Drago Company produces a line of brass-based products, one of which is a flow control valve (for

Question:

To address these problems, management is considering two decision alternatives. Alternative 1 would be to redesign the production layout process to secure both an increase in product quality and a decrease in manufacturing cycle time. Alternative 2 would be to lease (on a year-to-year basis) state-of-the-art inspection/testing equipment, which would allow the company to better and more accurately identify poor-quality output before that output leaves the plant.

Because of limitations on available capital to support additional investments (i.e., the capital spending budget for the year has already been constructed and is committed to other projects) and the possible need in the near future to redesign the flow-control valve, the company feels that it cannot pursue both of the above-referenced alternatives; it must choose one or the other.

The management accounting team for the company has gathered the following information that bears on the decision now facing management:

Decision Alternative 1: One-time engineering (process) redesign costs.............................$160,000

Decision Alternative 2: Annual leasing cost for inspection/testing equipment..................$100,000

The following fully allocated (i.e., variable plus fixed) costs are budgeted for quality-related activities for the coming year:

Cost to rework defective products.................................$100 per hour

Transportation costs (for obtaining repair parts).........$150 per delivery

Customer-support costs..................................................$ 50 per hour

Repair costs in the field (i.e., warranty costs)................$120 per hour

Estimates of the variable cost component of each of the above activity costs are as follows:

Estimated Variable Cost

Component (%)

Cost to rework defective products..............................................30

Transportation costs (for obtaining repair parts)......................60

Customer-support costs...............................................................50

Repair costs in the field (i.e., warranty costs).............................40

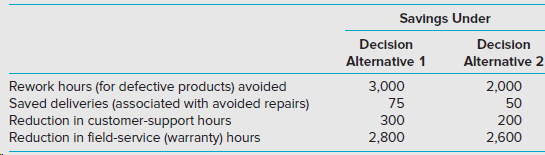

Estimated savings of quality-related activities under each decision alternative is:

The average contribution margin ratio for the product in question, over the past 3 years, and based only on direct labor and direct materials costs (i.e., quality-related savings are captured in their entirety above), has been 30%. Incremental sales (resulting from producing a better product) under each of the two decision alternatives are estimated as follows:

Decision Alternative 1 = $800,000

Decision Alternative 2 = $600,000

Required

1. What is the incremental cost (cash outlay) for each of the two decision alternatives?

2. What is the estimated year 1 financial benefit associated with each decision alternative? Round both answers to the nearest whole dollar.

3. What is the estimated year 1 net difference between the decision alternatives? That is, based on a 1-year financial analysis, which of the two decision alternatives is preferable (and by how much)? (Hint: Remember to factor in both costs and benefits, that is, both cash outflows and cash inflows.)

4. Comment on the results obtained in requirements 1, 2 and 3, particularly in terms of the COQ reporting model and any other pertinent concepts from Chapter 17.

5. What strategic considerations (including both financial and nonfinancial) bear upon the decision facing Drago?

Contribution MarginContribution margin is an important element of cost volume profit analysis that managers carry out to assess the maximum number of units that are required to be at the breakeven point. Contribution margin is the profit before fixed cost and taxes...

Step by Step Answer:

1 Incremental cost cash outlay for each decision alternative note data are given x no calculations needed Decision Alternative 1 Onetime Process Reengineering 160000 Decision Alternative 2 Annual Cost ...View the full answer

Cost Management A Strategic Emphasis

ISBN: 9781259917028

8th Edition

Authors: Edward Blocher, David F. Stout, Paul Juras, Steven Smith