Assume the Black-Scholes framework. Consider a 1-year European contingent claim on a stock. You are given: (i)

Question:

Assume the Black-Scholes framework. Consider a 1-year European contingent claim on a stock. You are given:

(i) The time-0 stock price is 45.

(ii) The stock’s volatility is 25%.

(iii) The stock pays dividends continuously at a rate proportional to its price. The dividend yield is 3%.

(iv) The continuously compounded risk-free interest rate is 7%.

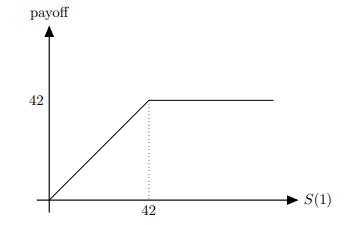

(v) The time-1 payoff of the contingent claim is as follows:

Calculate the time-0 contingent-claim elasticity.

(A) 0.24

(B) 0.29

(C) 0.34

(D) 0.39

(E) 0.44

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

C There are two ways to view the contingent claim We discuss both below As wi...View the full answer

Answered By

Rohail Amjad

Experienced Finance Guru have a full grip on various sectors, i.e Media, Insurance, Automobile, Rice and other Financial Services.

Have also served in Business Development Department as a Data Anlayst

32+ Reviews

83+ Question Solved

Related Book For

Question Posted: