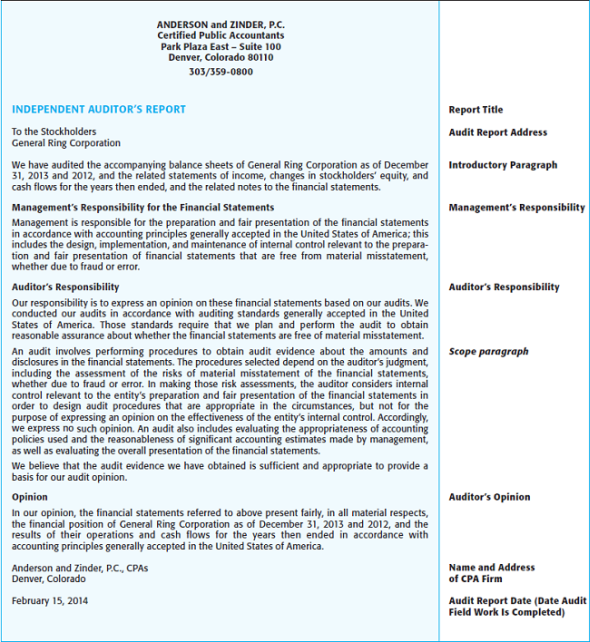

Audit Report

The audit report is issued by a certified public accountant who is appointed by the shareholders to provide assurance upon the truth and fairness of the financial statements prepared by the managers of the company. Audit report contains the auditor’s opinion on the truth and fairness of the financial statements of a company based on the examination of evidence on the subject matter.

Audit Opinion

The audit opinion is a part of the audit report and comes under the opinion paragraph in which auditor states the final wording about the truth and fairness of the company’s financial statements.

Audit Report or Opinion Types

The audit report and audit opinion are used alternatively as most of the audit report contents are same and only opinion paragraph differs based on one of the four types.

Unqualified Audit Opinion

First in which auditor provides assurance that the financial statements are giving a true and fair view in all material respects at the financial statement date. This report is called unqualified audit report.

Qualified Audit Opinion

The second type of audit opinion is called a qualified audit report that contains objections raised by auditor about the truth and fairness of the financial statements. This type of audit opinion may further be divided into two categories depending on the objections pointed out by the auditor. In the first type of qualified audit, opinion auditor highlights the material area that he is unsure about the truth and fairness of, based on the disagreement with the accounting standards. In the second type of qualified audit opinion, the auditor highlights the material area that he was unable to obtain sufficient audit evidence about the truth and fairness of.

Adverse Audit Opinion

Under this type of opinion, the auditor obtains substantial evidence that the figures reported in financial statements are in disagreement pervasively with the applicable accounting standards. The final wording for this type of opinion is that the financial statements do not give a true and fair view.

Disclaimer of Opinion

The last type of opinion is called the disclaimer of opinion. When auditors are unable to obtain sufficient appropriate audit evidence on pervasive areas of financial statements, they simply don’t provide any opinion on the financial statements.

Audit Report Example