The CEO of Sweet Holdings Limited recently said the company is targeting growth in the rest of

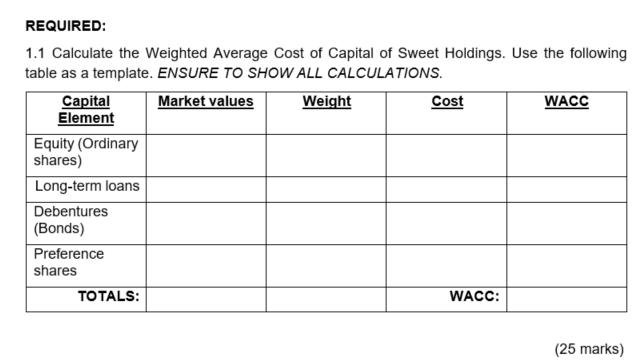

Question:

The CEO of Sweet Holdings Limited recently said ‘the company is targeting growth in the rest of Africa over the next 5 years in an effort to diversify revenue streams across a wider range of geographies. The first project in Africa that Sweet Holdings has identified is located in Namibia. The company has specified that it will raise financing for the project in South Africa. There is more risk associated with the project because the Namibian trading environment is different to the South African trading environment. Therefore, management has to determine the specific weighted average cost of capital that applies to a project of this nature. Information that may assist management with its calculations is set out below.

Additional information on capital structure and the cost of capital:

- Sweet Holdings financial year-end results have recently been released. The company’s reported results include 2.1 million issued ordinary shares and earnings after tax of R5.64 million.

- Sweet Holdings current price/earnings is 13.- Given

- Sweet Holdings recently declared and paid a dividend of R2.10 per ordinary share.

- Maintained a growth rate of 15% per annum in earnings and dividends. This growth rate is sustainable for the foreseeable future.

- The company has a long-term loan with a book value of R10 million. The loan will be repaid in full in three years’ time at a premium of 5%. Similar long-term loans are currently traded in the market at 12% per annum before tax.

- Sweet Holdings has issued 180 000 12% redeemable debentures with a par value of R100 per debenture. These debentures are currently trading at R102 per debenture. The debentures will be redeemed at a premium of 2% in five years’ time.

- Sweet Holdings has 200 000 non-cumulative, non-redeemable preference shares in issue at a nominal value of R80 per share. If market-related dividends were paid, dividends would be R1 800 000. According to the terms of the share, the company may declare R2 000 000 non-cumulative preference dividends in any one year.

- The company tax rate is 28% per year.

Additional information on the Namibian project:

Sweet Holdings Limited is planning a new resort with 20 units.

The research and development department have given the following estimates:

- The proposed rental is R4 000 per unit per eve.

- Expected occupancy for the first year is fifty percent increasing to eighty percent for the following five years.

- Due to the highly demanding international tourism, Sweet Holdings only budgets on five years per resort at the capital budgeting stage.

- The costs associated with the new resort are:

- Additional working capital will initially amount to R1 000 000.

- The total amount of capital required is R10 000 000 that will be used for the construction of buildings and the purchase of game and equipment. The residual value of the assets should be R3 000 000 at the end of the five years. The assets are not sold at the end of the five years.

- The direct cost per night per unit is R1 500 which is only incurred if the unit is occupied. Fixed costs, excluding employee costs of R7 million per annum will also be incurred.

- The new resort will be built on land that is currently rented out at R500 000 per year.

- A number of staff will be transferred from another resort and will continue receiving their current salaries totaling R1 500 000 per annum. If the project does not go ahead, the employees will be retrenched from their current position and retrenchment costs of R2 000 000 will be incurred.

- General head office overheads of R130 000 will be allocated to the project should it go ahead.

Expert Answer:

11 The weighted average cost of capital WACC is the rate that a company is expected to pay on averag... View the full answer

Managerial Accounting

ISBN: 978-0176223311

1st Canadian Edition

Authors: Karen Wilken Braun, Wendy Tietz, Walter Harrison, Rhonda Pyp