On April 1, 2013, Abbots acquired all the issued common shares (cum div.) of Evion for $100,000.

Question:

On April 1, 2013, Abbots acquired all the issued common shares (cum div.) of Evion for $100,000. At that date, relevant balances in the records of Evion were:

Share capital ……………….. $80,000

Retained earnings ………… 10,000

Dividend payable ………….. 4,000

All the identifiable assets and liabilities of Evion were recorded at fair value except for the following:

The plant was expected to have a further fi ve-year life. All the inventory on hand at April 1, 2013, was sold by the end of the financial year.

At April 1, 2013, Evion had recorded goodwill of $2,000. As a result of an impairment test on March 31, 2014, Evion wrote goodwill down by $1,500 in its books.

The dividend payable was subsequently paid in June 2013.

During the period ending March 31, 2014, intragroup sales consisted of $40,000 from Abbots to Evion at a profit to Abbots of $10,000. These were all sold to external entities by Evion for $42,000 before March 31, 2014.

Evion also sold some inventory to Abbots for $10,000. This had cost Evion $6,000. Abbots since has sold all the items to external entities for $8,000, except one batch on which Evion recorded a $500 profit before tax (original cost to Evion was $1,000).

On October 1, 2013, Abbots sold an item, regarded by Abbots as a non-current asset, to Evion. At the time of sale, the item’s carrying amount to Abbots was $28,000, and it was sold to Evion for $30,000. Abbots was using a 10% p.a. depreciation rate applied to cost.

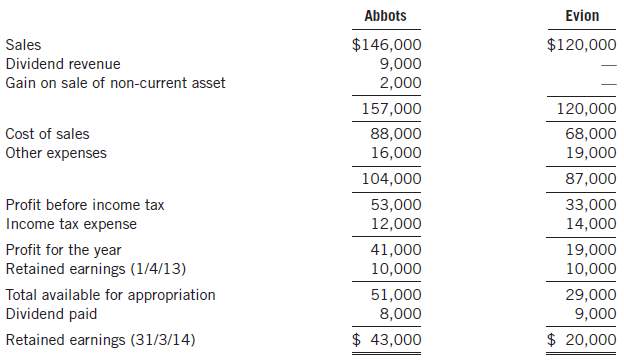

The following information was obtained from the companies for the year ended March 31, 2014:

Required

Prepare the consolidated statement of comprehensive income as at March 31, 2014. Assume a tax rate of 40%.

Goodwill is an important concept and terminology in accounting which means good reputation. The word goodwill is used at various places in accounting but it is recognized only at the time of a business combination. There are generally two types of...

Step by Step Answer:

On April 1 2013 Abbots acquired the shares of Evion Consideration transferred 96000 Cash 100000 Dividend payable 4000 Net fair value of identifiable assets and liabilities of Evion 90000 Share capital ...View the full answer