On July 1, 2013, the FHLMC 30-Year Generic 4% 2012 was analyzed using the Monte Carlo valuation

Question:

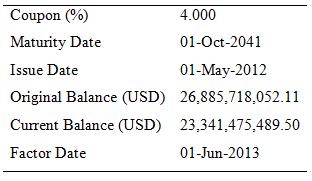

On July 1, 2013, the FHLMC 30-Year Generic 4% 2012 was analyzed using the Monte Carlo valuation model of FactSet. At the time of the analysis the security’s price was 104.644 with accrued interest of 0.300 (per $100 par value). Summary information about the security is as follows:

The results of a simulation using 200 interest-rate path are reproduced as follows:

YTM (%) | 2.981 |

Average Life | 5.307 |

Modified Duration | 4.551 |

Effective Duration | 4.135 |

Effective Convexity | –1.905 |

Partial Duration—6 Month | –0.088 |

Partial Duration—1 Year | 0.097 |

Partial Duration—2 Year | 0.516 |

Partial Duration—5 Year | 1.500 |

Partial Duration—10 Year | 1.806 |

Partial Duration—30 Year | 0.304 |

Spread Duration | 4.338 |

Spread (TRSY) | 1.585 |

Z-Spread | 97.232 |

OAS (TRSY) | 95.158 |

OAS (Libor) | 77.909 |

Projected CPR (PB WAVG) | 14.870 |

Projected PSA (PB WAVG) | 278.342 |

(a) Explain the meaning of each of the measures above.

(b) Given the computed convexity measure, how is this pass-through security expected to perform compared to a comparable Treasury security if the term structure of Treasury rates decreases substantially in a parallel fashion?

Step by Step Answer:

a YTM is the percentage rate of return paid on a bond note or other fixed income security if the investor buys and holds it to its maturity date The calculation for YTM is based on the coupon rate len...View the full answer