Auditors are required to understand the client?s industry and business but may not be experts in identifying

Question:

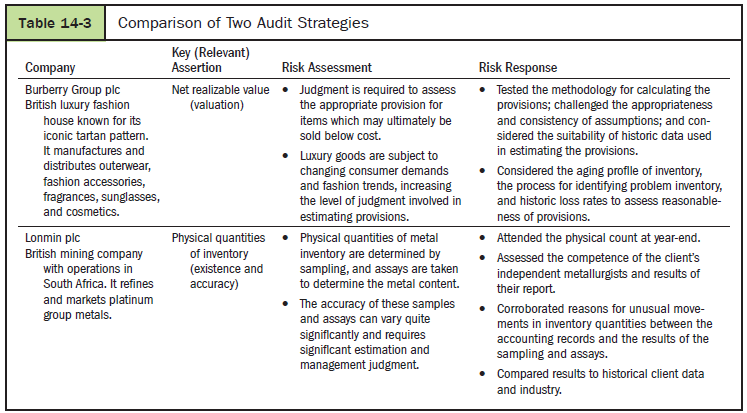

Auditors are required to understand the client?s industry and business but may not be experts in identifying the quantity and value of certain inventory items. For example, with regards to the audit strategy of Lonmin Mines (see Table 14-3, the auditor relied upon the work of a specialist to determine the existence of inventory. Auditing standards provide guidance on whether and how an auditor can rely on a specialist. Refer to CAS 620, Using the Work of an Auditor?s Expert, to answer the following questions.

a. List three examples of inventory items for which an auditor may need to use a specialist for testing existence and valuation, or both. How would an auditor use a specialist in each example?

b. What characteristics should the auditor consider to ensure the specialist is qualified?

c. Does the specialist need to be independent of the client and the auditor?

Table 14-3

Step by Step Answer:

a There are many types of inventory items for which auditors may need to use a specialist for testing existence or valuation including oil and gas res...View the full answer

Auditing The Art and Science of Assurance Engagements

ISBN: 978-0134613116

14th Canadian edition

Authors: Alvin A. Arens, Randal J. Elder, Mark S. Beasley, Joanne C. Jones