With the cooperation of the cost accounting manager for the mill and each plant's controller, she...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

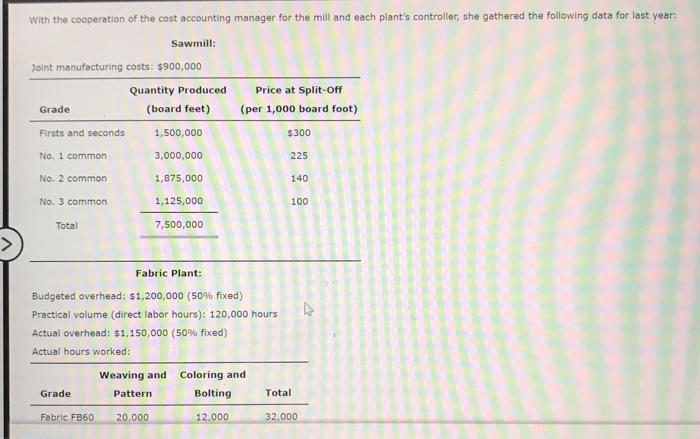

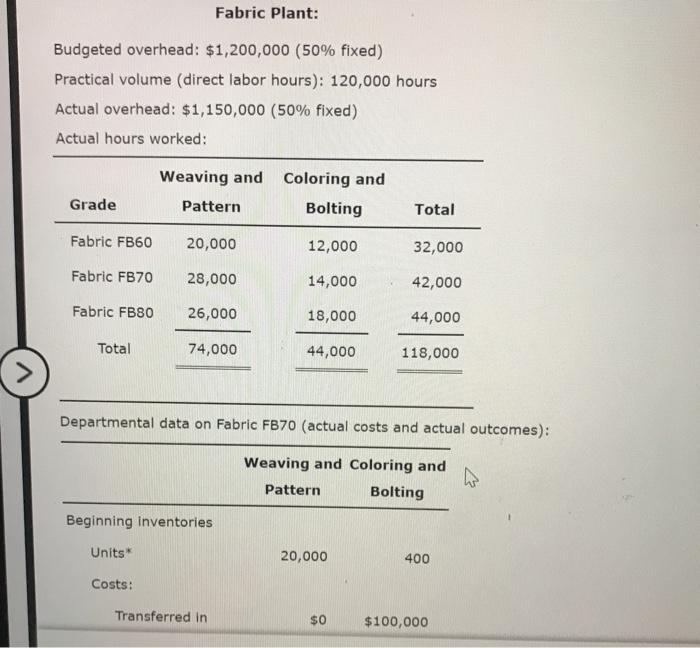

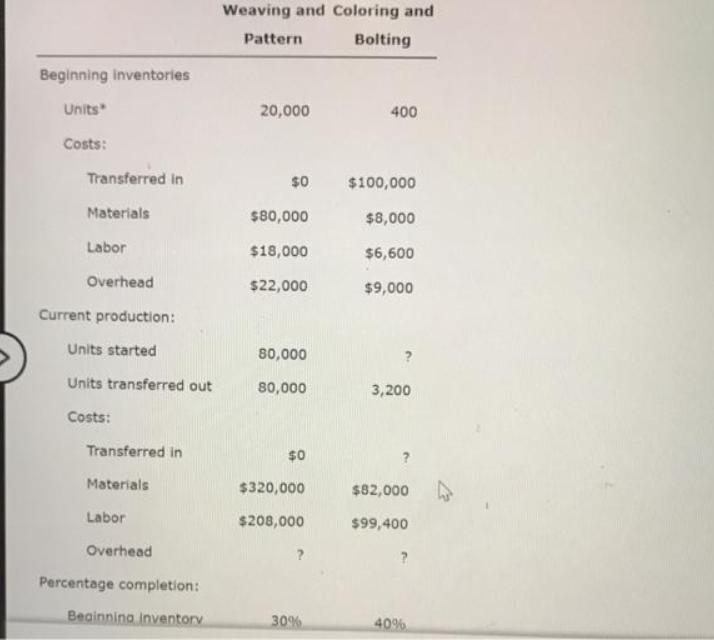

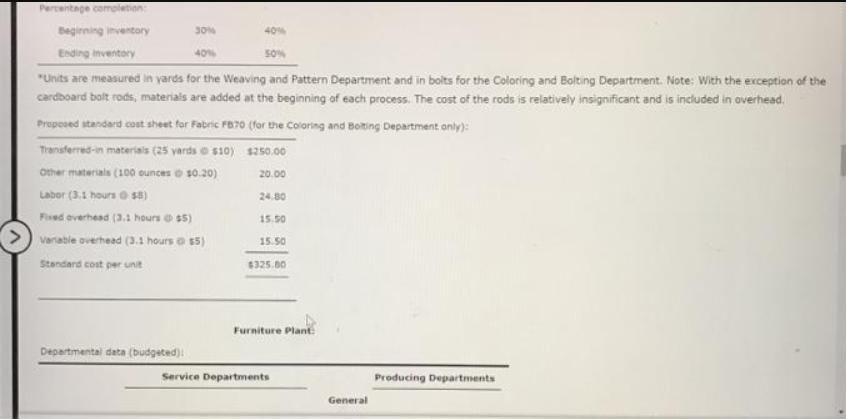

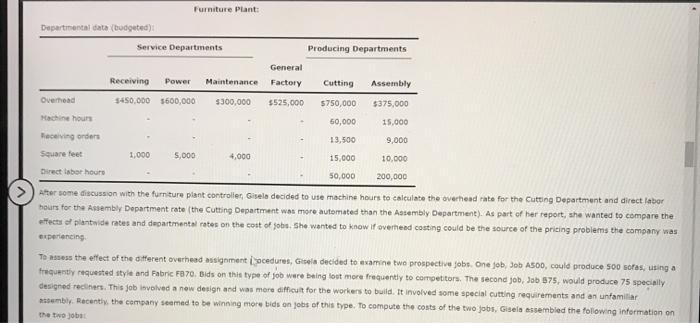

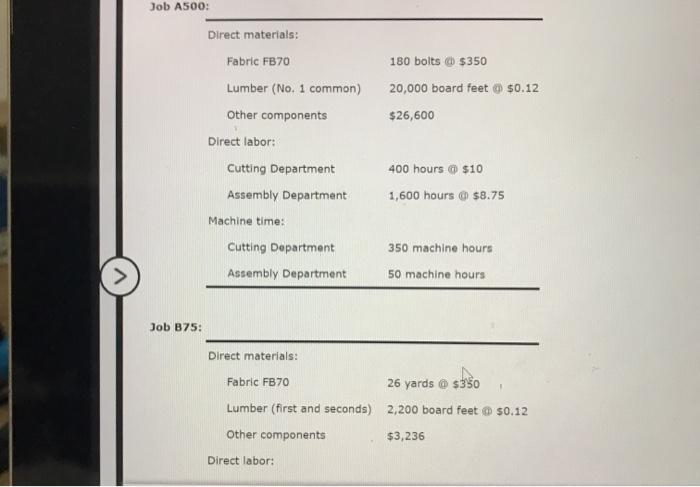

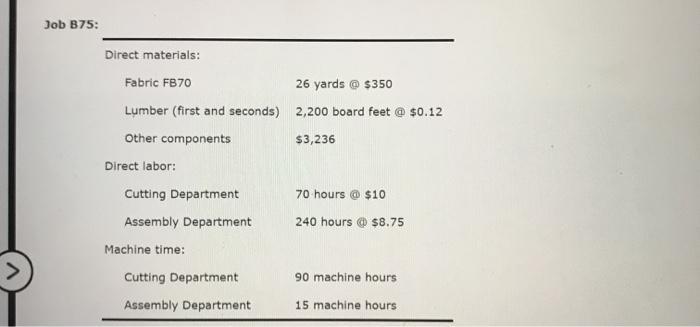

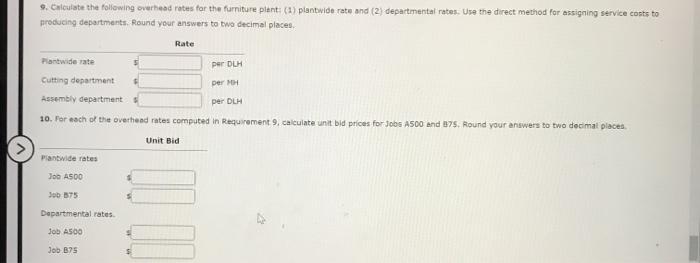

With the cooperation of the cost accounting manager for the mill and each plant's controller, she gathered the following data for last year: Sawmill: Joint manufacturing costs: $900,000 Grade Firsts and seconds. No. 1 common No. 2 common No. 3 common. Total Quantity Produced (board feet) Grade Fabric FB60 1,500,000 3,000,000 1,875,000 1,125,000 7,500,000 Fabric Plant: Budgeted overhead: $1,200,000 (50% fixed) Practical volume (direct labor hours): 120,000 hours Actual overhead: $1,150,000 (50% fixed) Actual hours worked: Price at Split-Off (per 1,000 board foot) 20,000 Weaving and Coloring and Pattern Bolting 12,000 $300 225 140 100 Total 32,000 > Fabric Plant: Budgeted overhead: $1,200,000 (50% fixed) Practical volume (direct labor hours): 120,000 hours Actual overhead: $1,150,000 (50% fixed) Actual hours worked: Grade Fabric FB60 Fabric FB70 Fabric FB80 Total Weaving and Coloring and Pattern Bolting Units* 20,000 Costs: 28,000 26,000 74,000 Beginning inventories 12,000 Transferred in 14,000 18,000 Departmental data on Fabric FB70 (actual costs and actual outcomes): Weaving and Coloring and Pattern Bolting 44,000 20,000 Total $0 32,000 42,000 44,000 118,000 400 $100,000 Beginning inventories Units" Costs: Transferred in Materials Labor Overhead Current production: Units started Units transferred out Costs: Transferred in Materials Labor Overhead Percentage completion: Beginning inventory Weaving and Coloring and Pattern Bolting 20,000 $0 $80,000 $18,000 $22,000 80,000 80,000 $0 $320,000 $208,000 30% 400 $100,000 $8,000 $6,600 $9,000 3,200 $82,000 $99,400 ? 40% Percentage completion: Beginning inventory Ending Inventory 40% 50% "Units are measured in yards for the Weaving and Pattern Department and in bolts for the Coloring and Bolting Department. Note: With the exception of the cardboard bolt rods, materials are added at the beginning of each process. The cost of the rods is relatively insignificant and is included in overhead. 30% Departmental data (budgeted) 40% Proposed standard cost sheet for Fabric FB20 (for the Coloring and Bolting Department only): Transferred-in materials (25 yards $10) $250.00 Other materials (100 ounces $0.20) 20.00 Labor (3.1 hours $8) Fixed overhead (3.1 hours @ $5) Variable overhead (3.1 hours $5) Standard cost per unit 24.80 15.50 15.50 $325.00 Furniture Plant Service Departments General Producing Departments Departmental data (budgeted): Overhead Machine hours Receiving orders Square feet Direct labor hours Furniture Plant: Service Departments General Receiving Power Maintenance Factory $450,000 $600,000 Cutting Assembly $300,000 $525,000 $750,000 $375,000 50,000 15,000 13,500 9,000 15,000 10,000 50,000 200,000 After some discussion with the furniture plant controller, Gisela decided to use machine hours to calculate the overhead rate for the Cutting Department and direct labor hours for the Assembly Department rate (the Cutting Department was more automated than the Assembly Department). As part of her report, she wanted to compare the effects of plantwide rates and departmental rates on the cost of jobs. She wanted to know if overhead casting could be the source of the pricing problems the company was experiencing. 1,000 5,000 Producing Departments 4,000 To assess the effect of the different overhead assignment ocedures, Gisela decided to examine two prospective jobs. One job, Job A500, could produce 500 sofas, using a frequently requested style and Fabric F870. Bids on this type of job were being lost more frequently to competitors. The second job, Job 575, would produce 75 specially designed recliners. This job involved a new design and was more difficult for the workers to build. It involved some special cutting requirements and an unfamiliar assembly. Recently, the company seemed to be winning more bids on jobs of this type. To compute the costs of the two jobs, Gisela assembled the following information on the two jobs Job A500: Job 875: Direct materials: Fabric FB70 Lumber (No. 1 common) Other components Direct labor: Cutting Department Assembly Department Machine time: Cutting Department Assembly Department Direct materials: Fabric FB70 Lumber (first and seconds) Other components Direct labor: 180 bolts @ $350 20,000 board feet @ $0.12 $26,600 400 hours @ $10 1,600 hours $8.75 350 machine hours 50 machine hours 26 yards @ $350 2,200 board feet @ $0.12 $3,236 Job B75: Direct materials: Fabric FB70 Lumber (first and seconds) Other components Direct labor: Cutting Department Assembly Department Machine time: Cutting Department Assembly Department 26 yards @ $350 2,200 board feet @ $0.12 $3,236 70 hours @ $10 240 hours @ $8.75 90 machine hours. 15 machine hours. 9. Calculate the following overhead rates for the furniture plant: (1) plantwide rate and (2) departmental rates. Use the direct method for assigning service costs to producing departments. Round your answers to two decimal places. Plantwide rate per DLH Cutting department per MH Assembly department per DLH 10. For each of the overhead rates computed in Requirement 9, calculate unit bid prices for Jobs A500 and 875. Round your answers to two decimal places. Plantwide rates Job A500 Job 875 Rate Departmental rates. Job A500 Job 875 Unit Bid Assume that the company's aggressive bidding policy is unit cost plus 50 percent. Did departmental overhead rates have any effect on Beauville's winning or losing bids? What recommendation would you make? Explain, Round your answers to two decimal places. Departmental rates decrease the bid for the more easily produced Job A500 and increase the bid for the more difficult to produce Job B75. This appears to be in the right direction. We would recommend using the departmental rates ✔ Now, adjust the costs and bids for departmental rate bids using the proposed standard costs for the Coloring and Bolting Department. Did this make a difference? What does this tell you? Round your answers to two decimal places. Enter all amounts as positive numbers. Standard cost would decrease ✔ the cost of Fabric FB70 for both jobs. For Job A500, prime costs will decrease ✔ by s will decrease ✔ by s And for Job 875, prime costs : Thus, the bid for Job A500 will decrease by Similarly, the bid for Job B75 will decrease ✔ by $ apparently avaid including waste in our bid by using standard costs and improve ✔ our bidding. It also tells us that we This tells us that we can need to focus on becoming more efficient. With the cooperation of the cost accounting manager for the mill and each plant's controller, she gathered the following data for last year: Sawmill: Joint manufacturing costs: $900,000 Grade Firsts and seconds. No. 1 common No. 2 common No. 3 common. Total Quantity Produced (board feet) Grade Fabric FB60 1,500,000 3,000,000 1,875,000 1,125,000 7,500,000 Fabric Plant: Budgeted overhead: $1,200,000 (50% fixed) Practical volume (direct labor hours): 120,000 hours Actual overhead: $1,150,000 (50% fixed) Actual hours worked: Price at Split-Off (per 1,000 board foot) 20,000 Weaving and Coloring and Pattern Bolting 12,000 $300 225 140 100 Total 32,000 > Fabric Plant: Budgeted overhead: $1,200,000 (50% fixed) Practical volume (direct labor hours): 120,000 hours Actual overhead: $1,150,000 (50% fixed) Actual hours worked: Grade Fabric FB60 Fabric FB70 Fabric FB80 Total Weaving and Coloring and Pattern Bolting Units* 20,000 Costs: 28,000 26,000 74,000 Beginning inventories 12,000 Transferred in 14,000 18,000 Departmental data on Fabric FB70 (actual costs and actual outcomes): Weaving and Coloring and Pattern Bolting 44,000 20,000 Total $0 32,000 42,000 44,000 118,000 400 $100,000 Beginning inventories Units" Costs: Transferred in Materials Labor Overhead Current production: Units started Units transferred out Costs: Transferred in Materials Labor Overhead Percentage completion: Beginning inventory Weaving and Coloring and Pattern Bolting 20,000 $0 $80,000 $18,000 $22,000 80,000 80,000 $0 $320,000 $208,000 30% 400 $100,000 $8,000 $6,600 $9,000 3,200 $82,000 $99,400 ? 40% Percentage completion: Beginning inventory Ending Inventory 40% 50% "Units are measured in yards for the Weaving and Pattern Department and in bolts for the Coloring and Bolting Department. Note: With the exception of the cardboard bolt rods, materials are added at the beginning of each process. The cost of the rods is relatively insignificant and is included in overhead. 30% Departmental data (budgeted) 40% Proposed standard cost sheet for Fabric FB20 (for the Coloring and Bolting Department only): Transferred-in materials (25 yards $10) $250.00 Other materials (100 ounces $0.20) 20.00 Labor (3.1 hours $8) Fixed overhead (3.1 hours @ $5) Variable overhead (3.1 hours $5) Standard cost per unit 24.80 15.50 15.50 $325.00 Furniture Plant Service Departments General Producing Departments Departmental data (budgeted): Overhead Machine hours Receiving orders Square feet Direct labor hours Furniture Plant: Service Departments General Receiving Power Maintenance Factory $450,000 $600,000 Cutting Assembly $300,000 $525,000 $750,000 $375,000 50,000 15,000 13,500 9,000 15,000 10,000 50,000 200,000 After some discussion with the furniture plant controller, Gisela decided to use machine hours to calculate the overhead rate for the Cutting Department and direct labor hours for the Assembly Department rate (the Cutting Department was more automated than the Assembly Department). As part of her report, she wanted to compare the effects of plantwide rates and departmental rates on the cost of jobs. She wanted to know if overhead casting could be the source of the pricing problems the company was experiencing. 1,000 5,000 Producing Departments 4,000 To assess the effect of the different overhead assignment ocedures, Gisela decided to examine two prospective jobs. One job, Job A500, could produce 500 sofas, using a frequently requested style and Fabric F870. Bids on this type of job were being lost more frequently to competitors. The second job, Job 575, would produce 75 specially designed recliners. This job involved a new design and was more difficult for the workers to build. It involved some special cutting requirements and an unfamiliar assembly. Recently, the company seemed to be winning more bids on jobs of this type. To compute the costs of the two jobs, Gisela assembled the following information on the two jobs Job A500: Job 875: Direct materials: Fabric FB70 Lumber (No. 1 common) Other components Direct labor: Cutting Department Assembly Department Machine time: Cutting Department Assembly Department Direct materials: Fabric FB70 Lumber (first and seconds) Other components Direct labor: 180 bolts @ $350 20,000 board feet @ $0.12 $26,600 400 hours @ $10 1,600 hours $8.75 350 machine hours 50 machine hours 26 yards @ $350 2,200 board feet @ $0.12 $3,236 Job B75: Direct materials: Fabric FB70 Lumber (first and seconds) Other components Direct labor: Cutting Department Assembly Department Machine time: Cutting Department Assembly Department 26 yards @ $350 2,200 board feet @ $0.12 $3,236 70 hours @ $10 240 hours @ $8.75 90 machine hours. 15 machine hours. 9. Calculate the following overhead rates for the furniture plant: (1) plantwide rate and (2) departmental rates. Use the direct method for assigning service costs to producing departments. Round your answers to two decimal places. Plantwide rate per DLH Cutting department per MH Assembly department per DLH 10. For each of the overhead rates computed in Requirement 9, calculate unit bid prices for Jobs A500 and 875. Round your answers to two decimal places. Plantwide rates Job A500 Job 875 Rate Departmental rates. Job A500 Job 875 Unit Bid Assume that the company's aggressive bidding policy is unit cost plus 50 percent. Did departmental overhead rates have any effect on Beauville's winning or losing bids? What recommendation would you make? Explain, Round your answers to two decimal places. Departmental rates decrease the bid for the more easily produced Job A500 and increase the bid for the more difficult to produce Job B75. This appears to be in the right direction. We would recommend using the departmental rates ✔ Now, adjust the costs and bids for departmental rate bids using the proposed standard costs for the Coloring and Bolting Department. Did this make a difference? What does this tell you? Round your answers to two decimal places. Enter all amounts as positive numbers. Standard cost would decrease ✔ the cost of Fabric FB70 for both jobs. For Job A500, prime costs will decrease ✔ by s will decrease ✔ by s And for Job 875, prime costs : Thus, the bid for Job A500 will decrease by Similarly, the bid for Job B75 will decrease ✔ by $ apparently avaid including waste in our bid by using standard costs and improve ✔ our bidding. It also tells us that we This tells us that we can need to focus on becoming more efficient. With the cooperation of the cost accounting manager for the mill and each plant's controller, she gathered the following data for last year: Sawmill: Joint manufacturing costs: $900,000 Grade Firsts and seconds. No. 1 common No. 2 common No. 3 common. Total Quantity Produced (board feet) Grade Fabric FB60 1,500,000 3,000,000 1,875,000 1,125,000 7,500,000 Fabric Plant: Budgeted overhead: $1,200,000 (50% fixed) Practical volume (direct labor hours): 120,000 hours Actual overhead: $1,150,000 (50% fixed) Actual hours worked: Price at Split-Off (per 1,000 board foot) 20,000 Weaving and Coloring and Pattern Bolting 12,000 $300 225 140 100 Total 32,000 > Fabric Plant: Budgeted overhead: $1,200,000 (50% fixed) Practical volume (direct labor hours): 120,000 hours Actual overhead: $1,150,000 (50% fixed) Actual hours worked: Grade Fabric FB60 Fabric FB70 Fabric FB80 Total Weaving and Coloring and Pattern Bolting Units* 20,000 Costs: 28,000 26,000 74,000 Beginning inventories 12,000 Transferred in 14,000 18,000 Departmental data on Fabric FB70 (actual costs and actual outcomes): Weaving and Coloring and Pattern Bolting 44,000 20,000 Total $0 32,000 42,000 44,000 118,000 400 $100,000 Beginning inventories Units" Costs: Transferred in Materials Labor Overhead Current production: Units started Units transferred out Costs: Transferred in Materials Labor Overhead Percentage completion: Beginning inventory Weaving and Coloring and Pattern Bolting 20,000 $0 $80,000 $18,000 $22,000 80,000 80,000 $0 $320,000 $208,000 30% 400 $100,000 $8,000 $6,600 $9,000 3,200 $82,000 $99,400 ? 40% Percentage completion: Beginning inventory Ending Inventory 40% 50% "Units are measured in yards for the Weaving and Pattern Department and in bolts for the Coloring and Bolting Department. Note: With the exception of the cardboard bolt rods, materials are added at the beginning of each process. The cost of the rods is relatively insignificant and is included in overhead. 30% Departmental data (budgeted) 40% Proposed standard cost sheet for Fabric FB20 (for the Coloring and Bolting Department only): Transferred-in materials (25 yards $10) $250.00 Other materials (100 ounces $0.20) 20.00 Labor (3.1 hours $8) Fixed overhead (3.1 hours @ $5) Variable overhead (3.1 hours $5) Standard cost per unit 24.80 15.50 15.50 $325.00 Furniture Plant Service Departments General Producing Departments Departmental data (budgeted): Overhead Machine hours Receiving orders Square feet Direct labor hours Furniture Plant: Service Departments General Receiving Power Maintenance Factory $450,000 $600,000 Cutting Assembly $300,000 $525,000 $750,000 $375,000 50,000 15,000 13,500 9,000 15,000 10,000 50,000 200,000 After some discussion with the furniture plant controller, Gisela decided to use machine hours to calculate the overhead rate for the Cutting Department and direct labor hours for the Assembly Department rate (the Cutting Department was more automated than the Assembly Department). As part of her report, she wanted to compare the effects of plantwide rates and departmental rates on the cost of jobs. She wanted to know if overhead casting could be the source of the pricing problems the company was experiencing. 1,000 5,000 Producing Departments 4,000 To assess the effect of the different overhead assignment ocedures, Gisela decided to examine two prospective jobs. One job, Job A500, could produce 500 sofas, using a frequently requested style and Fabric F870. Bids on this type of job were being lost more frequently to competitors. The second job, Job 575, would produce 75 specially designed recliners. This job involved a new design and was more difficult for the workers to build. It involved some special cutting requirements and an unfamiliar assembly. Recently, the company seemed to be winning more bids on jobs of this type. To compute the costs of the two jobs, Gisela assembled the following information on the two jobs Job A500: Job 875: Direct materials: Fabric FB70 Lumber (No. 1 common) Other components Direct labor: Cutting Department Assembly Department Machine time: Cutting Department Assembly Department Direct materials: Fabric FB70 Lumber (first and seconds) Other components Direct labor: 180 bolts @ $350 20,000 board feet @ $0.12 $26,600 400 hours @ $10 1,600 hours $8.75 350 machine hours 50 machine hours 26 yards @ $350 2,200 board feet @ $0.12 $3,236 Job B75: Direct materials: Fabric FB70 Lumber (first and seconds) Other components Direct labor: Cutting Department Assembly Department Machine time: Cutting Department Assembly Department 26 yards @ $350 2,200 board feet @ $0.12 $3,236 70 hours @ $10 240 hours @ $8.75 90 machine hours. 15 machine hours. 9. Calculate the following overhead rates for the furniture plant: (1) plantwide rate and (2) departmental rates. Use the direct method for assigning service costs to producing departments. Round your answers to two decimal places. Plantwide rate per DLH Cutting department per MH Assembly department per DLH 10. For each of the overhead rates computed in Requirement 9, calculate unit bid prices for Jobs A500 and 875. Round your answers to two decimal places. Plantwide rates Job A500 Job 875 Rate Departmental rates. Job A500 Job 875 Unit Bid Assume that the company's aggressive bidding policy is unit cost plus 50 percent. Did departmental overhead rates have any effect on Beauville's winning or losing bids? What recommendation would you make? Explain, Round your answers to two decimal places. Departmental rates decrease the bid for the more easily produced Job A500 and increase the bid for the more difficult to produce Job B75. This appears to be in the right direction. We would recommend using the departmental rates ✔ Now, adjust the costs and bids for departmental rate bids using the proposed standard costs for the Coloring and Bolting Department. Did this make a difference? What does this tell you? Round your answers to two decimal places. Enter all amounts as positive numbers. Standard cost would decrease ✔ the cost of Fabric FB70 for both jobs. For Job A500, prime costs will decrease ✔ by s will decrease ✔ by s And for Job 875, prime costs : Thus, the bid for Job A500 will decrease by Similarly, the bid for Job B75 will decrease ✔ by $ apparently avaid including waste in our bid by using standard costs and improve ✔ our bidding. It also tells us that we This tells us that we can need to focus on becoming more efficient. With the cooperation of the cost accounting manager for the mill and each plant's controller, she gathered the following data for last year: Sawmill: Joint manufacturing costs: $900,000 Grade Firsts and seconds. No. 1 common No. 2 common No. 3 common. Total Quantity Produced (board feet) Grade Fabric FB60 1,500,000 3,000,000 1,875,000 1,125,000 7,500,000 Fabric Plant: Budgeted overhead: $1,200,000 (50% fixed) Practical volume (direct labor hours): 120,000 hours Actual overhead: $1,150,000 (50% fixed) Actual hours worked: Price at Split-Off (per 1,000 board foot) 20,000 Weaving and Coloring and Pattern Bolting 12,000 $300 225 140 100 Total 32,000 > Fabric Plant: Budgeted overhead: $1,200,000 (50% fixed) Practical volume (direct labor hours): 120,000 hours Actual overhead: $1,150,000 (50% fixed) Actual hours worked: Grade Fabric FB60 Fabric FB70 Fabric FB80 Total Weaving and Coloring and Pattern Bolting Units* 20,000 Costs: 28,000 26,000 74,000 Beginning inventories 12,000 Transferred in 14,000 18,000 Departmental data on Fabric FB70 (actual costs and actual outcomes): Weaving and Coloring and Pattern Bolting 44,000 20,000 Total $0 32,000 42,000 44,000 118,000 400 $100,000 Beginning inventories Units" Costs: Transferred in Materials Labor Overhead Current production: Units started Units transferred out Costs: Transferred in Materials Labor Overhead Percentage completion: Beginning inventory Weaving and Coloring and Pattern Bolting 20,000 $0 $80,000 $18,000 $22,000 80,000 80,000 $0 $320,000 $208,000 30% 400 $100,000 $8,000 $6,600 $9,000 3,200 $82,000 $99,400 ? 40% Percentage completion: Beginning inventory Ending Inventory 40% 50% "Units are measured in yards for the Weaving and Pattern Department and in bolts for the Coloring and Bolting Department. Note: With the exception of the cardboard bolt rods, materials are added at the beginning of each process. The cost of the rods is relatively insignificant and is included in overhead. 30% Departmental data (budgeted) 40% Proposed standard cost sheet for Fabric FB20 (for the Coloring and Bolting Department only): Transferred-in materials (25 yards $10) $250.00 Other materials (100 ounces $0.20) 20.00 Labor (3.1 hours $8) Fixed overhead (3.1 hours @ $5) Variable overhead (3.1 hours $5) Standard cost per unit 24.80 15.50 15.50 $325.00 Furniture Plant Service Departments General Producing Departments Departmental data (budgeted): Overhead Machine hours Receiving orders Square feet Direct labor hours Furniture Plant: Service Departments General Receiving Power Maintenance Factory $450,000 $600,000 Cutting Assembly $300,000 $525,000 $750,000 $375,000 50,000 15,000 13,500 9,000 15,000 10,000 50,000 200,000 After some discussion with the furniture plant controller, Gisela decided to use machine hours to calculate the overhead rate for the Cutting Department and direct labor hours for the Assembly Department rate (the Cutting Department was more automated than the Assembly Department). As part of her report, she wanted to compare the effects of plantwide rates and departmental rates on the cost of jobs. She wanted to know if overhead casting could be the source of the pricing problems the company was experiencing. 1,000 5,000 Producing Departments 4,000 To assess the effect of the different overhead assignment ocedures, Gisela decided to examine two prospective jobs. One job, Job A500, could produce 500 sofas, using a frequently requested style and Fabric F870. Bids on this type of job were being lost more frequently to competitors. The second job, Job 575, would produce 75 specially designed recliners. This job involved a new design and was more difficult for the workers to build. It involved some special cutting requirements and an unfamiliar assembly. Recently, the company seemed to be winning more bids on jobs of this type. To compute the costs of the two jobs, Gisela assembled the following information on the two jobs Job A500: Job 875: Direct materials: Fabric FB70 Lumber (No. 1 common) Other components Direct labor: Cutting Department Assembly Department Machine time: Cutting Department Assembly Department Direct materials: Fabric FB70 Lumber (first and seconds) Other components Direct labor: 180 bolts @ $350 20,000 board feet @ $0.12 $26,600 400 hours @ $10 1,600 hours $8.75 350 machine hours 50 machine hours 26 yards @ $350 2,200 board feet @ $0.12 $3,236 Job B75: Direct materials: Fabric FB70 Lumber (first and seconds) Other components Direct labor: Cutting Department Assembly Department Machine time: Cutting Department Assembly Department 26 yards @ $350 2,200 board feet @ $0.12 $3,236 70 hours @ $10 240 hours @ $8.75 90 machine hours. 15 machine hours. 9. Calculate the following overhead rates for the furniture plant: (1) plantwide rate and (2) departmental rates. Use the direct method for assigning service costs to producing departments. Round your answers to two decimal places. Plantwide rate per DLH Cutting department per MH Assembly department per DLH 10. For each of the overhead rates computed in Requirement 9, calculate unit bid prices for Jobs A500 and 875. Round your answers to two decimal places. Plantwide rates Job A500 Job 875 Rate Departmental rates. Job A500 Job 875 Unit Bid Assume that the company's aggressive bidding policy is unit cost plus 50 percent. Did departmental overhead rates have any effect on Beauville's winning or losing bids? What recommendation would you make? Explain, Round your answers to two decimal places. Departmental rates decrease the bid for the more easily produced Job A500 and increase the bid for the more difficult to produce Job B75. This appears to be in the right direction. We would recommend using the departmental rates ✔ Now, adjust the costs and bids for departmental rate bids using the proposed standard costs for the Coloring and Bolting Department. Did this make a difference? What does this tell you? Round your answers to two decimal places. Enter all amounts as positive numbers. Standard cost would decrease ✔ the cost of Fabric FB70 for both jobs. For Job A500, prime costs will decrease ✔ by s will decrease ✔ by s And for Job 875, prime costs : Thus, the bid for Job A500 will decrease by Similarly, the bid for Job B75 will decrease ✔ by $ apparently avaid including waste in our bid by using standard costs and improve ✔ our bidding. It also tells us that we This tells us that we can need to focus on becoming more efficient. With the cooperation of the cost accounting manager for the mill and each plant's controller, she gathered the following data for last year: Sawmill: Joint manufacturing costs: $900,000 Grade Firsts and seconds. No. 1 common No. 2 common No. 3 common. Total Quantity Produced (board feet) Grade Fabric FB60 1,500,000 3,000,000 1,875,000 1,125,000 7,500,000 Fabric Plant: Budgeted overhead: $1,200,000 (50% fixed) Practical volume (direct labor hours): 120,000 hours Actual overhead: $1,150,000 (50% fixed) Actual hours worked: Price at Split-Off (per 1,000 board foot) 20,000 Weaving and Coloring and Pattern Bolting 12,000 $300 225 140 100 Total 32,000 > Fabric Plant: Budgeted overhead: $1,200,000 (50% fixed) Practical volume (direct labor hours): 120,000 hours Actual overhead: $1,150,000 (50% fixed) Actual hours worked: Grade Fabric FB60 Fabric FB70 Fabric FB80 Total Weaving and Coloring and Pattern Bolting Units* 20,000 Costs: 28,000 26,000 74,000 Beginning inventories 12,000 Transferred in 14,000 18,000 Departmental data on Fabric FB70 (actual costs and actual outcomes): Weaving and Coloring and Pattern Bolting 44,000 20,000 Total $0 32,000 42,000 44,000 118,000 400 $100,000 Beginning inventories Units" Costs: Transferred in Materials Labor Overhead Current production: Units started Units transferred out Costs: Transferred in Materials Labor Overhead Percentage completion: Beginning inventory Weaving and Coloring and Pattern Bolting 20,000 $0 $80,000 $18,000 $22,000 80,000 80,000 $0 $320,000 $208,000 30% 400 $100,000 $8,000 $6,600 $9,000 3,200 $82,000 $99,400 ? 40% Percentage completion: Beginning inventory Ending Inventory 40% 50% "Units are measured in yards for the Weaving and Pattern Department and in bolts for the Coloring and Bolting Department. Note: With the exception of the cardboard bolt rods, materials are added at the beginning of each process. The cost of the rods is relatively insignificant and is included in overhead. 30% Departmental data (budgeted) 40% Proposed standard cost sheet for Fabric FB20 (for the Coloring and Bolting Department only): Transferred-in materials (25 yards $10) $250.00 Other materials (100 ounces $0.20) 20.00 Labor (3.1 hours $8) Fixed overhead (3.1 hours @ $5) Variable overhead (3.1 hours $5) Standard cost per unit 24.80 15.50 15.50 $325.00 Furniture Plant Service Departments General Producing Departments Departmental data (budgeted): Overhead Machine hours Receiving orders Square feet Direct labor hours Furniture Plant: Service Departments General Receiving Power Maintenance Factory $450,000 $600,000 Cutting Assembly $300,000 $525,000 $750,000 $375,000 50,000 15,000 13,500 9,000 15,000 10,000 50,000 200,000 After some discussion with the furniture plant controller, Gisela decided to use machine hours to calculate the overhead rate for the Cutting Department and direct labor hours for the Assembly Department rate (the Cutting Department was more automated than the Assembly Department). As part of her report, she wanted to compare the effects of plantwide rates and departmental rates on the cost of jobs. She wanted to know if overhead casting could be the source of the pricing problems the company was experiencing. 1,000 5,000 Producing Departments 4,000 To assess the effect of the different overhead assignment ocedures, Gisela decided to examine two prospective jobs. One job, Job A500, could produce 500 sofas, using a frequently requested style and Fabric F870. Bids on this type of job were being lost more frequently to competitors. The second job, Job 575, would produce 75 specially designed recliners. This job involved a new design and was more difficult for the workers to build. It involved some special cutting requirements and an unfamiliar assembly. Recently, the company seemed to be winning more bids on jobs of this type. To compute the costs of the two jobs, Gisela assembled the following information on the two jobs Job A500: Job 875: Direct materials: Fabric FB70 Lumber (No. 1 common) Other components Direct labor: Cutting Department Assembly Department Machine time: Cutting Department Assembly Department Direct materials: Fabric FB70 Lumber (first and seconds) Other components Direct labor: 180 bolts @ $350 20,000 board feet @ $0.12 $26,600 400 hours @ $10 1,600 hours $8.75 350 machine hours 50 machine hours 26 yards @ $350 2,200 board feet @ $0.12 $3,236 Job B75: Direct materials: Fabric FB70 Lumber (first and seconds) Other components Direct labor: Cutting Department Assembly Department Machine time: Cutting Department Assembly Department 26 yards @ $350 2,200 board feet @ $0.12 $3,236 70 hours @ $10 240 hours @ $8.75 90 machine hours. 15 machine hours. 9. Calculate the following overhead rates for the furniture plant: (1) plantwide rate and (2) departmental rates. Use the direct method for assigning service costs to producing departments. Round your answers to two decimal places. Plantwide rate per DLH Cutting department per MH Assembly department per DLH 10. For each of the overhead rates computed in Requirement 9, calculate unit bid prices for Jobs A500 and 875. Round your answers to two decimal places. Plantwide rates Job A500 Job 875 Rate Departmental rates. Job A500 Job 875 Unit Bid Assume that the company's aggressive bidding policy is unit cost plus 50 percent. Did departmental overhead rates have any effect on Beauville's winning or losing bids? What recommendation would you make? Explain, Round your answers to two decimal places. Departmental rates decrease the bid for the more easily produced Job A500 and increase the bid for the more difficult to produce Job B75. This appears to be in the right direction. We would recommend using the departmental rates ✔ Now, adjust the costs and bids for departmental rate bids using the proposed standard costs for the Coloring and Bolting Department. Did this make a difference? What does this tell you? Round your answers to two decimal places. Enter all amounts as positive numbers. Standard cost would decrease ✔ the cost of Fabric FB70 for both jobs. For Job A500, prime costs will decrease ✔ by s will decrease ✔ by s And for Job 875, prime costs : Thus, the bid for Job A500 will decrease by Similarly, the bid for Job B75 will decrease ✔ by $ apparently avaid including waste in our bid by using standard costs and improve ✔ our bidding. It also tells us that we This tells us that we can need to focus on becoming more efficient. With the cooperation of the cost accounting manager for the mill and each plant's controller, she gathered the following data for last year: Sawmill: Joint manufacturing costs: $900,000 Grade Firsts and seconds. No. 1 common No. 2 common No. 3 common. Total Quantity Produced (board feet) Grade Fabric FB60 1,500,000 3,000,000 1,875,000 1,125,000 7,500,000 Fabric Plant: Budgeted overhead: $1,200,000 (50% fixed) Practical volume (direct labor hours): 120,000 hours Actual overhead: $1,150,000 (50% fixed) Actual hours worked: Price at Split-Off (per 1,000 board foot) 20,000 Weaving and Coloring and Pattern Bolting 12,000 $300 225 140 100 Total 32,000 > Fabric Plant: Budgeted overhead: $1,200,000 (50% fixed) Practical volume (direct labor hours): 120,000 hours Actual overhead: $1,150,000 (50% fixed) Actual hours worked: Grade Fabric FB60 Fabric FB70 Fabric FB80 Total Weaving and Coloring and Pattern Bolting Units* 20,000 Costs: 28,000 26,000 74,000 Beginning inventories 12,000 Transferred in 14,000 18,000 Departmental data on Fabric FB70 (actual costs and actual outcomes): Weaving and Coloring and Pattern Bolting 44,000 20,000 Total $0 32,000 42,000 44,000 118,000 400 $100,000 Beginning inventories Units" Costs: Transferred in Materials Labor Overhead Current production: Units started Units transferred out Costs: Transferred in Materials Labor Overhead Percentage completion: Beginning inventory Weaving and Coloring and Pattern Bolting 20,000 $0 $80,000 $18,000 $22,000 80,000 80,000 $0 $320,000 $208,000 30% 400 $100,000 $8,000 $6,600 $9,000 3,200 $82,000 $99,400 ? 40% Percentage completion: Beginning inventory Ending Inventory 40% 50% "Units are measured in yards for the Weaving and Pattern Department and in bolts for the Coloring and Bolting Department. Note: With the exception of the cardboard bolt rods, materials are added at the beginning of each process. The cost of the rods is relatively insignificant and is included in overhead. 30% Departmental data (budgeted) 40% Proposed standard cost sheet for Fabric FB20 (for the Coloring and Bolting Department only): Transferred-in materials (25 yards $10) $250.00 Other materials (100 ounces $0.20) 20.00 Labor (3.1 hours $8) Fixed overhead (3.1 hours @ $5) Variable overhead (3.1 hours $5) Standard cost per unit 24.80 15.50 15.50 $325.00 Furniture Plant Service Departments General Producing Departments Departmental data (budgeted): Overhead Machine hours Receiving orders Square feet Direct labor hours Furniture Plant: Service Departments General Receiving Power Maintenance Factory $450,000 $600,000 Cutting Assembly $300,000 $525,000 $750,000 $375,000 50,000 15,000 13,500 9,000 15,000 10,000 50,000 200,000 After some discussion with the furniture plant controller, Gisela decided to use machine hours to calculate the overhead rate for the Cutting Department and direct labor hours for the Assembly Department rate (the Cutting Department was more automated than the Assembly Department). As part of her report, she wanted to compare the effects of plantwide rates and departmental rates on the cost of jobs. She wanted to know if overhead casting could be the source of the pricing problems the company was experiencing. 1,000 5,000 Producing Departments 4,000 To assess the effect of the different overhead assignment ocedures, Gisela decided to examine two prospective jobs. One job, Job A500, could produce 500 sofas, using a frequently requested style and Fabric F870. Bids on this type of job were being lost more frequently to competitors. The second job, Job 575, would produce 75 specially designed recliners. This job involved a new design and was more difficult for the workers to build. It involved some special cutting requirements and an unfamiliar assembly. Recently, the company seemed to be winning more bids on jobs of this type. To compute the costs of the two jobs, Gisela assembled the following information on the two jobs Job A500: Job 875: Direct materials: Fabric FB70 Lumber (No. 1 common) Other components Direct labor: Cutting Department Assembly Department Machine time: Cutting Department Assembly Department Direct materials: Fabric FB70 Lumber (first and seconds) Other components Direct labor: 180 bolts @ $350 20,000 board feet @ $0.12 $26,600 400 hours @ $10 1,600 hours $8.75 350 machine hours 50 machine hours 26 yards @ $350 2,200 board feet @ $0.12 $3,236 Job B75: Direct materials: Fabric FB70 Lumber (first and seconds) Other components Direct labor: Cutting Department Assembly Department Machine time: Cutting Department Assembly Department 26 yards @ $350 2,200 board feet @ $0.12 $3,236 70 hours @ $10 240 hours @ $8.75 90 machine hours. 15 machine hours. 9. Calculate the following overhead rates for the furniture plant: (1) plantwide rate and (2) departmental rates. Use the direct method for assigning service costs to producing departments. Round your answers to two decimal places. Plantwide rate per DLH Cutting department per MH Assembly department per DLH 10. For each of the overhead rates computed in Requirement 9, calculate unit bid prices for Jobs A500 and 875. Round your answers to two decimal places. Plantwide rates Job A500 Job 875 Rate Departmental rates. Job A500 Job 875 Unit Bid Assume that the company's aggressive bidding policy is unit cost plus 50 percent. Did departmental overhead rates have any effect on Beauville's winning or losing bids? What recommendation would you make? Explain, Round your answers to two decimal places. Departmental rates decrease the bid for the more easily produced Job A500 and increase the bid for the more difficult to produce Job B75. This appears to be in the right direction. We would recommend using the departmental rates ✔ Now, adjust the costs and bids for departmental rate bids using the proposed standard costs for the Coloring and Bolting Department. Did this make a difference? What does this tell you? Round your answers to two decimal places. Enter all amounts as positive numbers. Standard cost would decrease ✔ the cost of Fabric FB70 for both jobs. For Job A500, prime costs will decrease ✔ by s will decrease ✔ by s And for Job 875, prime costs : Thus, the bid for Job A500 will decrease by Similarly, the bid for Job B75 will decrease ✔ by $ apparently avaid including waste in our bid by using standard costs and improve ✔ our bidding. It also tells us that we This tells us that we can need to focus on becoming more efficient. With the cooperation of the cost accounting manager for the mill and each plant's controller, she gathered the following data for last year: Sawmill: Joint manufacturing costs: $900,000 Grade Firsts and seconds. No. 1 common No. 2 common No. 3 common. Total Quantity Produced (board feet) Grade Fabric FB60 1,500,000 3,000,000 1,875,000 1,125,000 7,500,000 Fabric Plant: Budgeted overhead: $1,200,000 (50% fixed) Practical volume (direct labor hours): 120,000 hours Actual overhead: $1,150,000 (50% fixed) Actual hours worked: Price at Split-Off (per 1,000 board foot) 20,000 Weaving and Coloring and Pattern Bolting 12,000 $300 225 140 100 Total 32,000 > Fabric Plant: Budgeted overhead: $1,200,000 (50% fixed) Practical volume (direct labor hours): 120,000 hours Actual overhead: $1,150,000 (50% fixed) Actual hours worked: Grade Fabric FB60 Fabric FB70 Fabric FB80 Total Weaving and Coloring and Pattern Bolting Units* 20,000 Costs: 28,000 26,000 74,000 Beginning inventories 12,000 Transferred in 14,000 18,000 Departmental data on Fabric FB70 (actual costs and actual outcomes): Weaving and Coloring and Pattern Bolting 44,000 20,000 Total $0 32,000 42,000 44,000 118,000 400 $100,000 Beginning inventories Units" Costs: Transferred in Materials Labor Overhead Current production: Units started Units transferred out Costs: Transferred in Materials Labor Overhead Percentage completion: Beginning inventory Weaving and Coloring and Pattern Bolting 20,000 $0 $80,000 $18,000 $22,000 80,000 80,000 $0 $320,000 $208,000 30% 400 $100,000 $8,000 $6,600 $9,000 3,200 $82,000 $99,400 ? 40% Percentage completion: Beginning inventory Ending Inventory 40% 50% "Units are measured in yards for the Weaving and Pattern Department and in bolts for the Coloring and Bolting Department. Note: With the exception of the cardboard bolt rods, materials are added at the beginning of each process. The cost of the rods is relatively insignificant and is included in overhead. 30% Departmental data (budgeted) 40% Proposed standard cost sheet for Fabric FB20 (for the Coloring and Bolting Department only): Transferred-in materials (25 yards $10) $250.00 Other materials (100 ounces $0.20) 20.00 Labor (3.1 hours $8) Fixed overhead (3.1 hours @ $5) Variable overhead (3.1 hours $5) Standard cost per unit 24.80 15.50 15.50 $325.00 Furniture Plant Service Departments General Producing Departments Departmental data (budgeted): Overhead Machine hours Receiving orders Square feet Direct labor hours Furniture Plant: Service Departments General Receiving Power Maintenance Factory $450,000 $600,000 Cutting Assembly $300,000 $525,000 $750,000 $375,000 50,000 15,000 13,500 9,000 15,000 10,000 50,000 200,000 After some discussion with the furniture plant controller, Gisela decided to use machine hours to calculate the overhead rate for the Cutting Department and direct labor hours for the Assembly Department rate (the Cutting Department was more automated than the Assembly Department). As part of her report, she wanted to compare the effects of plantwide rates and departmental rates on the cost of jobs. She wanted to know if overhead casting could be the source of the pricing problems the company was experiencing. 1,000 5,000 Producing Departments 4,000 To assess the effect of the different overhead assignment ocedures, Gisela decided to examine two prospective jobs. One job, Job A500, could produce 500 sofas, using a frequently requested style and Fabric F870. Bids on this type of job were being lost more frequently to competitors. The second job, Job 575, would produce 75 specially designed recliners. This job involved a new design and was more difficult for the workers to build. It involved some special cutting requirements and an unfamiliar assembly. Recently, the company seemed to be winning more bids on jobs of this type. To compute the costs of the two jobs, Gisela assembled the following information on the two jobs Job A500: Job 875: Direct materials: Fabric FB70 Lumber (No. 1 common) Other components Direct labor: Cutting Department Assembly Department Machine time: Cutting Department Assembly Department Direct materials: Fabric FB70 Lumber (first and seconds) Other components Direct labor: 180 bolts @ $350 20,000 board feet @ $0.12 $26,600 400 hours @ $10 1,600 hours $8.75 350 machine hours 50 machine hours 26 yards @ $350 2,200 board feet @ $0.12 $3,236 Job B75: Direct materials: Fabric FB70 Lumber (first and seconds) Other components Direct labor: Cutting Department Assembly Department Machine time: Cutting Department Assembly Department 26 yards @ $350 2,200 board feet @ $0.12 $3,236 70 hours @ $10 240 hours @ $8.75 90 machine hours. 15 machine hours. 9. Calculate the following overhead rates for the furniture plant: (1) plantwide rate and (2) departmental rates. Use the direct method for assigning service costs to producing departments. Round your answers to two decimal places. Plantwide rate per DLH Cutting department per MH Assembly department per DLH 10. For each of the overhead rates computed in Requirement 9, calculate unit bid prices for Jobs A500 and 875. Round your answers to two decimal places. Plantwide rates Job A500 Job 875 Rate Departmental rates. Job A500 Job 875 Unit Bid Assume that the company's aggressive bidding policy is unit cost plus 50 percent. Did departmental overhead rates have any effect on Beauville's winning or losing bids? What recommendation would you make? Explain, Round your answers to two decimal places. Departmental rates decrease the bid for the more easily produced Job A500 and increase the bid for the more difficult to produce Job B75. This appears to be in the right direction. We would recommend using the departmental rates ✔ Now, adjust the costs and bids for departmental rate bids using the proposed standard costs for the Coloring and Bolting Department. Did this make a difference? What does this tell you? Round your answers to two decimal places. Enter all amounts as positive numbers. Standard cost would decrease ✔ the cost of Fabric FB70 for both jobs. For Job A500, prime costs will decrease ✔ by s will decrease ✔ by s And for Job 875, prime costs : Thus, the bid for Job A500 will decrease by Similarly, the bid for Job B75 will decrease ✔ by $ apparently avaid including waste in our bid by using standard costs and improve ✔ our bidding. It also tells us that we This tells us that we can need to focus on becoming more efficient. With the cooperation of the cost accounting manager for the mill and each plant's controller, she gathered the following data for last year: Sawmill: Joint manufacturing costs: $900,000 Grade Firsts and seconds. No. 1 common No. 2 common No. 3 common. Total Quantity Produced (board feet) Grade Fabric FB60 1,500,000 3,000,000 1,875,000 1,125,000 7,500,000 Fabric Plant: Budgeted overhead: $1,200,000 (50% fixed) Practical volume (direct labor hours): 120,000 hours Actual overhead: $1,150,000 (50% fixed) Actual hours worked: Price at Split-Off (per 1,000 board foot) 20,000 Weaving and Coloring and Pattern Bolting 12,000 $300 225 140 100 Total 32,000 > Fabric Plant: Budgeted overhead: $1,200,000 (50% fixed) Practical volume (direct labor hours): 120,000 hours Actual overhead: $1,150,000 (50% fixed) Actual hours worked: Grade Fabric FB60 Fabric FB70 Fabric FB80 Total Weaving and Coloring and Pattern Bolting Units* 20,000 Costs: 28,000 26,000 74,000 Beginning inventories 12,000 Transferred in 14,000 18,000 Departmental data on Fabric FB70 (actual costs and actual outcomes): Weaving and Coloring and Pattern Bolting 44,000 20,000 Total $0 32,000 42,000 44,000 118,000 400 $100,000 Beginning inventories Units" Costs: Transferred in Materials Labor Overhead Current production: Units started Units transferred out Costs: Transferred in Materials Labor Overhead Percentage completion: Beginning inventory Weaving and Coloring and Pattern Bolting 20,000 $0 $80,000 $18,000 $22,000 80,000 80,000 $0 $320,000 $208,000 30% 400 $100,000 $8,000 $6,600 $9,000 3,200 $82,000 $99,400 ? 40% Percentage completion: Beginning inventory Ending Inventory 40% 50% "Units are measured in yards for the Weaving and Pattern Department and in bolts for the Coloring and Bolting Department. Note: With the exception of the cardboard bolt rods, materials are added at the beginning of each process. The cost of the rods is relatively insignificant and is included in overhead. 30% Departmental data (budgeted) 40% Proposed standard cost sheet for Fabric FB20 (for the Coloring and Bolting Department only): Transferred-in materials (25 yards $10) $250.00 Other materials (100 ounces $0.20) 20.00 Labor (3.1 hours $8) Fixed overhead (3.1 hours @ $5) Variable overhead (3.1 hours $5) Standard cost per unit 24.80 15.50 15.50 $325.00 Furniture Plant Service Departments General Producing Departments Departmental data (budgeted): Overhead Machine hours Receiving orders Square feet Direct labor hours Furniture Plant: Service Departments General Receiving Power Maintenance Factory $450,000 $600,000 Cutting Assembly $300,000 $525,000 $750,000 $375,000 50,000 15,000 13,500 9,000 15,000 10,000 50,000 200,000 After some discussion with the furniture plant controller, Gisela decided to use machine hours to calculate the overhead rate for the Cutting Department and direct labor hours for the Assembly Department rate (the Cutting Department was more automated than the Assembly Department). As part of her report, she wanted to compare the effects of plantwide rates and departmental rates on the cost of jobs. She wanted to know if overhead casting could be the source of the pricing problems the company was experiencing. 1,000 5,000 Producing Departments 4,000 To assess the effect of the different overhead assignment ocedures, Gisela decided to examine two prospective jobs. One job, Job A500, could produce 500 sofas, using a frequently requested style and Fabric F870. Bids on this type of job were being lost more frequently to competitors. The second job, Job 575, would produce 75 specially designed recliners. This job involved a new design and was more difficult for the workers to build. It involved some special cutting requirements and an unfamiliar assembly. Recently, the company seemed to be winning more bids on jobs of this type. To compute the costs of the two jobs, Gisela assembled the following information on the two jobs Job A500: Job 875: Direct materials: Fabric FB70 Lumber (No. 1 common) Other components Direct labor: Cutting Department Assembly Department Machine time: Cutting Department Assembly Department Direct materials: Fabric FB70 Lumber (first and seconds) Other components Direct labor: 180 bolts @ $350 20,000 board feet @ $0.12 $26,600 400 hours @ $10 1,600 hours $8.75 350 machine hours 50 machine hours 26 yards @ $350 2,200 board feet @ $0.12 $3,236 Job B75: Direct materials: Fabric FB70 Lumber (first and seconds) Other components Direct labor: Cutting Department Assembly Department Machine time: Cutting Department Assembly Department 26 yards @ $350 2,200 board feet @ $0.12 $3,236 70 hours @ $10 240 hours @ $8.75 90 machine hours. 15 machine hours. 9. Calculate the following overhead rates for the furniture plant: (1) plantwide rate and (2) departmental rates. Use the direct method for assigning service costs to producing departments. Round your answers to two decimal places. Plantwide rate per DLH Cutting department per MH Assembly department per DLH 10. For each of the overhead rates computed in Requirement 9, calculate unit bid prices for Jobs A500 and 875. Round your answers to two decimal places. Plantwide rates Job A500 Job 875 Rate Departmental rates. Job A500 Job 875 Unit Bid Assume that the company's aggressive bidding policy is unit cost plus 50 percent. Did departmental overhead rates have any effect on Beauville's winning or losing bids? What recommendation would you make? Explain, Round your answers to two decimal places. Departmental rates decrease the bid for the more easily produced Job A500 and increase the bid for the more difficult to produce Job B75. This appears to be in the right direction. We would recommend using the departmental rates ✔ Now, adjust the costs and bids for departmental rate bids using the proposed standard costs for the Coloring and Bolting Department. Did this make a difference? What does this tell you? Round your answers to two decimal places. Enter all amounts as positive numbers. Standard cost would decrease ✔ the cost of Fabric FB70 for both jobs. For Job A500, prime costs will decrease ✔ by s will decrease ✔ by s And for Job 875, prime costs : Thus, the bid for Job A500 will decrease by Similarly, the bid for Job B75 will decrease ✔ by $ apparently avaid including waste in our bid by using standard costs and improve ✔ our bidding. It also tells us that we This tells us that we can need to focus on becoming more efficient.

Expert Answer:

Answer rating: 100% (QA)

Answer 1 a Physical Unit Method of Allocation Grades Quantity Produced Boards Feet Allocation Unit C... View the full answer

Related Book For

Managerial Accounting

ISBN: 978-1118385388

2nd edition

Authors: Ramji Balakrishnan, Konduru Sivaramakrishnan, Geoff B. Sprinkle

Posted Date:

Students also viewed these accounting questions

-

The (partial) cost sheet for the single product manufactured at Vienna Company follows. Direct labor (6 hours @ $20) (6 hours e $2) (6 hours e $4) $120 Variable overhead 12 Fixed overhead 24 The...

-

C13 1-4 ? 1-6. BACTERIAL GROWTH & COMPONENTS OF MACROMOLECULES Suppose you discover a one-foot black and white sphere in Central Park and you suspect it is a new organism. If it really is alive and...

-

Following is information about Fine Furnitures direct labor hours and wages last period. Actual labor hours at the standard price per hour .... $1,680 Actual labor hours at the actual price per hour...

-

Within the context of the planning cycle, the planning that takes place at the highest levels of the firm is called: A. detailed planning and control. B. strategic planning. C. operational planning....

-

Why might a firm use theatre test, on-air test and physiological measure to pretest its finish broadcast ads?

-

Assume that you work for Greebles Department Store, and your manager requests that you outline the pros and cons of discontinuing its hardware department. That department appears to be generating...

-

It is said that "the higher the MARR, the higher the price that a company should be willing to pay for equipment that reduces annual operating expenses." Explain the reasoning behind this statement.

-

Discuss the sequence in which the major components of the master budget are prepared. Why is it necessary to prepare the components in such a sequence?

-

The following book and fair values were available for Westmont Company as of March 1. Book Value Inventory Land Buildings $ 551,500 771,000 1,895,000 Fair Value $ 515,250 1,050,750 Customer...

-

In this exercise, you create an application that allows the user to enter the gender (either F or M) and GPA for any number of students. The application should calculate the average GPA for all...

-

Using relevant theory, describe the team formation and dynamics process in project management. Illustrate with an example showing the beginning and the end of people in a project

-

Data for the Bidwell Company are as follows: Required: a. Based on the preceding data, calculate break-even sales in units. b. If Bidwell Company is subject to an effective income tax rate of 40...

-

Do you use decompositional analyses to understand what behavioral aspects (e.g., frequency, order size) are most strongly associated with these differences?

-

As you perform customer-base audits on an ongoing basis, how do they change as you gain more experience and perspective? Are they simpler or more complex?

-

Before contemplating a full audit, what kinds of basic analyses do you perform with this integrated dataset? What are the first crossover (product customer) questions you seek to answer?

-

Do you seek to know which products tend to be disproportionately favored by high-value customers?

-

Question 3 A cup of strawberry-flavor yoghurt has the weight, which is normally distributed with the mean of 150 grams and the standard deviation of 0.2 grams. A cup of mango-flavor yoghurt has the...

-

Assume you are the accountant for Catalina Industries. John Catalina, the owner of the company, is in a hurry to receive the financial statements for the year ended December 31, 20X1, and asks you...

-

Polyplast is considering purchasing an injection-molding machine for $500,000. This machine will, before considering taxes and depreciation, reduce costs by $108,000 per year. Polyplast's tax rate is...

-

Molly West is developing her retail firm's budget. She provides you with the following budgeted sales data (in units) for the first five months of the year: .....................Sales in Units...

-

Sunglow provides you with the following data for its most recent year of operations: Required: a. Use the high-low method to estimate Sunglow's monthly cost equation. b. Use two observations that are...

-

Caterpillars of the Monarch butterfly eat plants that are toxic to other animals so that their tissues become toxic. Birds that try to eat Monarchs vomit and then avoid the striking orange-and-black...

-

You are eating a salad when you almost bite down on a green insect hidden among the lettuce leaves. The friend who is eating with you says, That would have been gross, but I dont think it would have...

-

Islands tend to have fewer species than an equally sized area of the mainland. Is this consistent with the idea that species were spread around Earth purposefully? Is it consistent with evolution?

Study smarter with the SolutionInn App