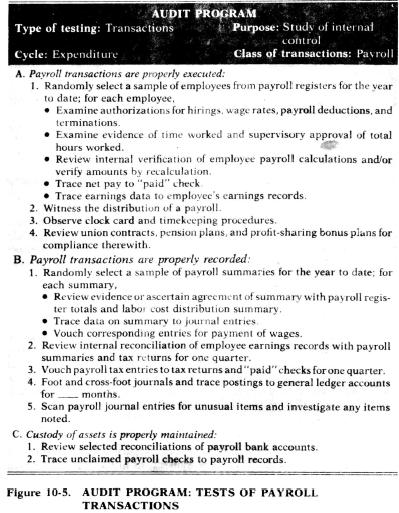

a. Identify the computer runs that are illustrated in Figure 10-5. b. Which runs may be tested

Question:

a. Identify the computer runs that are illustrated in Figure 10-5.

b. Which runs may be tested by the use of test data?

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Rukhsar Ansari

I am professional Chartered accountant and hold Master degree in commerce. Number crunching is my favorite thing. I have teaching experience of various subjects both online and offline. I am online tutor on various online platform.

4+ Reviews

17+ Question Solved

Related Book For

Modern Auditing

ISBN: 9780471542834

5th Edition

Authors: Walter Gerry Kell, William C. Boynton, Richard E. Ziegler

Question Posted: