient information to translate retained earnings and accumulated foreign exchange adjustments. Plug these two items with the amount required to balance the balance sheet.) (Negative amounts should be indicated by a minus sign. Enter your answers in thousands of dollars. Round your intermediate calculations and the final answers to the nearest whole dollar. Omit $ sign in your response.) Cash. Accounts receivable Inventories Prepaid expenses Plant assets (net) VICTORIA TEXTILES (India) Limited BALANCE SHEET December 31, Year 4 ($000s) Current monetary liabilities Unearned revenue Long-term debt Common shares Retained earnings (deficit) plug (i) Temporal method VICTORIA TEXTILES (India) Limited INCOME STATEMENT for the Year Ended December 31, Year 4 ($000s) (i) Temporal method (ii) Current rate. method (ii) Current rate method Sales Cost of sales. Opening inventory Purchases Closing inventory VICTORIA TEXTILES (India) Limited INCOME STATEMENT for the Year Ended December 31, Gross profit Operating expenses excluding depreciation Depreciation Interest Taxes Net income (loss) before foreign Exchange gains (losses) Foreign exchange gains (losses) Net income (loss) Year 4 ($000s) (i) O Presentation currency translation method O Functional currency translation method Temporal method $ (ii) Current rate method $ (b) Which method should Victoria Textiles Limited apply to its investment in this subsidiary?

Expert Answer:

Answer rating: 100% (QA)

a Prepare a Canadiandollar balance sheet at December 31 Year 4 and an income statement for the year then ended assuming that VTILs functional currency ... View the full answer

Posted Date:

Students also viewed these accounting questions

-

In Year 1, Victoria Textiles Limited decided that its Asian operations had expanded such that an Asian office should be established. The office would be involved in selling Victorias current product...

-

In 2007, there were a number of product recalls related to toys and pet foods. Some of these recalls resulted in lawsuits being led against the companies involved. Use the Web to nd three companies...

-

In preparing its consolidated financial statements at December 31, 20X7, the following elimination entries were included in the consolidation worksheet of Master Corporation: Master owns 60 percent...

-

Professor Quark opens his own company, Electronic Tutorial Services, and completes the following transactions in June: 6/1 Quark invests 24,000 into the business. 6/3 Purchased 2,100 of equipment on...

-

Name and describe the major features of a feasibility analysis. Why is feasibility analysis important?

-

The supply curve for product X is given by Qsx = 340 + 10Px. a. Find the inverse supply curve. b. How much surplus do producers receive when Qx = 350? When Qx = 1,000?

-

It has been argued that to be classified as a professional one must offer services to the public rather than simply be an employee of an organization. As such, most employees of an organization,...

-

Differentiate between a two-tier client/server system and a three-tier client/server system. Differentiate between a fat client and a thin client. Why would a firm choose one of these approaches over...

-

1. Develop a forecast with a three-period moving average and a four-period moving average. Identify which method is better by comparing MAD, MSE and MAPE. 2. Develop a forecast with a three-period...

-

Des Moines Power and Light has been collecting data on demand for electric power in its western subregion for only the past 2 years. Those data are shown in the table at the top of the shown below....

-

Assume that you are employed as an international consultant to undertake a private sector assessment of the Pacific Island Country. Select a Pacific Island country for the private sector assessment...

-

Explain the following change management models/theories, how are they similar and different and provide references. 1. Lewin's Change Management Model 2. Kotter's Eight-Step Change Model 3. The Jeff...

-

Social Issue Analysis and Response Final Draft Start Date Due Date Points Apr 17, 2023, 12:00 AM Apr 30, 2023, 11:59 PM 210 Assessment Traits Requires Lopeswrite Assessment Description Honors...

-

How does the data model determine which table is the date table?

-

Distinguish the primary functions of human resource management within the long term care industry. Evaluate the applicable federal and state laws, rules, regulations, and requirements in terms of...

-

Define target market . Define customer value . Write in one paragraph what do you think is the future of Marketing . Provide a marketing mix for a new product and the marketing campaign. Define...

-

5. Find the transfer functions X(s)/U(s) and X2(s)/U(s) for the translational mechanical system shown in Figure 2. X1 X2 k2 k ww 1711 k3 w www my b bi Figure 2

-

The liquidliquid extractor in Figure 8.1 operates at 100F and a nominal pressure of 15 psia. For the feed and solvent flows shown, determine the number of equilibrium stages to extract 99.5% of the...

-

Both the Kremser and Colburn equations have special forms when \(\mathrm{mV} / \mathrm{L}=1.0\). The results of comparing these equations are Eqs. (16-33) and (16-36a), which relate HETP to...

-

How should the leaving chief executive be involved in the succession planning and transition process?

-

What differences distinguish succession planning, chief executive transition, and emergency planning?

Study smarter with the SolutionInn App