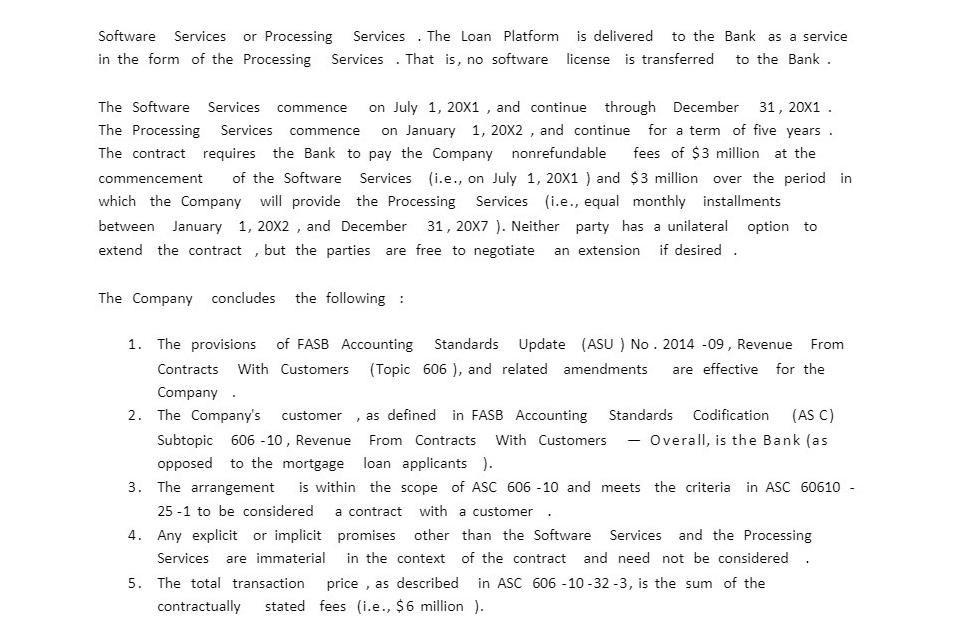

Software Services or Processing Services The Loan Platform is delivered to the Bank as a service...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Step 12 1 Do the software services constitute a performance obligation as defined in both ASC 606 an... View the full answer

Related Book For

Income Tax Fundamentals 2013

ISBN: 9781285586618

31st Edition

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

Posted Date: