Question: Consider estimation of the following two equation model: y1 = 1 + 1, y2 = 2x + 2. A sample of 50 observations produces the

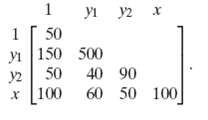

Consider estimation of the following two equation model: y1 = β1 + ε1, y2 = β2x + ε2. A sample of 50 observations produces the following moment matrix:

a. Write the explicit formula for the GLS estimator of [β1, β2].What is the asymptotic covariance matrix of the estimator?

b. Derive the OLS estimator and its sampling variance in this model.

c. Obtain the OLS estimates of β1 and β2, and estimate the sampling covariance matrix of the two estimates. Use n instead of (n ?? 1) as the divisor to compute the estimates of the disturbance variances

d. Compute the FGLS estimates of β1 and β2 and the estimated sampling covariance matrix.

e. Test the hypothesis that β2 = 1.

y y2 x 1 50 1 |150 500 32 50 x 100 40 90 60 50 100

Step by Step Solution

3.34 Rating (172 Votes )

There are 3 Steps involved in it

The model is y The generalized least squares estimator is B xxxly 022 12x The two elements are B 012 x 11xx xnx XB The asymptotic covariance matrix is ... View full answer

Get step-by-step solutions from verified subject matter experts

Document Format (1 attachment)

3-M-E-E-A (99).docx

120 KBs Word File