Replacement of a machine, income taxes, sensitivity. (CMA, adapted) The Smacker Company is a family-owned business that

Question:

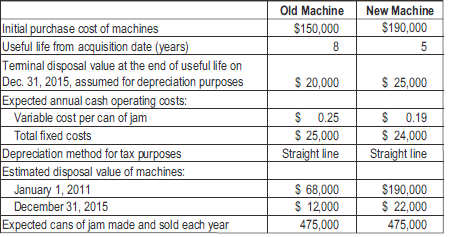

Replacement of a machine, income taxes, sensitivity. (CMA, adapted) The Smacker Company is a family-owned business that produces fruit jam. The company has a grinding machine that has been in use for three years. On January 1, 2011, Smacker is considering the purchase of a new grinding machine. Smacker has two options: (1) continue using the old machine or (2) sell the old machine and purchase a new machine. The seller of the new machine isn't offering a trade-in. The following information has been obtained:

Smacker is subject to a 36% income tax rate. Assume that any gain or loss on the sale of machines is treated as an ordinary tax item and will affect the taxes paid by Smacker in the year in which it occurs. Smacker's after-tax required rate of return is 14%. Assume all cash flows occur at year-end except for initial investment amounts.

Required

1. You have been asked whether Smacker should buy the new machine. To help in your analysis, calculate the following:

a. One-time after-tax cash effect of disposing of the old machine on January 1, 2011

b. Annual recurring after-tax cash operating savings from using the new machine (variable and fixed)

c. Cash tax savings due to differences in annual depreciation of the old machine and the new machine

d. Difference in after-tax cash flow from terminal disposal of new machine and old machine

2. Use your calculations in requirement 1 and the net present value method to determine whether Smacker should use the old machine or acquire the new machine.

3. How much more or less would the recurring after-tax cash operating savings of the new machine need to be for Smacker to earn exactly the 14% after-tax required rate of return? Assume that all other data about the investment do notchange.

What is NPV? The net present value is an important tool for capital budgeting decision to assess that an investment in a project is worthwhile or not? The net present value of a project is calculated before taking up the investment decision at...

Step by Step Answer:

Replacement of a machine income taxes sensitivity 1a Original cost of old machine 150 000 Depreciation taken during the first 3 years 15 0000 20000 8 ...View the full answer

Cost Accounting A Managerial Emphasis

ISBN: 978-0132109178

14th Edition

Authors: Charles T. Horngren, Srikant M.Dater, George Foster, Madhav