Question: This exercise is based on the following data set. a. Compute the ordinary least squares regression of Y on a constant, X1, and X2. Be

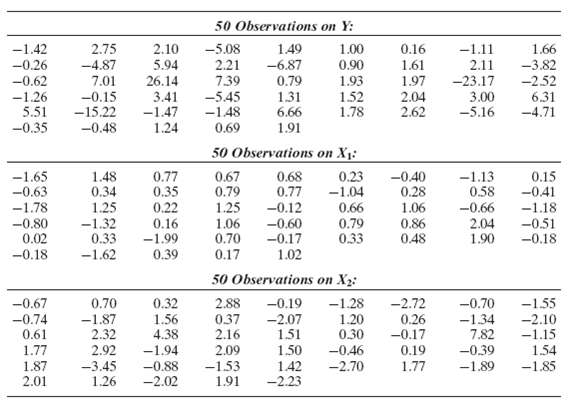

This exercise is based on the following data set.

a. Compute the ordinary least squares regression of Y on a constant, X1, and X2. Be sure to compute the conventional estimator of the asymptotic covariance matrix of the OLS estimator as well.

b. Compute the White estimator of the appropriate asymptotic covariance matrix for the OLS estimates.

c. Test for the presence of heteroscedasticity using White??s general test. Do your results suggest the nature of the heteroscedasticity?

d. Use the Breusch??Pagan Lagrange multiplier test to test for heteroscedasticity.

e. Sort the data keying on X1 and use the Goldfeld??Quandt test to test for heteroscedasticity. Repeat the procedure, using X2. What do youfind?

-1.42 2.75 -0.26 -4.87 -0.62 7.01 26.14 -1.26 -0.15 3.41 5.51 -15.22 -1.47 -0.35 -0.48 1.24 -1.65 -0.63 -1.78 -0.80 0.02 -0.18 -0.67 -0.74 0.61 1.77 1.87 2.01 2.10 5.94 1.48 0.77 0.34 0.35 1.25 0.22 -1.32 0.33 -1.62 0.70 -1.87 2.32 2.92 -3.45 1.26 0.16 -1.99 0.39 0.32 1.56 4.38 -1.94 -0.88 -2.02 50 Observations on Y: -5.08 1.00 2.21 0.90 7.39 1.93 1.52 1.78 -5.45 -1.48 0.69 1.49 -6.87 0.79 1.31 1.06 0.70 0.17 6.66 1.91 50 Observations on X: 0.67 0.23 0.79 -1.04 1.25 0.68 0.77 -0.12 -0.60 -0.17 1.02 0.66 0.79 0.33 50 Observations on X: 2.88 -0.19 -1.28 0.37 -2.07 1.20 2.16 1.51 0.30 2.09 1.50 -0.46 -1.53 1.42 -2.70 1.91 -2.23 0.16 1.61 1.97 2.04 2.62 -0.40 0.28 1.06 0.86 0.48 -2.72 0.26 -0.17 0.19 1.77 -1.11 2.11 -23.17 3.00 -5.16 -1.13 0.58 -0.66 2.04 1.90 1.66 -3.82 -2.52 6.31 -4.71 0.15 -0.41 -1.18 -0.51 -0.18 -0.70 -1.55 -1.34 -2.10 7.82 -1.15 -0.39 1.54 -1.89 -1.85

Step by Step Solution

3.44 Rating (167 Votes )

There are 3 Steps involved in it

The ordinary least squares regression of Y on a constant X and X produces the following results Sum of squared residuals 19119275 R2 Standard error of regression Variable Coefficient 190394 113113 376... View full answer

Get step-by-step solutions from verified subject matter experts

Document Format (1 attachment)

3-M-E-E-A (74).docx

120 KBs Word File