Refer to the preceding facts for Purples acquisition of Salmon common stock. On January 1, 2016, Salmon

Question:

Refer to the preceding facts for Purple’s acquisition of Salmon common stock. On January 1, 2016, Salmon held merchandise sold to it by Purple for $14,000. This beginning inventory had an applicable gross profit of 40%. During 2016, Purple sold merchandise to Salmon for $60,000. On December 31, 2016, Salmon held $12,000 of this merchandise in its inventory. This ending inventory had an applicable gross profit of 35%. Salmon owed Purple $8,000 on December 31 as a result of this intercompany sale.

Purple held $12,000 worth of merchandise in its beginning inventory from sales from Salmon. This beginning inventory had an applicable gross profit of 25%. During 2016, Salmon sold merchandise to Purple for $30,000. Purple held $16,000 of this inventory at the end of the year. This ending inventory had an applicable gross profit of 30%. Purple owed Salmon $6,000 on December 31 as a result of this intercompany sale.

On January 1, 2015, Purple sold equipment to Salmon at a profit of $40,000. Depreciation on this equipment is computed over an 8-year life using the straight-line method.

On January 1, 2016, Salmon sold equipment with a book value of $30,000 to Purple for $54,000. This equipment has a 6-year life and is depreciated using the straight-line method.

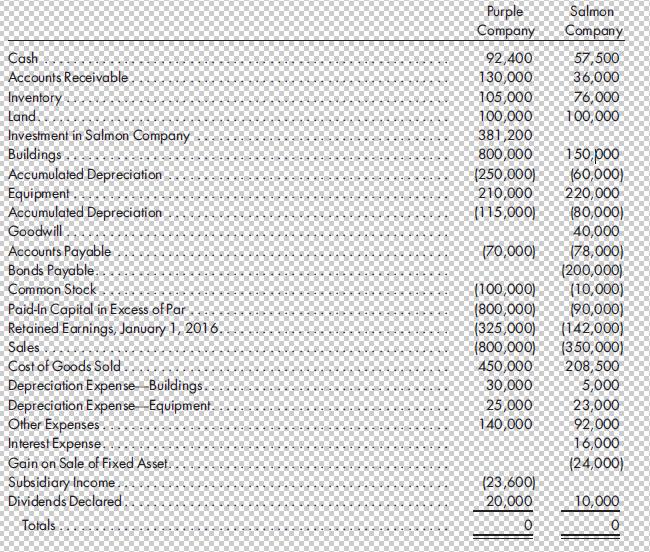

Purple and Salmon had the following trial balances on December 31, 2016:

Required

1. Prepare a value analysis and a determination and distribution of excess schedule for the investment in Salmon.

2. Complete a consolidated worksheet for Purple Company and its subsidiary Salmon Company as of December 31, 2016. Prepare supporting amortization and income distribution schedules.

Preceding Facts For Packard's Acquisition:

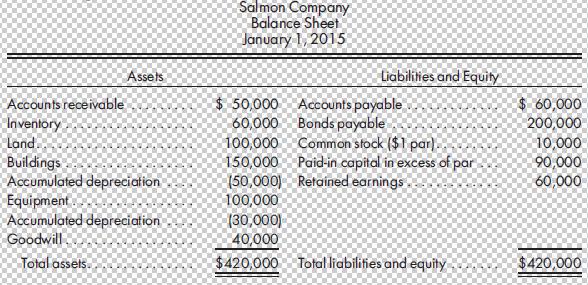

On January 1, 2015, Purple Company acquired Salmon Company. Purple paid $300,000 for 80% of Salmon’s common stock. On the date of acquisition, Salmon had the following balance sheet:

Buildings, which have a 20-year life, are understated by $100,000. Equipment, which has a 5-year life, is understated by $50,000. Any remaining excess is goodwill. Purple uses the simple equity method to account for its investment in Salmon.

Step by Step Answer:

To begin with step 1 Analyzing Value and Calculating the Excess Schedule for the Salmon Investment First figure out how much of Salmons net assets Pur...View the full answer

Advanced Accounting

ISBN: 978-1305084858

12th edition

Authors: Paul M. Fischer, William J. Tayler, Rita H. Cheng