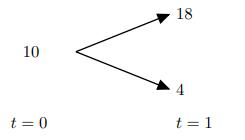

A nondividend-paying stock, S, is modeled by the binomial tree shown below. A European call option on

Question:

A nondividend-paying stock, S, is modeled by the binomial tree shown below.

A European call option on S expires at t = 1 with strike price K = 12.

Calculate the number of shares of stock in the replicating portfolio for this option.

(A) Less than 0.3

(B) At least 0.3, but less than 0.4

(C) At least 0.4, but less than 0.5

(D) At least 0.5, but less than 0.6

(E) At least 0.6

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

C Note that the payoff of the call is eit...View the full answer

Answered By

Susan Juma

I'm available and reachable 24/7. I have high experience in helping students with their assignments, proposals, and dissertations. Most importantly, I'm a professional accountant and I can handle all kinds of accounting and finance problems.

15+ Reviews

45+ Question Solved

Related Book For

Question Posted: