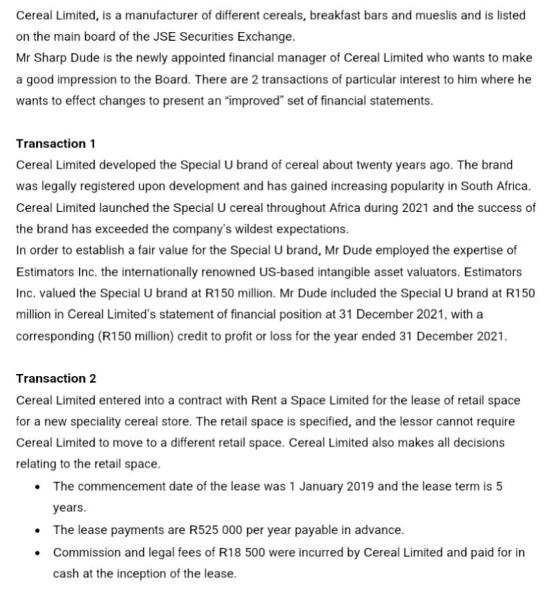

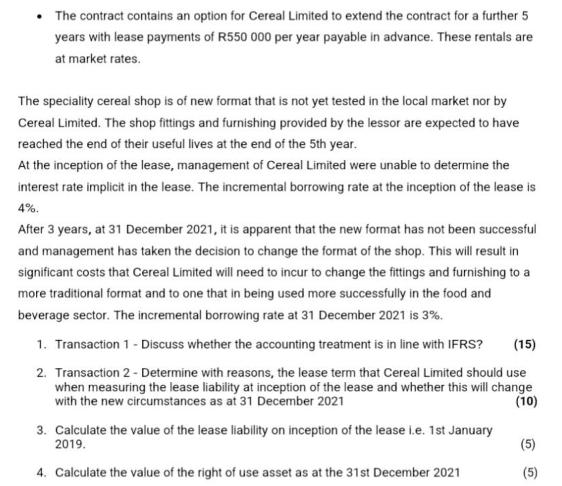

Cereal Limited, is a manufacturer of different cereals, breakfast bars and mueslis and is listed on...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

Cereal Limited, is a manufacturer of different cereals, breakfast bars and mueslis and is listed on the main board of the JSE Securities Exchange. Mr Sharp Dude is the newly appointed financial manager of Cereal Limited who wants to make a good impression to the Board. There are 2 transactions of particular interest to him where he wants to effect changes to present an "improved" set of financial statements. Transaction 1 Cereal Limited developed the Special U brand of cereal about twenty years ago. The brand was legally registered upon development and has gained increasing popularity in South Africa. Cereal Limited launched the Special U cereal throughout Africa during 2021 and the success of the brand has exceeded the company's wildest expectations. In order to establish a fair value for the Special U brand, Mr Dude employed the expertise of Estimators Inc. the internationally renowned US-based intangible asset valuators. Estimators Inc. valued the Special U brand at R150 million. Mr Dude included the Special U brand at R150 million in Cereal Limited's statement of financial position at 31 December 2021, with a corresponding (R150 million) credit to profit or loss for the year ended 31 December 2021. Transaction 2 Cereal Limited entered into a contract with Rent a Space Limited for the lease of retail space for a new speciality cereal store. The retail space is specified, and the lessor cannot require Cereal Limited to move to a different retail space. Cereal Limited also makes all decisions relating to the retail space. • The commencement date of the lease was 1 January 2019 and the lease term is 5 years. • The lease payments are R525 000 per year payable in advance. • Commission and legal fees of R18 500 were incurred by Cereal Limited and paid for in cash at the inception of the lease. • The contract contains an option for Cereal Limited to extend the contract for a further 5 years with lease payments of R550 000 per year payable in advance. These rentals are at market rates. The speciality cereal shop is of new format that is not yet tested in the local market nor by Cereal Limited. The shop fittings and furnishing provided by the lessor are expected to have reached the end of their useful lives at the end of the 5th year. At the inception of the lease, management of Cereal Limited were unable to determine the interest rate implicit in the lease. The incremental borrowing rate at the inception of the lease is 4%. After 3 years, at 31 December 2021, it is apparent that the new format has not been successful and management has taken the decision to change the format of the shop. This will result in significant costs that Cereal Limited will need to incur to change the fittings and furnishing to a more traditional format and to one that in being used more successfully in the food and beverage sector. The incremental borrowing rate at 31 December 2021 is 3%. 1. Transaction 1 - Discuss whether the accounting treatment is in line with IFRS? (15) 2. Transaction 2 - Determine with reasons, the lease term that Cereal Limited should use when measuring the lease liability at inception of the lease and whether this will change with the new circumstances as at 31 December 2021 (10) 3. Calculate the value of the lease liability on inception of the lease i.e. 1st January 2019. 4. Calculate the value of the right of use asset as at the 31st December 2021 (5) Cereal Limited, is a manufacturer of different cereals, breakfast bars and mueslis and is listed on the main board of the JSE Securities Exchange. Mr Sharp Dude is the newly appointed financial manager of Cereal Limited who wants to make a good impression to the Board. There are 2 transactions of particular interest to him where he wants to effect changes to present an "improved" set of financial statements. Transaction 1 Cereal Limited developed the Special U brand of cereal about twenty years ago. The brand was legally registered upon development and has gained increasing popularity in South Africa. Cereal Limited launched the Special U cereal throughout Africa during 2021 and the success of the brand has exceeded the company's wildest expectations. In order to establish a fair value for the Special U brand, Mr Dude employed the expertise of Estimators Inc. the internationally renowned US-based intangible asset valuators. Estimators Inc. valued the Special U brand at R150 million. Mr Dude included the Special U brand at R150 million in Cereal Limited's statement of financial position at 31 December 2021, with a corresponding (R150 million) credit to profit or loss for the year ended 31 December 2021. Transaction 2 Cereal Limited entered into a contract with Rent a Space Limited for the lease of retail space for a new speciality cereal store. The retail space is specified, and the lessor cannot require Cereal Limited to move to a different retail space. Cereal Limited also makes all decisions relating to the retail space. • The commencement date of the lease was 1 January 2019 and the lease term is 5 years. • The lease payments are R525 000 per year payable in advance. • Commission and legal fees of R18 500 were incurred by Cereal Limited and paid for in cash at the inception of the lease. • The contract contains an option for Cereal Limited to extend the contract for a further 5 years with lease payments of R550 000 per year payable in advance. These rentals are at market rates. The speciality cereal shop is of new format that is not yet tested in the local market nor by Cereal Limited. The shop fittings and furnishing provided by the lessor are expected to have reached the end of their useful lives at the end of the 5th year. At the inception of the lease, management of Cereal Limited were unable to determine the interest rate implicit in the lease. The incremental borrowing rate at the inception of the lease is 4%. After 3 years, at 31 December 2021, it is apparent that the new format has not been successful and management has taken the decision to change the format of the shop. This will result in significant costs that Cereal Limited will need to incur to change the fittings and furnishing to a more traditional format and to one that in being used more successfully in the food and beverage sector. The incremental borrowing rate at 31 December 2021 is 3%. 1. Transaction 1 - Discuss whether the accounting treatment is in line with IFRS? (15) 2. Transaction 2 - Determine with reasons, the lease term that Cereal Limited should use when measuring the lease liability at inception of the lease and whether this will change with the new circumstances as at 31 December 2021 (10) 3. Calculate the value of the lease liability on inception of the lease i.e. 1st January 2019. 4. Calculate the value of the right of use asset as at the 31st December 2021 (5) Cereal Limited, is a manufacturer of different cereals, breakfast bars and mueslis and is listed on the main board of the JSE Securities Exchange. Mr Sharp Dude is the newly appointed financial manager of Cereal Limited who wants to make a good impression to the Board. There are 2 transactions of particular interest to him where he wants to effect changes to present an "improved" set of financial statements. Transaction 1 Cereal Limited developed the Special U brand of cereal about twenty years ago. The brand was legally registered upon development and has gained increasing popularity in South Africa. Cereal Limited launched the Special U cereal throughout Africa during 2021 and the success of the brand has exceeded the company's wildest expectations. In order to establish a fair value for the Special U brand, Mr Dude employed the expertise of Estimators Inc. the internationally renowned US-based intangible asset valuators. Estimators Inc. valued the Special U brand at R150 million. Mr Dude included the Special U brand at R150 million in Cereal Limited's statement of financial position at 31 December 2021, with a corresponding (R150 million) credit to profit or loss for the year ended 31 December 2021. Transaction 2 Cereal Limited entered into a contract with Rent a Space Limited for the lease of retail space for a new speciality cereal store. The retail space is specified, and the lessor cannot require Cereal Limited to move to a different retail space. Cereal Limited also makes all decisions relating to the retail space. • The commencement date of the lease was 1 January 2019 and the lease term is 5 years. • The lease payments are R525 000 per year payable in advance. • Commission and legal fees of R18 500 were incurred by Cereal Limited and paid for in cash at the inception of the lease. • The contract contains an option for Cereal Limited to extend the contract for a further 5 years with lease payments of R550 000 per year payable in advance. These rentals are at market rates. The speciality cereal shop is of new format that is not yet tested in the local market nor by Cereal Limited. The shop fittings and furnishing provided by the lessor are expected to have reached the end of their useful lives at the end of the 5th year. At the inception of the lease, management of Cereal Limited were unable to determine the interest rate implicit in the lease. The incremental borrowing rate at the inception of the lease is 4%. After 3 years, at 31 December 2021, it is apparent that the new format has not been successful and management has taken the decision to change the format of the shop. This will result in significant costs that Cereal Limited will need to incur to change the fittings and furnishing to a more traditional format and to one that in being used more successfully in the food and beverage sector. The incremental borrowing rate at 31 December 2021 is 3%. 1. Transaction 1 - Discuss whether the accounting treatment is in line with IFRS? (15) 2. Transaction 2 - Determine with reasons, the lease term that Cereal Limited should use when measuring the lease liability at inception of the lease and whether this will change with the new circumstances as at 31 December 2021 (10) 3. Calculate the value of the lease liability on inception of the lease i.e. 1st January 2019. 4. Calculate the value of the right of use asset as at the 31st December 2021 (5) Cereal Limited, is a manufacturer of different cereals, breakfast bars and mueslis and is listed on the main board of the JSE Securities Exchange. Mr Sharp Dude is the newly appointed financial manager of Cereal Limited who wants to make a good impression to the Board. There are 2 transactions of particular interest to him where he wants to effect changes to present an "improved" set of financial statements. Transaction 1 Cereal Limited developed the Special U brand of cereal about twenty years ago. The brand was legally registered upon development and has gained increasing popularity in South Africa. Cereal Limited launched the Special U cereal throughout Africa during 2021 and the success of the brand has exceeded the company's wildest expectations. In order to establish a fair value for the Special U brand, Mr Dude employed the expertise of Estimators Inc. the internationally renowned US-based intangible asset valuators. Estimators Inc. valued the Special U brand at R150 million. Mr Dude included the Special U brand at R150 million in Cereal Limited's statement of financial position at 31 December 2021, with a corresponding (R150 million) credit to profit or loss for the year ended 31 December 2021. Transaction 2 Cereal Limited entered into a contract with Rent a Space Limited for the lease of retail space for a new speciality cereal store. The retail space is specified, and the lessor cannot require Cereal Limited to move to a different retail space. Cereal Limited also makes all decisions relating to the retail space. • The commencement date of the lease was 1 January 2019 and the lease term is 5 years. • The lease payments are R525 000 per year payable in advance. • Commission and legal fees of R18 500 were incurred by Cereal Limited and paid for in cash at the inception of the lease. • The contract contains an option for Cereal Limited to extend the contract for a further 5 years with lease payments of R550 000 per year payable in advance. These rentals are at market rates. The speciality cereal shop is of new format that is not yet tested in the local market nor by Cereal Limited. The shop fittings and furnishing provided by the lessor are expected to have reached the end of their useful lives at the end of the 5th year. At the inception of the lease, management of Cereal Limited were unable to determine the interest rate implicit in the lease. The incremental borrowing rate at the inception of the lease is 4%. After 3 years, at 31 December 2021, it is apparent that the new format has not been successful and management has taken the decision to change the format of the shop. This will result in significant costs that Cereal Limited will need to incur to change the fittings and furnishing to a more traditional format and to one that in being used more successfully in the food and beverage sector. The incremental borrowing rate at 31 December 2021 is 3%. 1. Transaction 1 - Discuss whether the accounting treatment is in line with IFRS? (15) 2. Transaction 2 - Determine with reasons, the lease term that Cereal Limited should use when measuring the lease liability at inception of the lease and whether this will change with the new circumstances as at 31 December 2021 (10) 3. Calculate the value of the lease liability on inception of the lease i.e. 1st January 2019. 4. Calculate the value of the right of use asset as at the 31st December 2021 (5)

Expert Answer:

Answer rating: 100% (QA)

1 Transaction 1 Discuss whether the accounting treatment is in line with IFRS The accounting treatment for the Special U brand in Transaction 1 does not align with International Financial Reporting St... View the full answer

Related Book For

Business Communication Developing Leaders for a Networked World

ISBN: 978-9814714655

2nd edition

Authors: Peter Cardon

Posted Date:

Students also viewed these accounting questions

-

2. Craig likes to collect records. Last year he had 10 records in his collection. Now he has 14 records. What is the percent increase of his collection?

-

Planning is one of the most important management functions in any business. A front office managers first step in planning should involve determine the departments goals. Planning also includes...

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

In Problem 10.16, we projected financial statements for Walmart Stores for Years +1 through +5. The data in Chapter 12s Exhibits 12.1612.18 include the actual amounts for 2008 and the projected...

-

The tires of a car make 75 revolutions as the car reduces its speed uniformly from to 55 km/s. The tires have a diameter of 0.80 m. (a) What was the angular acceleration of the tires? If the car...

-

The Restatement of the Law of Torts a. has been adopted by all states. b. is frequently cited by the courts. c. is prepared by the courts. d. all of the above.

-

What huge bankruptcy in 2001-2002 caused forensic accountants to become rising stars within the accounting profession?

-

The debits to Work in ProcessRoasting Department for Morning Brew Coffee Company for August 2014, together with information concerning production, are as follows: All direct materials are placed in...

-

p26. On December 31, 2019, Buffalo Wings Co. had outstanding P20 million face value convertible bonds maturing on December 31, 2022. Interest is payable annually on December 31. Each P1,000 bond is...

-

Vollmer Manufacturing makes three components for sale to refrigeration companies. The components are processed on two machines: a shaper and a grinder. The times (in minutes) required on each machine...

-

Discuss American Radiatronics Corporation in terms of organizational effectiveness based on Quinn's model, referring to the four quadrants and the two dimensions (control vs. flexibility and internal...

-

Marco Company shows the following costs for three jobs worked on in April. Job 306 Job 307 Job 308 Balances on March 31 Direct materials used (in March) $ 35,400 Direct labor used (in March) 26,400...

-

David is playing a game where he flips two coins and counts the total number of heads. The possible outcomes and probabilities are shown in the probability distribution below. .50 P(x) Frequency 25 0...

-

Toonces, Inc. has outstanding 600,000 shares of $2 par common stock and 120,000 shares of no-par 6% preferred stock with a stated value of $5. The preferred stock is cumulative and nonparticipating....

-

Calculate the Macaulay duration of a 9%, $1,000 par bond that matures in three years if the bond's YTM is 10% and interest is paid semiannually. You may useAppendix Cto answer the questions....

-

Who are the 12 stakeholders B2B marketers interact with? (5 marks) Define inbound and outbound marketing and give an example of each.(5 marks) Provide one example of how a CRM strategy can improve...

-

List 3 categories of tasks in a division of labor.

-

Read the Forecasting Supply Chain Demand Starbucks Corporation case in your text Operations and Supply Chain Management on pages 484-485, then address the four questions associated with the...

-

A. Each customer should provide their complete purchase information for all refund requests. B. Either Jake or Jen will give you their laptop when its your turn to present. C. Jen gave her...

-

Revise the following sentences to eliminate the phrases it is and there are. A. It is gratifying that General Mills has reduced sugar content in its childrens cereals so that there are fewer children...

-

Read Lea Adamss comments in the Communication Q&A section. Respond to the following questions: A. What does Adams say about finding out the needs of others in the persuasion process? How does she go...

-

The rules of conduct of CAs, CGAs, and CMAs require them to report a breach of the rules of conduct by a member to their profession's disciplinary body. What should they do before making such a...

-

The auditor's working papers usually can be pro vided to someone else only with the permission of the client. What is the rationale for such a rule?

-

Many people believe that a public accountant cannot be truly independent when payment of fees is dependent on the management of the client. Explain a way of reducing this appearance of lack of...

Study smarter with the SolutionInn App