Question: (Convert variable to absorption) Jenny Lowe started a new business in 1996 to produce portable, climate-controlled shelters. The shelters have many applica tions in special

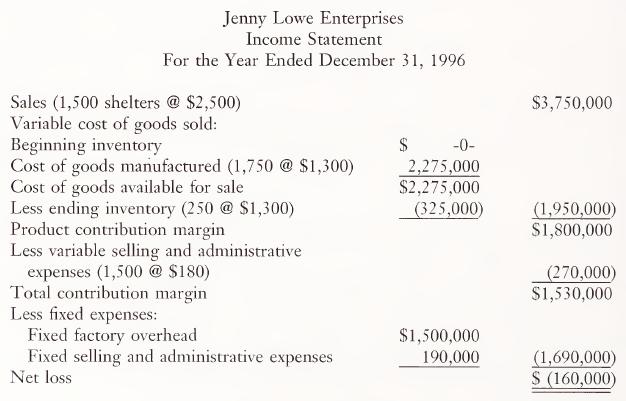

(Convert variable to absorption) Jenny Lowe started a new business in 1996 to produce portable, climate-controlled shelters. The shelters have many applica¬ tions in special events and sporting activities. Jenny’s accountant prepared the following variable costing income statement after the first year to help her in making decisions.

During the year, the following variable production costs per unit were recorded: direct material, $800; direct labor, $300; and overhead, $200.

Ms. Lowe was upset about the net loss because she had wanted to borrow funds to expand capacity. Her friend who teaches accounting at a local university suggested that the use of absorption costing could change the picture.

a. Prepare an absorption costing pretax income statement.

b. Explain the source of the difference between the net income and the net loss figures under the two costing systems.

c. Would it be appropriate to present an absorption costing income statement to the local banker in light of Ms. Lowe’s knowledge of the net loss deter¬ mined under variable costing? Explain.

d. Assume that during the second year of operations, Ms. Lowe’s company produced 1,750 shelters, sold 1,850, and experienced the same total fixed costs. 1. Prepare a variable costing pretax income statement. 2. Prepare an absorption costing pretax income statement. 3. Explain the difference between the incomes for the second year under the two systems.

LO1

Jenny Lowe Enterprises Income Statement For the Year Ended December 31, 1996 Sales (1,500 shelters @ $2,500) $3,750,000 Variable cost of goods sold: Beginning inventory $ -0- Cost of goods manufactured (1,750 @ $1,300) 2,275,000 Cost of goods available for sale $2,275,000 Less ending inventory (250 @ $1,300) (325,000) Product contribution margin (1,950,000) $1,800,000 Less variable selling and administrative expenses (1,500 @ $180) Total contribution margin (270,000) $1,530,000 Less fixed expenses: Fixed factory overhead $1,500,000 Fixed selling and administrative expenses 190,000 (1,690,000) Net loss $ (160,000)

Step by Step Solution

3.30 Rating (147 Votes )

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts