Question: A bank has the following balance sheet: Suppose interest rates rise such that the average yield on rate- sensitive assets increases by 45 basis points

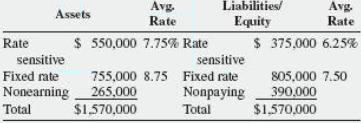

A bank has the following balance sheet:

Suppose interest rates rise such that the average yield on rate- sensitive assets increases by 45 basis points and the average yield on rate- sensitive liabilities increases by 35 basis points.

a. Calculate the bank’s repricing GAP and percentage gap.

b. Assuming the bank does not change the composition of its balance sheet calculate the resulting change in the bank’s interest income, interest expense, and net interest income?

c. Explain how the CGAP and spread effects influenced the change in net interest income.

Avg. Rate Liabilities Equity Avg. Rate Assets Rate $ 550,000 7.75% Rate $ 375,000 6.25% sensitive Fixed rate 755.000 8.75 Fixed rate 805,000 7.50 Nonearning 265,000 Total sensitive Nonpaying 390.000 $1,570,000 $1570,000 Total

Step by Step Solution

3.42 Rating (171 Votes )

There are 3 Steps involved in it

a Repricing GAP 550000 375000 175000 Percentage Gap 175... View full answer

Get step-by-step solutions from verified subject matter experts

Document Format (1 attachment)

403-B-B-F-M (1961).docx

120 KBs Word File