Gavin wants to dig deep into pricing theory, so he decides to work out an application of

Question:

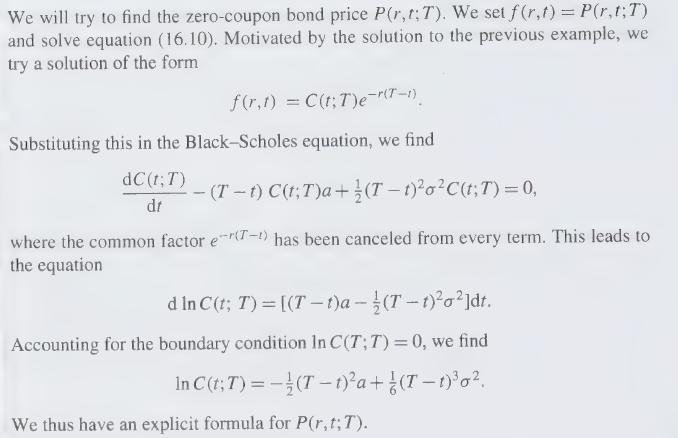

Gavin wants to dig deep into pricing theory, so he decides to work out an application of Eq. (16.11). He suggests to himself that a simple model of interest rates in the risk-neutral world might be

\[\mathrm{d} r=\sigma \mathrm{d} \hat{z}\]

where \(\hat{z}\) is standard Brownian motion and where \(r(0)=r_{0}\). He is working out a formula for the value of a zero-coupon bond that pays \(\$ 1\) at time \(T\), based on Equation (16.11), without using the Black-Scholes equation. Can you? Compare with Example 16.11.

Equation

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Nicholas Maina

Throughout my tutoring journey, I've amassed a wealth of hands-on experience and honed a diverse set of skills that enable me to guide students towards mastering complex subjects. My proficiency as a tutor rests on several key pillars:

1. Subject Mastery:

With a comprehensive understanding of a wide range of subjects spanning mathematics, science, humanities, and more, I can adeptly explain intricate concepts and break them down into digestible chunks. My proficiency extends to offering real-world applications, ensuring students grasp the practical relevance of their studies.

2. Individualized Guidance:

Recognizing that every student learns differently, I tailor my approach to accommodate various learning styles and paces. Through personalized interactions, I identify a student's strengths and areas for improvement, allowing me to craft targeted lessons that foster a deeper understanding of the material.

3. Problem-Solving Facilitation:

I excel in guiding students through problem-solving processes and encouraging critical thinking and analytical skills. By walking learners through step-by-step solutions and addressing their questions in a coherent manner, I empower them to approach challenges with confidence.

4. Effective Communication:

My tutoring proficiency is founded on clear and concise communication. I have the ability to convey complex ideas in an accessible manner, fostering a strong student-tutor rapport that encourages open dialogue and fruitful discussions.

5. Adaptability and Patience:

Tutoring is a dynamic process, and I have cultivated adaptability and patience to cater to evolving learning needs. I remain patient through difficulties, adjusting my teaching methods as necessary to ensure that students overcome obstacles and achieve their goals.

6. Interactive Learning:

Interactive learning lies at the heart of my approach. By engaging students in discussions, brainstorming sessions, and interactive exercises, I foster a stimulating learning environment that encourages active participation and long-term retention.

7. Continuous Improvement:

My dedication to being an effective tutor is a journey of continuous improvement. I regularly seek feedback and stay updated on educational methodologies, integrating new insights to refine my tutoring techniques and provide an even more enriching learning experience.

In essence, my hands-on experience as a tutor equips me with the tools to facilitate comprehensive understanding, critical thinking, and academic success. I am committed to helping students realize their full potential and fostering a passion for lifelong learning.

5+ Reviews

16+ Question Solved

Related Book For

Question Posted: