Question:

Playfair Sports Ltd. is authorized to issue $6,000,000 of 5-percent, 10-year bonds. On January 2, 2014, the contract date, when the market interest rate is 6 percent, the company issues $4,800,000 of the bonds and receives cash of $4,442,941. Interest is paid on June 30 and December 31 each year. Playfair Sports Ltd. amortizes bond discounts by the effective interest method.

Required

1. Prepare an amortization table for the first four semiannual interest periods. Follow the format of Panel B in Exhibit 15-4 on page 931.

2. Record the issue of bond on January 2, the first semiannual interest payment on June 30, and the second payment on December 31.

3. Show the balance sheet presentation of the bond on the date of issue.

Balance Sheet

Balance sheet is a statement of the financial position of a business that list all the assets, liabilities, and owner’s equity and shareholder’s equity at a particular point of time. A balance sheet is also called as a “statement of financial...

Transcribed Image Text:

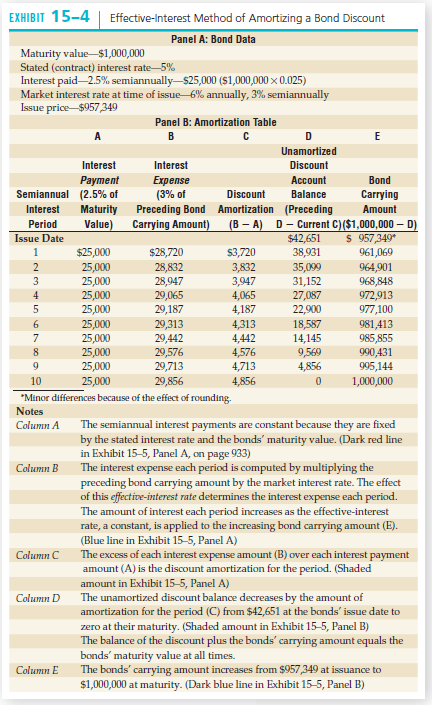

EXHIBIT 15-4 | Effective-Interest Method of Amortizing a Bond Discount Panel A: Bond Data Maturity value-$1,000,000 Stated (contract) interest rate-5% Interest paid 2.5% semiannually$25,000 (S1,000,000 x 0.025) Market interest rate at time of issue- 6% annually, 3% semiannually Issue price $957,349 Panel B: Amortization Table в Unamortized Interest Interest Discount Payment Semiannual (2.5% of Expense (3% of Preceding Bond Amortization Carrying Amount) Account Bond Discount Balance Carrying Interest Maturity (Preceding D- Current C)($1,000,000 – D) $42,651 38,931 35,099 31,152 27,087 22,900 18,587 14,145 9,569 4,856 Amount (B – A) Period Value) $ 957,349* 961,069 964,901. 968,848 972,913 977,100 981,413 985,855 990,431 995,144 1,000,000 Issue Date $3,720 $25,000 $28,720 28,832 28,947 29,065 29,187 25,000 25,000 25,000 25,000 3,832 3,947 4,065 4,187 4,313 4,442 4 25,000 29,313 29,442 29,576 29,713 29,856 25,000 25,000 25,00 4,576 4,713 4,856 *Minor differences because of the effect of rounding. 9. 10 25,000 Notes The semiannual interest payments are constant because they are fixed by the stated interest rate and the bonds' maturity value. (Dark red line in Exhibit 15-5, Panel A, on page 933) The interest expense each period is computed by multiplying the Column A Column B preceding bond carrying amount by the market interest rate. The effect of this effective-interest rate determines the interest expense each period. The amount of interest each period increases as the effective-interest rate, a constant, is applied to the increasing bond carrying amount (E). (Blue line in Exhibit 15-5, Panel A) The excess of each interest expense amount (B) over each interest payment amount (A) is the discount amortization for the period. (Shaded Column C amount in Exhibit 15–5, Panel A) The unamortized discount balance decreases by the amount of amortization for the period (C) from $42,651 at the bonds' issue date to zero at their maturity. (Shaded amount in Exhibit 15-5, Panel B) The balance of the discount plus the bonds' carrying amount equals the bonds' maturity value at all times. The bonds' carrying amount increases from $957,349 at issuance to $1,000,000 at maturity. (Dark blue line in Exhibit 15-5, Panel B) Column D Column E