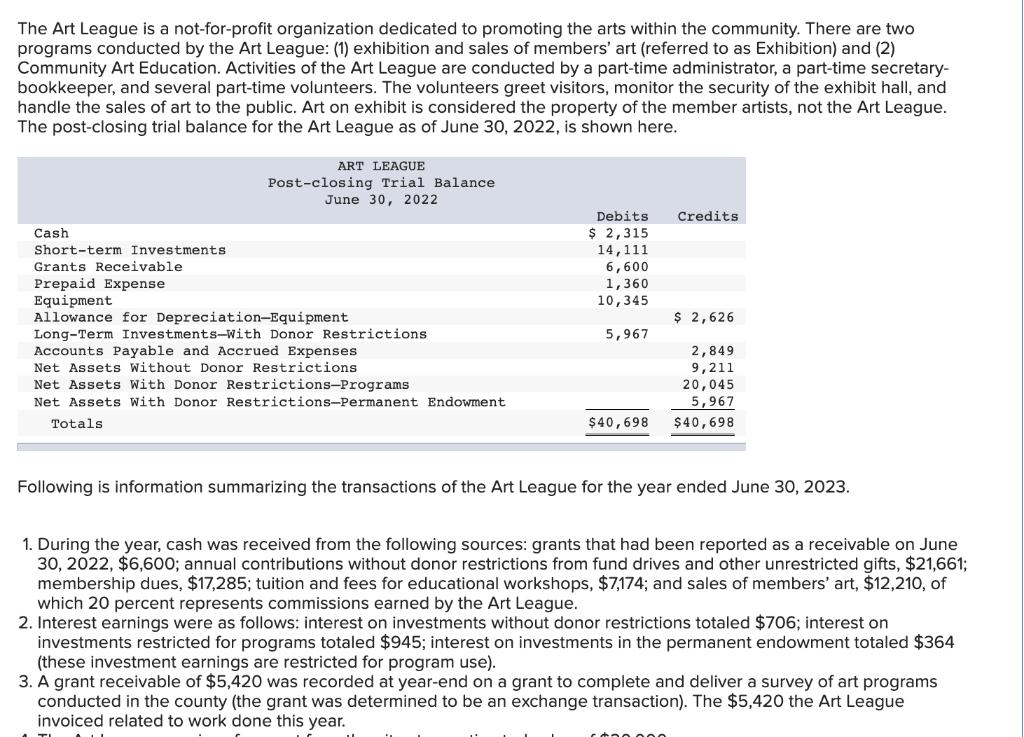

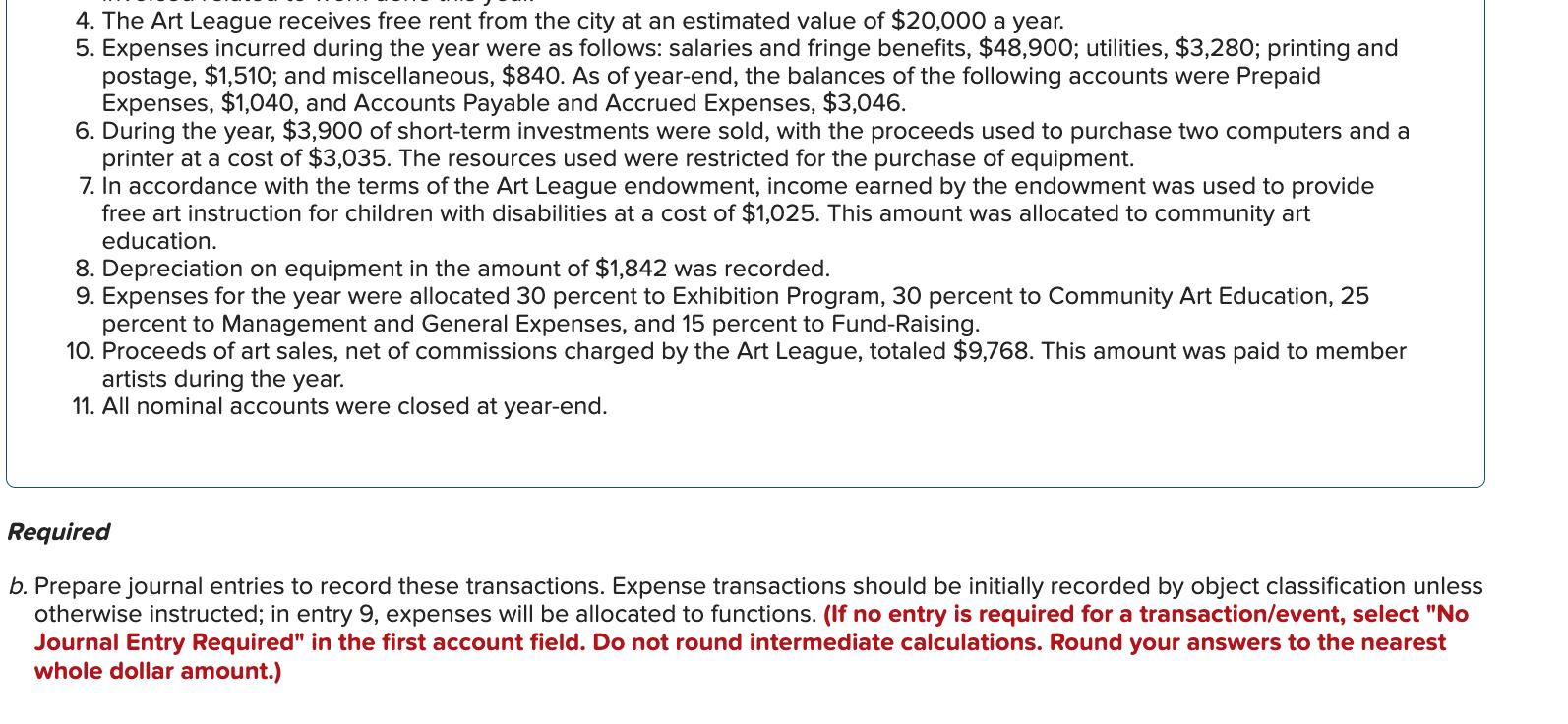

The Art League is a not-for-profit organization dedicated to promoting the arts within the community. There...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

The Art League is a not-for-profit organization dedicated to promoting the arts within the community. There are two programs conducted by the Art League: (1) exhibition and sales of members' art (referred to as Exhibition) and (2) Community Art Education. Activities of the Art League are conducted by a part-time administrator, a part-time secretary- bookkeeper, and several part-time volunteers. The volunteers greet visitors, monitor the security of the exhibit hall, and handle the sales of art to the public. Art on exhibit is considered the property of the member artists, not the Art League. The post-closing trial balance for the Art League as of June 30, 2022, is shown here. ART LEAGUE Post-closing Trial Balance June 30, 2022 Cash Short-term Investments Grants Receivable Prepaid Expense Equipment Allowance for Depreciation-Equipment Long-Term Investments-With Donor Restrictions Accounts Payable and Accrued Expenses Net Assets Without Donor Restrictions Net Assets With Donor Restrictions-Programs Net Assets With Donor Restrictions-Permanent Endowment Totals Debits $ 2,315 14,111 6,600 1,360 10,345 5,967 $40,698 Credits $ 2,626 600.000 2,849 9,211 20,045 5,967 $40,698 Following is information summarizing the transactions of the Art League for the year ended June 30, 2023. 1. During the year, cash was received from the following sources: grants that had been reported as a receivable on June 30, 2022, $6,600; annual contributions without donor restrictions from fund drives and other unrestricted gifts, $21,661; membership dues, $17,285; tuition and fees for educational workshops, $7,174; and sales of members' art, $12,210, of which 20 percent represents commissions earned by the Art League. 2. Interest earnings were as follows: interest on investments without donor restrictions totaled $706; interest on investments restricted for programs totaled $945; interest on investments in the permanent endowment totaled $364 (these investment earnings are restricted for program use). 3. A grant receivable of $5,420 was recorded at year-end on a grant to complete and deliver a survey of art programs conducted in the county (the grant was determined to be an exchange transaction). The $5,420 the Art League invoiced related to work done this year. 4. The Art League receives free rent from the city at an estimated value of $20,000 a year. 5. Expenses incurred during the year were as follows: salaries and fringe benefits, $48,900; utilities, $3,280; printing and postage, $1,510; and miscellaneous, $840. As of year-end, the balances of the following accounts were Prepaid Expenses, $1,040, and Accounts Payable and Accrued Expenses, $3,046. 6. During the year, $3,900 of short-term investments were sold, with the proceeds used to purchase two computers and a printer at a cost of $3,035. The resources used were restricted for the purchase of equipment. 7. In accordance with the terms of the Art League endowment, income earned by the endowment was used to provide free art instruction for children with disabilities at a cost of $1,025. This amount was allocated to community art education. 8. Depreciation on equipment in the amount of $1,842 was recorded. 9. Expenses for the year were allocated 30 percent to Exhibition Program, 30 percent to Community Art Education, 25 percent to Management and General Expenses, and 15 percent to Fund-Raising. 10. Proceeds of art sales, net of commissions charged by the Art League, totaled $9,768. This amount was paid to member artists during the year. 11. All nominal accounts were closed at year-end. Required b. Prepare journal entries to record these transactions. Expense transactions should be initially recorded by object classification unless otherwise instructed; in entry 9, expenses will be allocated to functions. (If no entry is required for a transaction/event, select "No Journal Entry Required" in the first account field. Do not round intermediate calculations. Round your answers to the nearest whole dollar amount.) A. Record the cash received from grant receivable, annual contribution, membership dues, tuition and fees, and sales of art. B. Record the interest on investment income received during the year. C. Record the $5,420 grant receivable at year-end to complete and deliver a survey of art programs conducted in the county. D. The Art League receives free rent from the city at an estimated value of a year. Record the transaction. Record the $20,000 free rent received from the city. E. Record the expenses incurred during the year. F. Record the sale of short-term investments made during the year. G. Record the purchase of equipment. H. Record the necessary adjustment in the net assets account for the purchase of equipment. 1. Record the payment made for free art education. J. Record the necessary adjustment in the net assets account for art education. K. Record the depreciation on equipment. L. Record the expenses for the year of which 30 percent allocated to Exhibition Program; 30 percent to Community Art Education; 25 percent to Management and General Expenses; and 15 percent to Fund- Raising. M. Record the $9,768 proceeds of art sales, net of commissions charged by the Art League. This amount was paid to member artists during the year. N. Record the closure of all nominal accounts without donor restrictions at year-end. O. Record the closure of investment income at the year-end. P. Record the reclassifications for net assets with donor restrictions released. Q. Record the reclassifications for net assets without donor restrictions released. The Art League is a not-for-profit organization dedicated to promoting the arts within the community. There are two programs conducted by the Art League: (1) exhibition and sales of members' art (referred to as Exhibition) and (2) Community Art Education. Activities of the Art League are conducted by a part-time administrator, a part-time secretary- bookkeeper, and several part-time volunteers. The volunteers greet visitors, monitor the security of the exhibit hall, and handle the sales of art to the public. Art on exhibit is considered the property of the member artists, not the Art League. The post-closing trial balance for the Art League as of June 30, 2022, is shown here. ART LEAGUE Post-closing Trial Balance June 30, 2022 Cash Short-term Investments Grants Receivable Prepaid Expense Equipment Allowance for Depreciation-Equipment Long-Term Investments-With Donor Restrictions Accounts Payable and Accrued Expenses Net Assets Without Donor Restrictions Net Assets With Donor Restrictions-Programs Net Assets With Donor Restrictions-Permanent Endowment Totals Debits $ 2,315 14,111 6,600 1,360 10,345 5,967 $40,698 Credits $ 2,626 600.000 2,849 9,211 20,045 5,967 $40,698 Following is information summarizing the transactions of the Art League for the year ended June 30, 2023. 1. During the year, cash was received from the following sources: grants that had been reported as a receivable on June 30, 2022, $6,600; annual contributions without donor restrictions from fund drives and other unrestricted gifts, $21,661; membership dues, $17,285; tuition and fees for educational workshops, $7,174; and sales of members' art, $12,210, of which 20 percent represents commissions earned by the Art League. 2. Interest earnings were as follows: interest on investments without donor restrictions totaled $706; interest on investments restricted for programs totaled $945; interest on investments in the permanent endowment totaled $364 (these investment earnings are restricted for program use). 3. A grant receivable of $5,420 was recorded at year-end on a grant to complete and deliver a survey of art programs conducted in the county (the grant was determined to be an exchange transaction). The $5,420 the Art League invoiced related to work done this year. 4. The Art League receives free rent from the city at an estimated value of $20,000 a year. 5. Expenses incurred during the year were as follows: salaries and fringe benefits, $48,900; utilities, $3,280; printing and postage, $1,510; and miscellaneous, $840. As of year-end, the balances of the following accounts were Prepaid Expenses, $1,040, and Accounts Payable and Accrued Expenses, $3,046. 6. During the year, $3,900 of short-term investments were sold, with the proceeds used to purchase two computers and a printer at a cost of $3,035. The resources used were restricted for the purchase of equipment. 7. In accordance with the terms of the Art League endowment, income earned by the endowment was used to provide free art instruction for children with disabilities at a cost of $1,025. This amount was allocated to community art education. 8. Depreciation on equipment in the amount of $1,842 was recorded. 9. Expenses for the year were allocated 30 percent to Exhibition Program, 30 percent to Community Art Education, 25 percent to Management and General Expenses, and 15 percent to Fund-Raising. 10. Proceeds of art sales, net of commissions charged by the Art League, totaled $9,768. This amount was paid to member artists during the year. 11. All nominal accounts were closed at year-end. Required b. Prepare journal entries to record these transactions. Expense transactions should be initially recorded by object classification unless otherwise instructed; in entry 9, expenses will be allocated to functions. (If no entry is required for a transaction/event, select "No Journal Entry Required" in the first account field. Do not round intermediate calculations. Round your answers to the nearest whole dollar amount.) A. Record the cash received from grant receivable, annual contribution, membership dues, tuition and fees, and sales of art. B. Record the interest on investment income received during the year. C. Record the $5,420 grant receivable at year-end to complete and deliver a survey of art programs conducted in the county. D. The Art League receives free rent from the city at an estimated value of a year. Record the transaction. Record the $20,000 free rent received from the city. E. Record the expenses incurred during the year. F. Record the sale of short-term investments made during the year. G. Record the purchase of equipment. H. Record the necessary adjustment in the net assets account for the purchase of equipment. 1. Record the payment made for free art education. J. Record the necessary adjustment in the net assets account for art education. K. Record the depreciation on equipment. L. Record the expenses for the year of which 30 percent allocated to Exhibition Program; 30 percent to Community Art Education; 25 percent to Management and General Expenses; and 15 percent to Fund- Raising. M. Record the $9,768 proceeds of art sales, net of commissions charged by the Art League. This amount was paid to member artists during the year. N. Record the closure of all nominal accounts without donor restrictions at year-end. O. Record the closure of investment income at the year-end. P. Record the reclassifications for net assets with donor restrictions released. Q. Record the reclassifications for net assets without donor restrictions released.

Expert Answer:

Answer rating: 100% (QA)

Journal NO ACCOUNT TITLES DEBIT CREDIT 1 CASH 60730 CONTRIBUTIONSUNRESTRICTED 700013861 20861 GRANTS RECEIVABLE 4600 MEMBERSHIP DUES 16285 TUITION FEE... View the full answer

Related Book For

Accounting for Governmental and Nonprofit Entities

ISBN: 978-1259917059

18th edition

Authors: Jacqueline L. Reck, James E. Rooks, Suzanne Lowensohn, Daniel Neely

Posted Date:

Students also viewed these accounting questions

-

The Art League is a not-for-profit organization dedicated to promoting the arts within the community. There are two programs conducted by the Art League: (1) exhibition and sales of members art...

-

The Art League is a not-for-profit organization dedicated to promoting the arts within the community. There are two programs conducted by the Art League: (1) exhibition and sales of members art...

-

The Art League is a not-for-profit organization dedicated to promoting the arts within the community. There are two programs conducted by the Art League: (1) exhibition and sales of members art...

-

A certain radioactive isotope is a by - product of some nuclear reactors. Due to an explosion, a nuclear reactor experiences a massive leak of this radioactive isotope. Fortunately, the isotope has a...

-

Management often disagrees with the use of seniority to determine promotion decision. Under what circumstances might an employer bypass a senior employee and promote a junior employee? Is this a fair...

-

Describe the location and structure of the pituitary gland.

-

Compute the missing amount for Jones Corporation. You will need to work through total stockholders equity. Requirements 1. Did Jones earn a net income or suffer a net loss for the year ? Compute the...

-

Cash flows during the first year of operations for the Harman-Kardon Consulting Company were as follows: Cash collected from customers, $340,000; Cash paid for rent, $40,000; Cash paid to employees...

-

Review the Competency 2 Resources: The Roles of Government in the Economy . Analyze 1 of the following government intervention programs: U.S. agriculture support programs Assistance for low Income...

-

Ginger Company of Bathurst has a policy of depositing all receipts and making all payments by cheque. On receiving the bank statement, Bill Free, a new bookkeeper, is quite upset that the balance in...

-

Elon Dust started a company called Busla Corporation on January 2, 2018. The annual reporting period ends on December 31", 2018. During the year 2018 the following transactions have occurred: (a) On...

-

Discuss the potential security risks associated with storing and processing sensitive data within a GBMS .?

-

Suppose you were long in a T-bond futures contract at 94-16. At the futures expiration for a delivered T- bond, if the bond's conversion factor was 1.1 and the accrued interests on the deliverable...

-

The Platter Valley factory of Bybee Industries manufactures field boots. The cost of each boot includes direct materials, direct labor, and manufacturing ( factory ) overhead. The firm traces all...

-

Hunter, Inc. analyzed its accounts receivable balances at December 3 1 , and arrived at the aged balances listed below, along with the percentage that is estimated to be uncollectible: % Considered...

-

12. A 50.0 mL sample of saltwater that is 3.0% m/v is diluted to 950 mL. What is its final mass/volume percent?

-

Suppose Procter & Gamble sells 20 million bars of soap per week, but the demand is not constant and production management would like to get a better handle on how sales are distributed over the year....

-

In the operation of an automated production line with storage buffers, what does it mean if a buffer is nearly always empty or nearly always full?

-

Explain the difference between a CAFR and general purpose external financial reports.

-

Residents of Green Acres, a gated community located in the City of Foothills, voted to form a local improvement district to fund the construction of a neighborhood park. The city agreed to administer...

-

Go to the Internet websites of any five of the charitable organizations listed in Illustration 138 and search for financial information and performance measures they may disclose on their websites....

-

The fly balls of spring loaded governor of Hartnell type running at 600 rpm have a radius of rotation of 80 mm with sleeve in mid-position and ball arms vertical. The ball arms and sleeve arms are of...

-

The height of Watt's governor is proportional to (a) speed (N) (b) \(\mathrm{N}^{2}\) (c) \(1 / \mathrm{N}\) (d) \(1 / \mathrm{N}^{2}\).

-

What is the main function of a governor? How does it differ from that of a flywheel?

Study smarter with the SolutionInn App