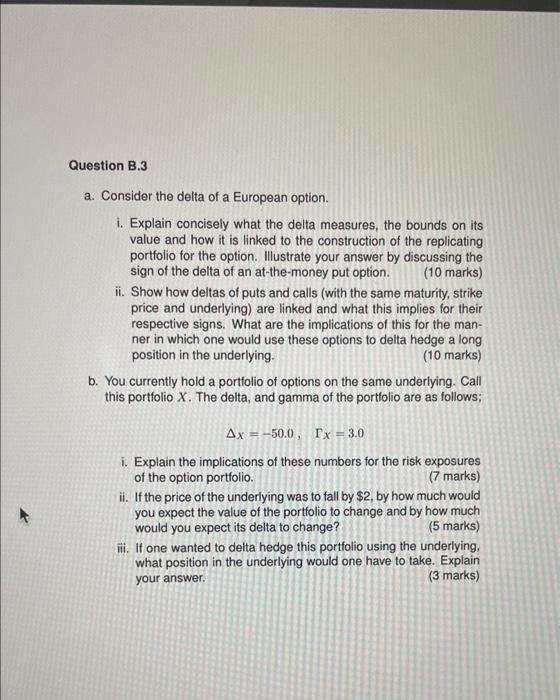

Question B.3 a. Consider the delta of a European option. i. Explain concisely what the delta...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

given a i The delta of a European option is the rate of change of the option price with respect to t... View the full answer

Related Book For

Posted Date: