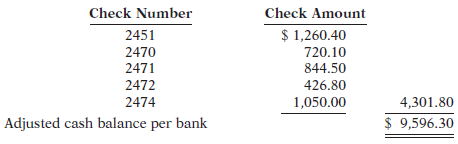

The bank portion of the bank reconciliation for Hunsaker Company at October 31, 2010, is shown below.

Question:

The bank portion of the bank reconciliation for Hunsaker Company at October 31, 2010, is shown below.

HUNSAKER COMPANY

Bank Reconciliation

October 31, 2010

Cash balance per bank …………………………. $12,367.90

Add: Deposits in transit …………………………… 1,530.20

13,898.10

Less: Outstanding checks

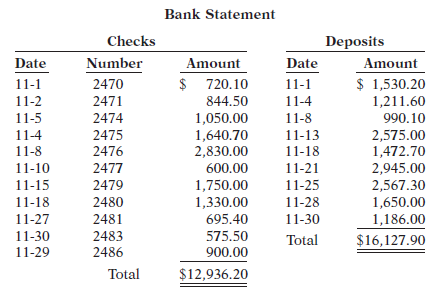

The adjusted cash balance per bank agreed with the cash balance per books at October 31. The November bank statement showed the following checks and deposits.

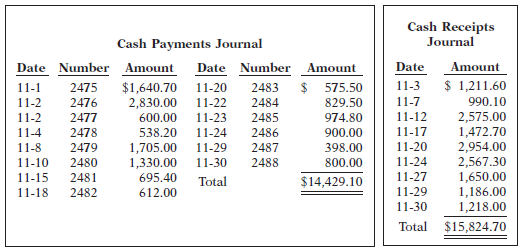

The cash records per books for November showed the following.

The bank statement contained two bank memoranda:

1. A credit of $2,242 for the collection of a $2,100 note for Hunsaker Company plus interest of $157 and less a collection fee of $15. Hunsaker Company has not accrued any interest on the note.

2. A debit for the printing of additional company checks $85.

At November 30 the cash balance per books was $10,991.90 and the cash balance per bank statement was $17,716.60. The bank did not make any errors, but Hunsaker Company made two errors.

Instructions

(a) Using the four steps in the reconciliation procedure describe below, prepare a bank reconciliation at November 30, 2010.

Step 1. Deposits in transit. Compare the individual deposits on the bank statement with the deposits in transit from the preceding bank reconciliation and with the deposits per company records or copies of duplicate deposit slips. Deposits recorded by the depositor that have not been recorded by the bank represent deposits in transit. Add these deposits to the balance per bank.

Step 2. Outstanding checks. Compare the paid checks shown on the bank statement or the paid checks returned with the bank statement with (a) checks outstanding from the preceding bank reconciliation, and (b) checks issued by the company as recorded in the cash payments journal. Issued checks recorded by the company that have not been paid by the bank represent outstanding checks. Deduct outstanding checks from the balance per the bank.

Step 3. Errors. Note any errors discovered in the previous steps and list them in the appropriate section of the reconciliation schedule. For example, if the company mistakenly recorded as $159 a paid check correctly written for $195, the company would deduct the error of $36 from the balance per books. All errors made by the depositor are reconciling items in determining the adjusted cash balance per books. In contrast, all errors made by the bank are reconciling items in determining the adjusted cash balance per the bank.

Step 4. Bank memoranda. Trace bank memoranda to the depositor’s records. The company lists in the appropriate section of the reconciliation schedule any unrecorded memoranda. For example, the company would deduct from the balance per books a $5 debit memorandum for bank service charges. Similarly, it would add to the balance per books a $32 credit memorandum for interest earned.

(b) Prepare the adjusting entries based on the reconciliation. (Note: The correction of any errors pertaining to recording checks should be made to Accounts Payable. The correction of any errors relating to recording cash receipts should be made to Accounts Receivable.)

Step by Step Answer:

a HUNSAKER COMPANY Bank Reconciliation November 30 2010 Balance per bank statement 1771660 Add Depos...View the full answer

Financial Accounting Tools for Business Decision Making

ISBN: 978-0470239803

5th Edition

Authors: Jerry J. Weygandt, Paul D. Kimmel, Donald E. Kieso