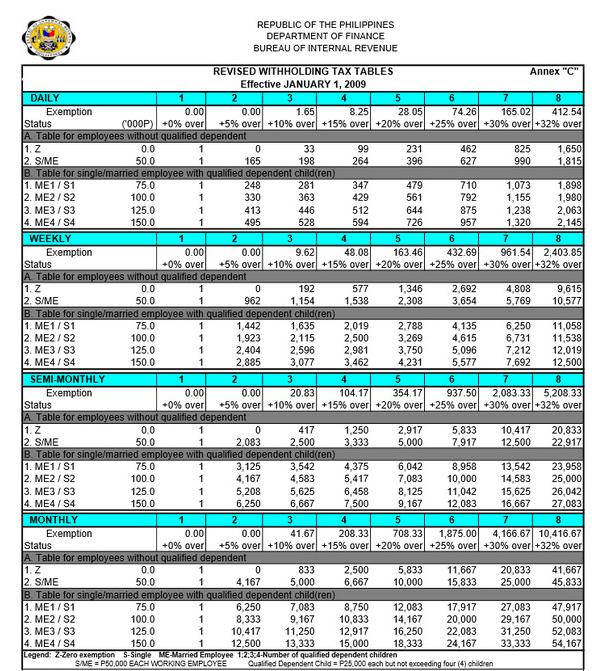

Refer to the BIR tax table. Determine the withholding income tax deduction for each employee below: a.

Fantastic news! We've Found the answer you've been seeking!

Question:

Refer to the BIR tax table. Determine the withholding income tax deduction for each employee below:

a. Julie Perez is a regular employee with a monthly compensation amounting to P27,554 and with total statutory deductions of P1,439.15

b. Marlex Baron is a marketer in a beauty company receiving a total of P30,000 a month with statutory deduction of P1,506.30. Ms. Baron also received a commission income amounting to P5,500 for the month.

Expert Answer:

To determine the withholding income tax deduction for each employee well need to follow the BIR tax ... View the full answer

Related Book For

Income Tax Fundamentals 2013

ISBN: 9781285586618

31st Edition

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

Posted Date: