This exercise asks you to complete the GMM derivation in section 4.4 .3 of the standard asymptotic

Question:

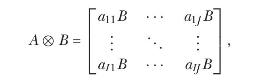

This exercise asks you to complete the GMM derivation in section 4.4 .3 of the standard asymptotic time-series test statistic (3.45). Use of the Kronecker product will be particularly useful. The Kronecker product, denoted by \(\otimes\), is a matrix operation defined as follows: if \(A\) and \(B\) are \(I \times J\) and \(K \times L\) matrices, respectively, their Kronecker product is the \(I K \times J L\) matrix:

Equation 3.45

where \(a_{i j}\) is the \((i, j)\) th element of \(A .{ }^{17}\)

\({ }^{17}\) The Kronecker product has the following properties:

\[

\begin{gathered}

A \otimes(B+C)=A \otimes B+A \otimes C \\

(A+B) \otimes C=A \otimes C+B \otimes C \\

(c A) \otimes B=A \otimes(c B)=c(A \otimes B) \\

(A \otimes B) \otimes C=A \otimes(B \otimes C) \\

(A \otimes B)(C \otimes D)=(A C) \otimes(B D) \\

(A \otimes B)^{-1}=A^{-1} \otimes B^{-1} \\

(A \otimes B)^{\prime}=A^{\prime} \otimes B^{\prime}, \end{gathered}

\]

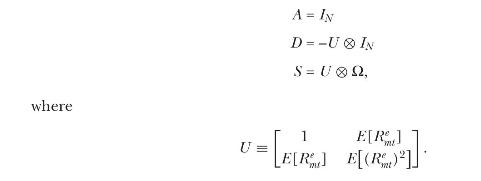

Write (4.92) and (4.96) as

Equation 4.92

Equation 4.96

Derive the formula for the asymptotic variance of the intercepts in the market model, (4.97).

Equation 4.97

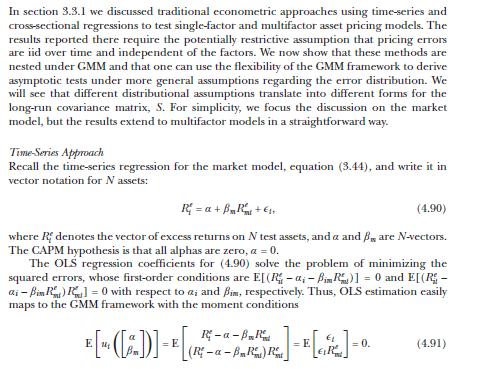

Data from section 4.4.3

Step by Step Answer:

Financial Decisions And Markets A Course In Asset Pricing

ISBN: 9780691160801

1st Edition

Authors: John Y. Campbell