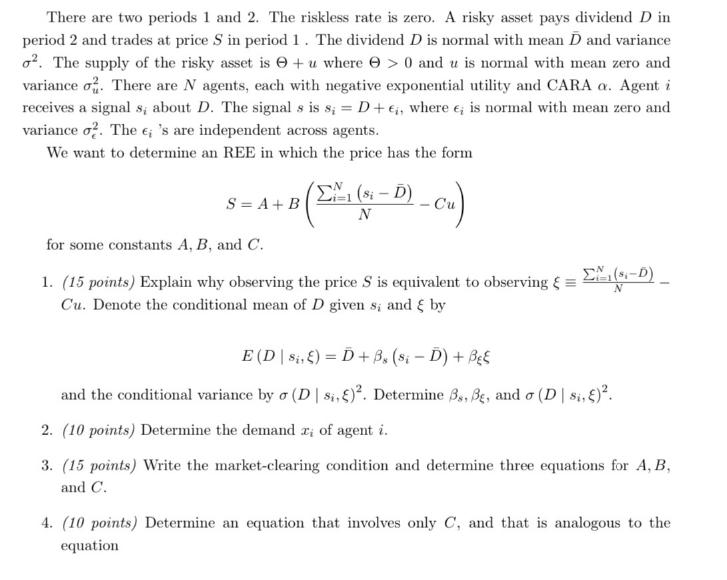

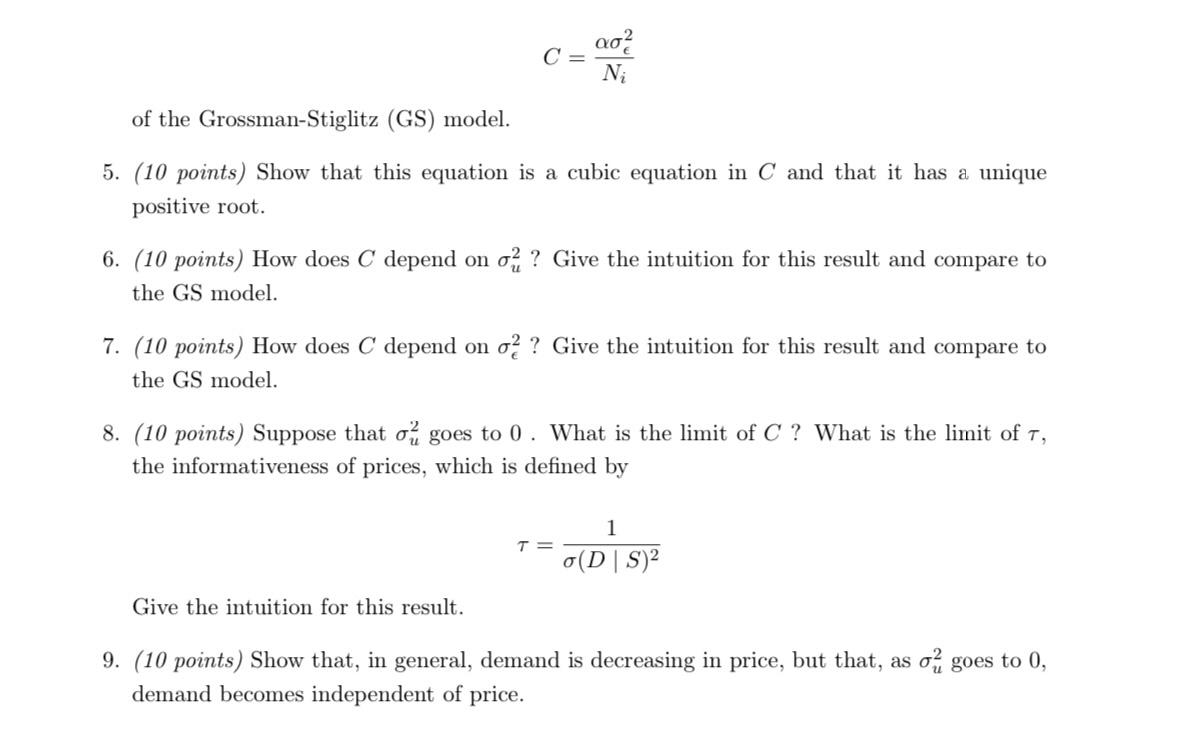

There are two periods 1 and 2. The riskless rate is zero. A risky asset pays...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

ANSWER Question 1 Observing the price S is equivalent to observing xiequivfracsumi1NsioverlineDNCu because the price S is a function of the signals sigmai and the noise u Specifically the price S is g... View the full answer

Related Book For

Industrial Organization Markets and Strategies

ISBN: 978-1107069978

2nd edition

Authors: Paul Belleflamme, Martin Peitz

Posted Date: