Question: When identifying key process risks that could reduce the likelihood of achieving process objectives and impact the likelihood that transactions generated within the process could

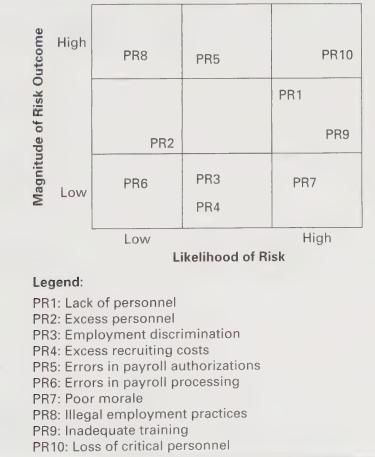

When identifying key process risks that could reduce the likelihood of achieving process objectives and impact the likelihood that transactions generated within the process could be misstated, why should the auditor consider both the likelihood and impact of the inherent risk? After assessing the inherent risks (e.g., by plotting them on a graph similar to what is shown in Figure 6-8), how should the auditor determine which risks should be incorporated into the audit?

Figure 6-8

Magnitude of Risk Outcome High PR8 PR5 PR1 PR2 PR3 PR6 PR7 Low PR4 Low High Likelihood of Risk Legend: PR1: Lack of personnel PR2: Excess personnel PR3: Employment discrimination PR4: Excess recruiting costs PR5: Errors in payroll authorizations PR6: Errors in payroll processing PR7: Poor morale PR8: Illegal employment practices PR9: Inadequate training PR10: Loss of critical personnel PR10 PR9

Step by Step Solution

3.45 Rating (168 Votes )

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts