Assume that you have been given the following information on Fiore Industries: Using the BlackScholes Option Pricing

Question:

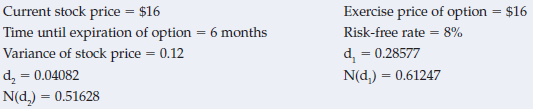

Using the Black€“Scholes Option Pricing Model, what is the value of the option?

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

P 16 X 16 t 05 r RF 008 2 012 d 1 028577 d 2 004082 Nd ...View the full answer

Answered By

Shem John

I’m Shem. I’m a highly experienced tutor with a deep background in mathematics, the sciences, and the humanities. For over five years I have been a trusted guide to many students as they navigate the academic world. With a bachelor's degree in Industrial Chemistry with Management, I can edit your research paper, dissertation, or other piece of scientific writing to prepare it for publication. Through my extensive understanding of the English language, academic and professional writing, as well as the experience I have had in developing curricula regarding academic and professional writing, my skill set is dynamic, dependable, and expansive. As an independent chemist, I have provided literature references and explained chemical calculations to entrepreneurs with scientifically based products. I am also experienced in numerous types of data analysis and fluent in R, Python, Tableau,SPSS, STATA, Excel VBA and Matlab programming. I am very responsive, an excellent communicator and collaborator. I am easy to work with, good-natured, down to the details, good with time management, an independent and self-motivated worker, reasonable, down-to-Earth, and I aim to never disappoint!

0 Reviews

10+ Question Solved

Related Book For

Fundamentals of Financial Management

ISBN: 978-1337395250

15th edition

Authors: Eugene F. Brigham, Joel F. Houston

Question Posted: