You are given a portfolio of three assets whose returns are jointly normally distributed with the following

Question:

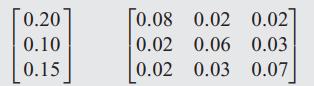

You are given a portfolio of three assets whose returns are jointly normally distributed with the following mean vector and covariance matrix:

(a) Compute the 95% VaR for the portfolio if we invest $1 in the first asset, $2 in the second asset, and $3 in the third asset.

(b) How much does each asset’s holding contribute to the overall VaR risk?

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Let the mean vector of returns be and the covariance matrix be denoted Let the vector o...View the full answer

Answered By

Pardeep Kumar

I have a degree in criminology and Criminal Justice, and currently pursuing an MA in Criminology from a reputable institution. I have lectured students before, after which I started to follow my writing passion. That is, for over the past 5 years, I've helped many clients accomplish their writing needs. I'm an experienced academic writer, essay writer, and blogger. Besides, I am an online tutor and homework helper.

0 Reviews

10+ Question Solved

Related Book For

Question Posted: