Question: As an example, we can use the same short time series we used to demonstrate how to use moving averages, to create forecasts using Browns

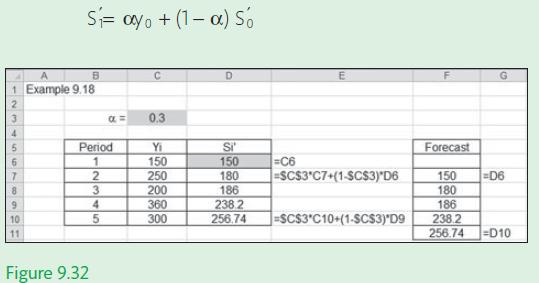

As an example, we can use the same short time series we used to demonstrate how to use moving averages, to create forecasts using Brown’s exponential smoothing method, as illustrated in Figure 9.32. To start the smoothing process the data analyst must make a choice for the smoothing constant α and the initial estimate of S’0. The value of S’0 is needed to determine the smoothed statistic for S’0.

Applying simple exponential smoothing In this example, we have chosen α = 0.3 and S′0 = y1=150.

B 1 Example 9.18 2 3 4 5 6 7 Si ayo+(1-a) So 8 9 10 11 Period 1 2 Figure 9.32 a= 3 4 5 C 0.3 Yi 150 250 200 360 300 D Si' 150 180 186 238.2 256.74 =C6 E -SC$3*C7+(1-SC$3)*D6 =SC$3*C10+(1-SCS3)*D9 Forecast 150 =D6 180 186 238.2 256.74 -D10

Step by Step Solution

3.51 Rating (154 Votes )

There are 3 Steps involved in it

Excel solution Cell C3 Period Cells B6B1... View full answer

Get step-by-step solutions from verified subject matter experts