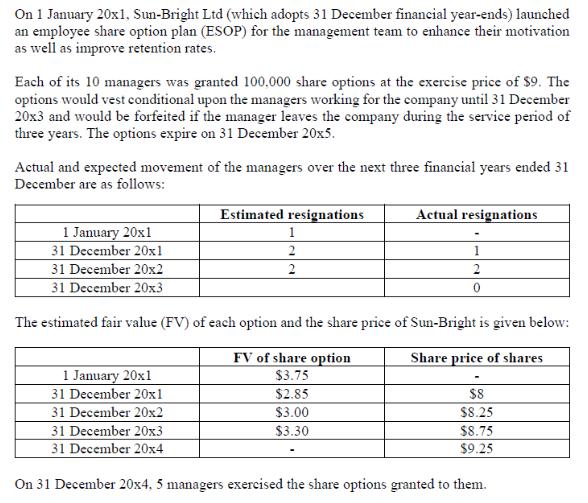

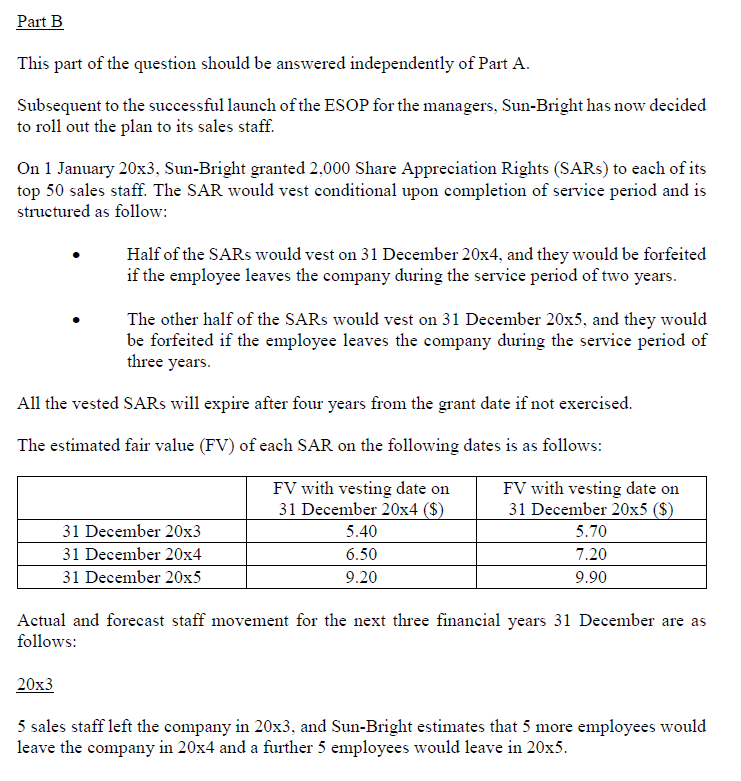

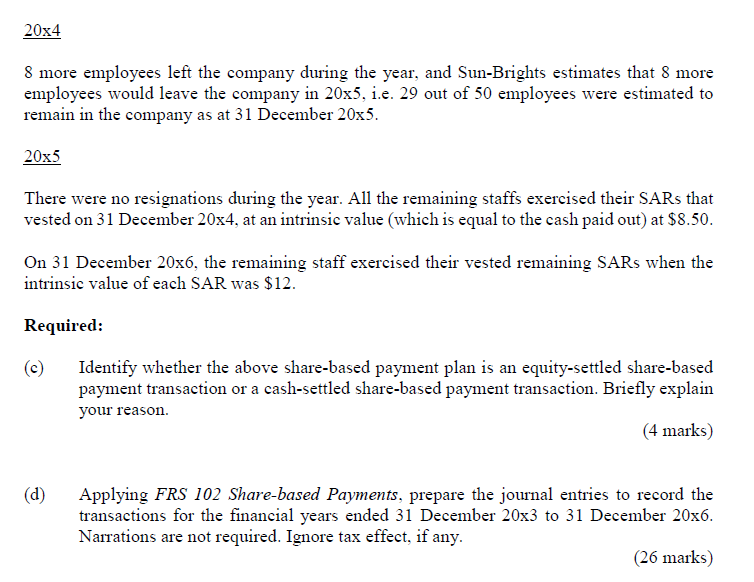

On 1 January 20x1, Sun-Bright Ltd (which adopts 31 December financial year-ends) launched an employee share...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

On 1 January 20x1, Sun-Bright Ltd (which adopts 31 December financial year-ends) launched an employee share option plan (ESOP) for the management team to enhance their motivation as well as improve retention rates. Each of its 10 managers was granted 100.000 share options at the exercise price of $9. The options would vest conditional upon the managers working for the company until 31 December 20x3 and would be forfeited if the manager leaves the company during the service period of three years. The options expire on 31 December 20x5. Actual and expected movement of the managers over the next three financial years ended 31 December are as follows: 1 January 20x1 31 December 20x1 31 December 20x2 Estimated resignations 2 2 Actual resignations 1 2 0 31 December 20x3 The estimated fair value (FV) of each option and the share price of Sun-Bright is given below: 1 January 20x1 31 December 20x1 31 December 20x2 31 December 20x3 FV of share option $3.75 $2.85 $3.00 $3.30 Share price of shares $8 $8.25 $8.75 $9.25 31 December 20x4 On 31 December 20x4, 5 managers exercised the share options granted to them. Required: (a) (b) Applying FRS 102 Share-based Payments, prepare the journal entries to record the transactions from 1 January 20x1 to 31 December 20x4. Narrations are not required. Ignore tax effect, if any. (16 marks) Supposing on 1 January 20x2, the management revised the exercise price of the share option to $8. As a result of this modification, the FV of the modified option on this date was estimated to be $3.25, while the FV of the original option on this date was $2.85 as shown on the table above. Compute the remuneration expense recorded for the years 20x2 and 20x3. (8 marks) Part B This part of the question should be answered independently of Part A. Subsequent to the successful launch of the ESOP for the managers, Sun-Bright has now decided to roll out the plan to its sales staff. On 1 January 20x3, Sun-Bright granted 2,000 Share Appreciation Rights (SARS) to each of its top 50 sales staff. The SAR would vest conditional upon completion of service period and is structured as follow: Half of the SARS would vest on 31 December 20x4, and they would be forfeited if the employee leaves the company during the service period of two years. The other half of the SARS would vest on 31 December 20x5, and they would be forfeited if the employee leaves the company during the service period of three years. All the vested SARs will expire after four years from the grant date if not exercised. The estimated fair value (FV) of each SAR on the following dates is as follows: FV with vesting date on 31 December 20x4 ($) FV with vesting date on 31 December 20x5 ($) 31 December 20x3 31 December 20x4 5.40 6.50 5.70 7.20 9.20 9.90 31 December 20x5 Actual and forecast staff movement for the next three financial years 31 December are as follows: 20x3 5 sales staff left the company in 20x3, and Sun-Bright estimates that 5 more employees would leave the company in 20x4 and a further 5 employees would leave in 20x5. 20x4 8 more employees left the company during the year, and Sun-Brights estimates that 8 more employees would leave the company in 20x5, i.e. 29 out of 50 employees were estimated to remain in the company as at 31 December 20x5. 20x5 There were no resignations during the year. All the remaining staffs exercised their SARs that vested on 31 December 20x4, at an intrinsic value (which is equal to the cash paid out) at $8.50. On 31 December 20x6, the remaining staff exercised their vested remaining SARs when the intrinsic value of each SAR was $12. Required: (c) Identify whether the above share-based payment plan is an equity-settled share-based payment transaction or a cash-settled share-based payment transaction. Briefly explain your reason. (d) (4 marks) Applying FRS 102 Share-based Payments, prepare the journal entries to record the transactions for the financial years ended 31 December 20x3 to 31 December 20x6. Narrations are not required. Ignore tax effect, if any. (26 marks) On 1 January 20x1, Sun-Bright Ltd (which adopts 31 December financial year-ends) launched an employee share option plan (ESOP) for the management team to enhance their motivation as well as improve retention rates. Each of its 10 managers was granted 100.000 share options at the exercise price of $9. The options would vest conditional upon the managers working for the company until 31 December 20x3 and would be forfeited if the manager leaves the company during the service period of three years. The options expire on 31 December 20x5. Actual and expected movement of the managers over the next three financial years ended 31 December are as follows: 1 January 20x1 31 December 20x1 31 December 20x2 Estimated resignations 2 2 Actual resignations 1 2 0 31 December 20x3 The estimated fair value (FV) of each option and the share price of Sun-Bright is given below: 1 January 20x1 31 December 20x1 31 December 20x2 31 December 20x3 FV of share option $3.75 $2.85 $3.00 $3.30 Share price of shares $8 $8.25 $8.75 $9.25 31 December 20x4 On 31 December 20x4, 5 managers exercised the share options granted to them. Required: (a) (b) Applying FRS 102 Share-based Payments, prepare the journal entries to record the transactions from 1 January 20x1 to 31 December 20x4. Narrations are not required. Ignore tax effect, if any. (16 marks) Supposing on 1 January 20x2, the management revised the exercise price of the share option to $8. As a result of this modification, the FV of the modified option on this date was estimated to be $3.25, while the FV of the original option on this date was $2.85 as shown on the table above. Compute the remuneration expense recorded for the years 20x2 and 20x3. (8 marks) Part B This part of the question should be answered independently of Part A. Subsequent to the successful launch of the ESOP for the managers, Sun-Bright has now decided to roll out the plan to its sales staff. On 1 January 20x3, Sun-Bright granted 2,000 Share Appreciation Rights (SARS) to each of its top 50 sales staff. The SAR would vest conditional upon completion of service period and is structured as follow: Half of the SARS would vest on 31 December 20x4, and they would be forfeited if the employee leaves the company during the service period of two years. The other half of the SARS would vest on 31 December 20x5, and they would be forfeited if the employee leaves the company during the service period of three years. All the vested SARs will expire after four years from the grant date if not exercised. The estimated fair value (FV) of each SAR on the following dates is as follows: FV with vesting date on 31 December 20x4 ($) FV with vesting date on 31 December 20x5 ($) 31 December 20x3 31 December 20x4 5.40 6.50 5.70 7.20 9.20 9.90 31 December 20x5 Actual and forecast staff movement for the next three financial years 31 December are as follows: 20x3 5 sales staff left the company in 20x3, and Sun-Bright estimates that 5 more employees would leave the company in 20x4 and a further 5 employees would leave in 20x5. 20x4 8 more employees left the company during the year, and Sun-Brights estimates that 8 more employees would leave the company in 20x5, i.e. 29 out of 50 employees were estimated to remain in the company as at 31 December 20x5. 20x5 There were no resignations during the year. All the remaining staffs exercised their SARs that vested on 31 December 20x4, at an intrinsic value (which is equal to the cash paid out) at $8.50. On 31 December 20x6, the remaining staff exercised their vested remaining SARs when the intrinsic value of each SAR was $12. Required: (c) Identify whether the above share-based payment plan is an equity-settled share-based payment transaction or a cash-settled share-based payment transaction. Briefly explain your reason. (d) (4 marks) Applying FRS 102 Share-based Payments, prepare the journal entries to record the transactions for the financial years ended 31 December 20x3 to 31 December 20x6. Narrations are not required. Ignore tax effect, if any. (26 marks)

Expert Answer:

Related Book For

Intermediate Accounting

ISBN: 978-0324300987

10th Edition

Authors: Loren A Nikolai, D. Bazley and Jefferson P. Jones

Posted Date:

Students also viewed these finance questions

-

Davies Ltd has seen its profit drop considerably over the past few days due to a challenging business environment. In a bid to improve its bottom-line, the companys senior management wants to...

-

Write each number in scientific notation. 0.875

-

How does the learning model by Brock and Hommes explain unexpected price fluctuations?

-

Propose a structure for the compound A (C6H15O2 N) that is unstable in aqueous acid and has the following NMR spectra: 2.30 (6H, s): 2.45 (2H. d,J Hz); 3.27 (6H, s): 4.50 (1 H. t. 6 Hz) 6 Proton...

-

Make a preliminary design for a solar-driven Rankine refrigeration machine to provide the temperature environment required below the surface of a \(20 \times 40 \mathrm{~m}\) iceskating rink that is...

-

Sedona Company set the following standard costs for one unit of its product for 2013. Direct material (20 Ibs. @ $ 2.50 per Ib.) . . . . . . . . . . . . . . . . . . . $ 50.00 Direct labor (10 hrs. @...

-

A university spent $2 million to install solar panels atop a parking garage. These panels will have a capacity of 300 kilowatts (kW) and have a life expectancy of 20 years. Suppose that the discount...

-

Write a paper on Hurricanes in United States explaining the following Explaining the nature (natural science) of this agent (how does a hurricane form, etc.);. How the nature of the agent impacts...

-

In 2022, can Epicurus' simple prescription for happiness work (see DeBotton's article)? Explain why or why not. Make sure to identify his prescription in your answer. Use specific examples.

-

After treatment on a salmon farm, the population of sea lice follows the differential equation P3(t)'=-dp3(t) which has the solution p(t) = Qed where Q and d are positive constants. Using this...

-

Convert the following for loop to a while loop to obtain the same result stored in the variable sum. 1 double sum = 0.0; 2 int threshold = 3; 3 for (double j = 0, k = 0; j

-

Write a method that takes an array of type int and returns a double value. The method returns the average value of the positive elements of the taken array. Output Sample run int[] in = {1, 5, 7, -1,...

-

This case presents an issue that becomes more likely the larger an organization becomes. The legal department of any company is an important part of the organization. The laws and regulations...

-

Task 1: Search the Internet for IT governance planning. Select a specific governance plan that exists at a company or a plan framework from an organization. Write a paper on three or four of the most...

-

Consider the circuit of Fig. 7.97. Find v0 (t) if i(0) = 2 A and v(t) = 0. 1 3 ett)

-

The y-intercept b0 of a least-squares regression line has a useful interpretation only if the x-values are either all positive or all negative. In Exercises 812, determine whether the statement is...

-

In general, the slope of the least-squares regression line is equal to the correlation coefficient. In Exercises 812, determine whether the statement is true or false. If the statement is false,...

-

At the final exam in a statistics class, the professor asks each student to indicate how many hours he or she studied for the exam. After grading the exam, the professor computes the least-squares...

Study smarter with the SolutionInn App