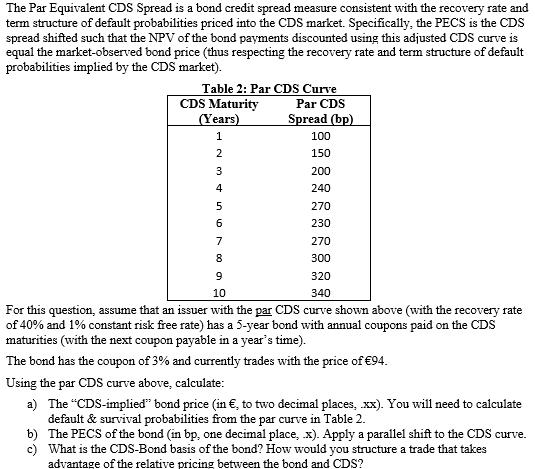

The Par Equivalent CDS Spread is a bond credit spread measure consistent with the recovery rate...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

a To calculate the CDSimplied bond price we need to discount the bonds cash flows using the default ... View the full answer

Related Book For

Financial Institutions Management A Risk Management Approach

ISBN: 978-0071051590

8th edition

Authors: Marcia Cornett, Patricia McGraw, Anthony Saunders

Posted Date: