Hero MotoCorp Ltd. (Formerly Hero Honda Motors Ltd.) is the worlds largest manufacturer of twowheelers, based in

Question:

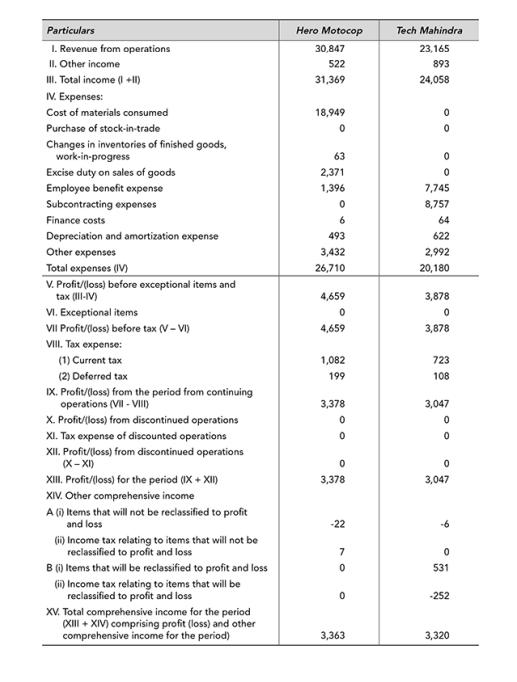

Hero MotoCorp Ltd. (Formerly Hero Honda Motors Ltd.) is the world’s largest manufacturer of twowheelers, based in India. In 2001, the company had achieved the coveted position of being the largest twowheeler manufacturing company in India and also, the ‘World No.1’ twowheeler company in terms of unit volume sales in a calendar year. Hero MotoCorp Ltd. continues to maintain this position till date.It derives its income from manufacturing and sale of motorcycles. Tech Mahindra Limited is engaged in the IT solutions and services, business process services and IT platforms. The company is present in 90 countries with over 115,000 associates.

The statements of profit and loss of two companies for the year ended 31st March 2017 are reproduced below:

Questions for Discussion

1. Comment upon the key differences in the composition of expenses for the two companies.

2. Hero Motocop has reported excise duty as a separate line item. Likewise, Tech Mahindra reported subcontracting expense as a separate line item rather than clubbing them with other expenses. What accounting principle in involved?

Step by Step Answer:

Hero MotoCorp Cost of goods sold This is the largest expense for Hero MotoCorp accounting for 723 of total expenses This is expected as it is a manufa...View the full answer