Question: Stephanie Waldron is an aggressive individual whose career as a self-employed management consultant has blossomed. Waldron is both willing and able to bear substantial risk

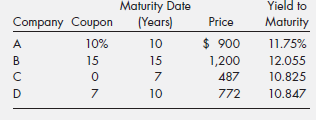

Stephanie Waldron is an aggressive individual whose career as a self-employed management consultant has blossomed. Waldron is both willing and able to bear substantial risk in order to earn a higher return. She is also very independent, preferring to make her own investment decisions after considering various alternatives. She has a Keogh account that she manages herself. Although she could select various types of mutual funds as investment vehicles for the account, she prefers to select specific assets. The account's value exceeds $200,000, and Waldron recently liquidated several securities whose prices had risen sufficiently so that she believed further price increases to be unlikely. As her financial planner, you believe that high-yield debt instruments would be an attractive alternative to stocks, whose prices have risen recently. High-yield securities offer larger returns but may involve substantial risk. The combination of high risk and high return are consistent with Waldron's investment philosophy, so she has asked you to suggest several alternative high-yield bonds. The terms of several B-rated bonds are as follows:

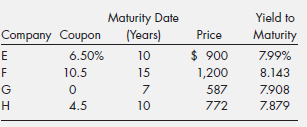

Waldron is interested in each of the bonds but has several questions concerning their risk. Since each bond has the same rating, it seems reasonable to conclude that the probability of default is about the same for each bond. However, there may be considerable difference in their price volatility. Waldron has asked you to rank each bond from the least to the most price volatile. She also wants you to compare the bonds' price volatility with the triple-A-rated bonds with the same terms to maturity. To do this, you have found four triple-A-rated bonds with the following terms:

If interest rates rise by 3 percent across the board, what will be the new price of each of the eight bonds? What do these new prices suggest about the price volatility of high-yield versus high-quality bonds? To answer this last question, compare bond A to bond E, B to F, C to G, and D to H. Which bonds' prices were more volatile? If two bonds with the same term to maturity sell for the same price, which bond may subject the investor to more interest rate risk? Does acquiring bonds with higher credit ratings and less default risk also imply the investor has less interest raterisk?

Maturity Date Yield to Company Coupon A B Price (Years) Maturity 11.75% 12.055 10.825 $ 900 1,200 487 10% 15 10 15 D 10 772 10.847

Step by Step Solution

3.40 Rating (163 Votes )

There are 3 Steps involved in it

To compare the price volatility compute each bonds duration Brated Coupon Price Yield to Duration Ra... View full answer

Get step-by-step solutions from verified subject matter experts

Document Format (1 attachment)

124-B-C-F-I-S (162).docx

120 KBs Word File