Refer to the preceding facts for Parsons acquisition of Solar common stock. Parson uses the simple equity

Question:

Refer to the preceding facts for Parson’s acquisition of Solar common stock. Parson uses the simple equity method to account for its investment in Solar. During 2017, Solar sells $40,000 worth of merchandise to Parson. As a result of these intercompany sales, Parson holds beginning inventory of $16,000 and ending inventory of $10,000 of merchandise acquired from Solar. At December 31, 2017, Parson owes Solar $8,000 from merchandise sales. Solar has a gross profit rate of 30%.

During 2017, Parson sells $60,000 worth of merchandise to Solar. Solar holds $15,000 of this merchandise in its ending inventory. Solar owes $10,000 to Parson as a result of these intercompany sales. Parson has a gross profit rate of 40%.

On January 1, 2015, Parson sells equipment having a net book value of $50,000 to Solar for $80,000. The equipment has a 5-year useful life and is depreciated using the straight-line method.

On January 1, 2017, Solar sells equipment to Parson at a profit of $25,000. The equipment has a 5-year useful life and is depreciated using the straight-line method.

Neither company has provided for income tax. The companies qualify as an affiliated group and, thus, will file a consolidated tax return based on a 40% corporate tax rate. The original purchase is not a nontaxable exchange.

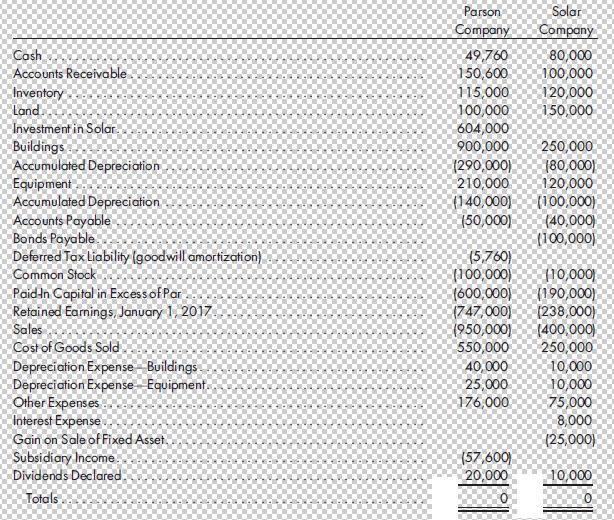

On December 31, 2017, Parson and Solar have the following trial balances:

Required

1. Prepare a determination and distribution of excess schedule.

2. Prepare a consolidated worksheet for the year ended December 31, 2017. Include a provision for income tax and income distribution schedules.

Preceding Facts for Parson's Acquisition:

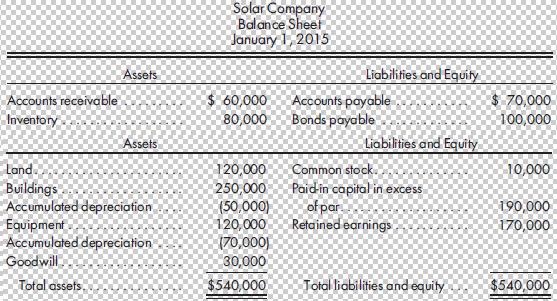

On January 1, 2015, Parson Company acquires an 80% interest in Solar Company for $500,000. Solar had the following balance sheet on the date of acquisition:

Buildings, which have a 20-year life, are undervalued by $70,000. Equipment, which has a 5-year life, is undervalued by $50,000. Any remaining excess of cost over book value is attributable to goodwill, which has a 15-year life for tax purposes only.

Step by Step Answer:

Answer Excess Purchase Price ExcessPurchasePrice PurchasepricepaidbyParson BookvalueofSolarsnetassets ExcessPurchasePricePurchasepricepaidbyParsonBook...View the full answer

Advanced Accounting

ISBN: 978-1305084858

12th edition

Authors: Paul M. Fischer, William J. Tayler, Rita H. Cheng