KC Restaurants Ltd., a Canadian-controlled private corporation, was incorporated on July 1, 20X0, and began operations immediately.

Question:

KC Restaurants Ltd., a Canadian-controlled private corporation, was incorporated on July 1, 20X0, and began operations immediately. By December 31, 20X0 (the corporation’s first year end), three new restaurants had been opened, two of which were franchises.

During the first few months of operations, the following expenditures were made by KCR:

Legal fees for the cost of incorporation……………………………… $ 4,000

Cooking equipment, including food processors, ovens, and hot plates.. 320,000

Franchise #1……………………………………………………………. 40,000

Franchise #2 …………………………………………………. 80,000

Cutlery, plates, glasses, and cups…………………………………… 115,000

Computer programs for restaurant accounting ………………………… 3,000

Building (constructed after March 18, 2007) ……………………… 222,000

Franchise #1 was purchased on October 1, 20X0, and will expire after 120 months. Franchise #2, which was acquired on July 1, 20X0, has no expiry date and will continue indefinitely, provided that the terms of the franchise agreement are met. Other equipment, such as tables and chairs, was leased.

For the taxation year ending December 31, 20X0, KCR claimed a deduction for the maximum available CCA and cumulative eligible capital account. For tax purposes, after these deductions were made, the company lost $40,000 in 20X0.

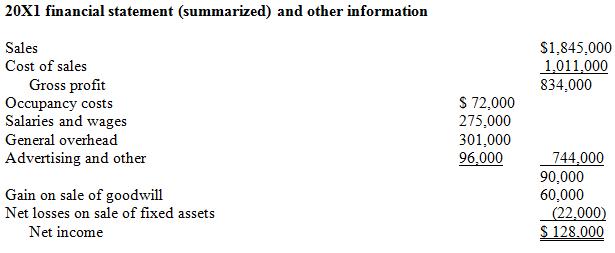

The company became profitable in 20X1. A summary of the income statement prepared for accounting purposes for the year ended December 31, 20X1, with additional information, is provided below.

The following additional information relates to the previous 20X1 financial statements:

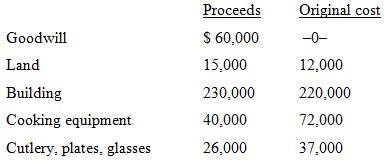

1. On December 1, 20X1, KCR sold the non-franchised restaurant. The sale price included these proceeds:

2. Included in advertising expenses is $2,000 of donations made to a registered charity.

3. Salaries include an accrued bonus of $12,000 awarded on December 31, 20X1, to a manager. The bonus will be paid in three equal instalments of $4,000 on April 30, 20X2, August 31, 20X2, and December 31, 20X2.

4. Expenses include accounting amortization/depreciation of $102,000.

Required:

1. Calculate the undepreciated capital cost for tax purposes for each class of depreciable property at the end of the 20X0 taxation year after CCA claims for that year. (Assume assets purchased in 20X0 were purchased after 2014.)

2. Calculate the balance in the cumulative eligible capital account at the end of the 20X0 taxation year after the deduction for that year.

3. For the taxation year ended December 31, 20X1, calculate KCR’s net income for tax purposes. Begin your answer with net income per the financial statement, and add or subtract adjustments.

Step by Step Answer:

Part 1 CCA 20X0 The company has a short year end and the CCA must be reduced accordingly Reg 11003 T...View the full answer

Canadian Income Taxation Planning And Decision Making

ISBN: 9781259094330

17th Edition 2014-2015 Version

Authors: Joan Kitunen, William Buckwold