(i) The company made additional sales on 28 December. Both the sales and the cost of goods...

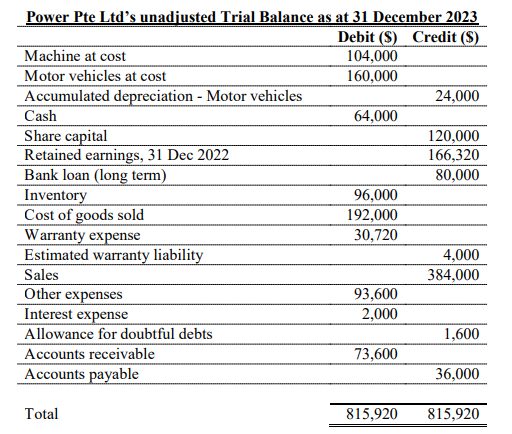

Question:

(i) The company made additional sales on 28 December. Both the sales and the cost of goods sold were not recorded in the accounts. Based on the specific identification cost flow assumption, the value of the ending inventory following the sales should be $56,000 and not $96,000 as shown in the unadjusted trial balance. Power Pte Ltd sets its selling price at the inventory cost plus a markup of 50%. 75% of the sales on 28 December were on credit and the balance were cash sales.

(ii) The company estimated that warranty expenses average 8% of sales.

(iii) The machine that costs $104,000 was acquired on 1 January 2023. This cost includes $2,500 maintenance costs for the year ending 31 December 2023. However, the cost of $500 to transport the machine from the supplier's warehouse to the company's premises at the time of purchase was treated as expense and included in the "Other expenses Account".

(iv) No depreciation has been charged for the year ended 31 December 2023.

• The company depreciates the machine using the straight-line method. The machine is expected to have a residual value of $7,500 at the end of its useful life of 5 years.

• The company depreciates motor vehicles using the double-declining method with an assumed useful life of 4 years and residual value at 10% of the cost.

(v) In the month of December, the company issued from the inventory, parts costing $1,500 to replace defective goods covered under warranty.

(vi) The bank loan carries an annual interest of 5%, payable twice a year on every 30 June and 31 December. As the company has yet to receive the bank statement, the Cash account shown in the unadjusted trial balance has not taken this into account.

(vii) Included in the sales was $3,000 deposit received from a customer in November for goods to be delivered in January 2024.

(viii) Power Pte Ltd estimated that 4% of accounts receivable owing on 31 December 2023 will be uncollectible. Required: Analyse the above and present the necessary entries for Power Pte Ltd for the year ending 31 December 2023.

Expert Answer:

Auditing Cases An Interactive Learning Approach

ISBN: 978-0132423502

4th Edition

Authors: Steven M Glover, Douglas F Prawitt