Consider the following two-factor model for the returns of three securities. Assume that the factors and epsilons

Question:

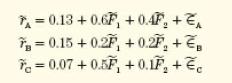

Consider the following two-factor model for the returns of three securities.

Assume that the factors and epsilons have means of zero. Also, assume the factors have variances of 0.1 and are uncorrelated with each other.

If ![]() what are the variances of the returns of the three securities, as well as the covariances and correlations between them?

what are the variances of the returns of the three securities, as well as the covariances and correlations between them?

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Susan Juma

I'm available and reachable 24/7. I have high experience in helping students with their assignments, proposals, and dissertations. Most importantly, I'm a professional accountant and I can handle all kinds of accounting and finance problems.

15+ Reviews

45+ Question Solved

Related Book For

Corporate Finance

ISBN: 9780077173630

3rd Edition

Authors: David Hillier, Stephen A. Ross, Randolph W. Westerfield, Bradford D. Jordan, Jeffrey F. Jaffe

Question Posted: