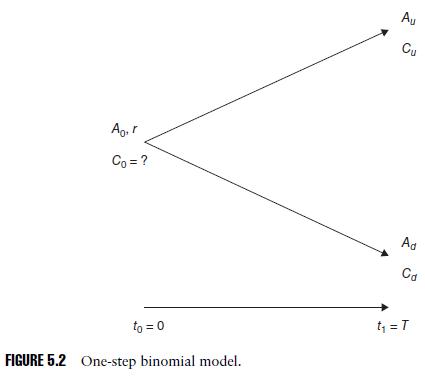

In the 1-step binomial model shown in Figure 5.2, consider the portfolio consisting of one long position

Question:

In the 1-step binomial model shown in Figure 5.2, consider the portfolio consisting of one long position in the contingent claim and short

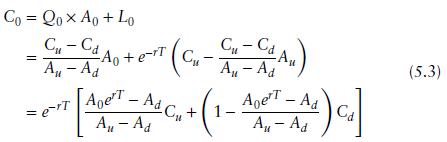

\[Q_{0}=\left(C_{u}-C_{d}ight) /\left(A_{u}-A_{d}ight)\]

of the asset, \(P=C-Q_{0} A\).

(a) Show that the portfolio has the same value at \(t_{1}=T\) regardless of the terminal state \(A_{u}, A_{d}\), that is \(P\left(t_{1}ight)=P_{1}\) for a constant \(P_{1}\) and the portfolio is risk-less.

(b) Using an arbitrage argument, show that today's value of the portfolio should be its discounted future value

\[P_{0}=C_{0}-Q_{0} A_{0}=e^{-r T} P_{1}\]

and compute \(C_{0}\).

(c) Show that the computed value of \(C_{0}\) above is the same as Formula 5.3.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

ANDREW KIPRUTO

Academic Writing Expert

I have over 7 years of research and application experience. I am trained and licensed to provide expertise in IT information, computer sciences related topics and other units like chemistry, Business, law, biology, biochemistry, and genetics. I'm a network and IT admin with +8 years of experience in all kind of environments.

I can help you in the following areas:

Networking

- Ethernet, Wireless Airmax and 802.11, fiber networks on GPON/GEPON and WDM

- Protocols and IP Services: VLANs, LACP, ACLs, VPNs, OSPF, BGP, RADIUS, PPPoE, DNS, Proxies, SNMP

- Vendors: MikroTik, Ubiquiti, Cisco, Juniper, HP, Dell, DrayTek, SMC, Zyxel, Furukawa Electric, and many more

- Monitoring Systems: PRTG, Zabbix, Whatsup Gold, TheDude, RRDtoo

Always available for new projects! Contact me for any inquiries

1+ Reviews

10+ Question Solved

Related Book For

Mathematical Techniques In Finance An Introduction Wiley Finance

ISBN: 9781119838401

1st Edition

Authors: Amir Sadr

Question Posted: