Use the following information to answer question. You are given the following return information for 3-month T-bills,

Question:

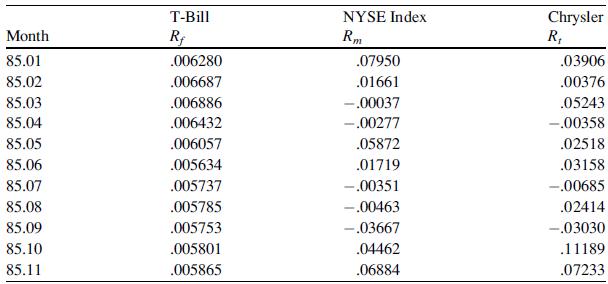

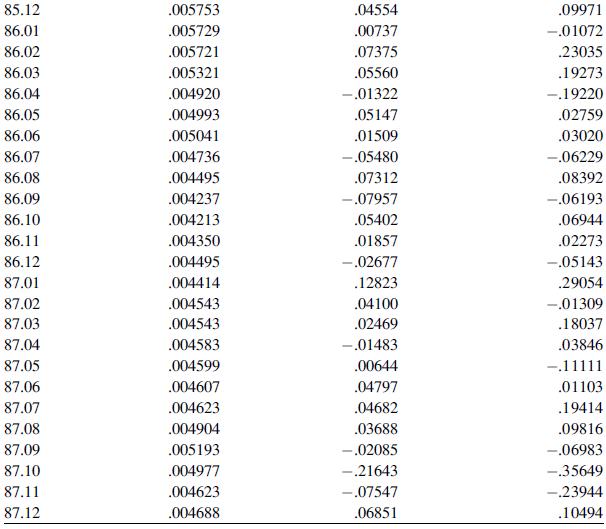

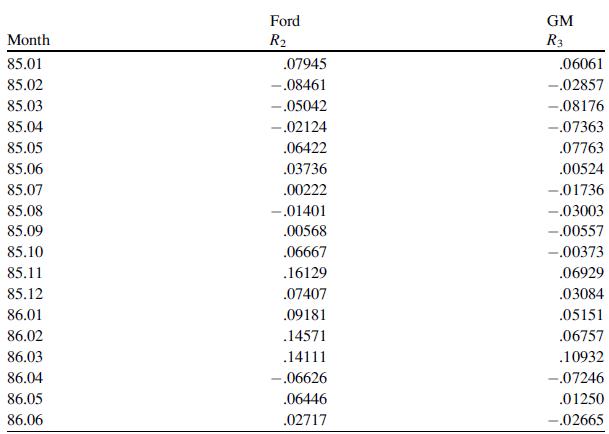

Use the following information to answer question. You are given the following return information for 3-month T-bills, the NYSE Index, Chrysler, Ford, and GM for the 3-year period from January 1985 through December 1987.

Compare the two methods you used for forecasting in questions 34–41. Is one method superior to the other in all cases?

Question 34

Use MINITAB to plot the return data for T-bills against time. (Let t = 1 be the first month.) Can you identify any of the components of the time series?

Question 35

Compute a simple 3-period moving average for the return on T-bills. Forecast the value for January 1988 using this method.

Question 36

With the MINITAB program, use an AR(1) model to describe the time-series behavior of T-bills. Forecast the value for January 1988 using the AR(1)

procedure.

Question 37

Using only data from January 1985 through November 1987, forecast the value for December 1987, using both the 3-period moving average and the AR(1)

model. Compare your results. Which model forecasts better?

Question 38

Repeat question 37 using the data for the NYSE index.

Question 39

Repeat question 37 using the data for Chrysler.

Question 40

Repeat question 37 using the data for Ford.

Question 41

Repeat question 37 using the data for GM.

Step by Step Answer:

This question has not been answered yet.

You can Ask your question!

Statistics For Business And Financial Economics

ISBN: 9781461458975

3rd Edition

Authors: Cheng Few Lee , John C Lee , Alice C Lee