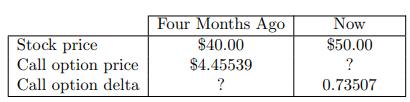

Assume the Black-Scholes framework. Four months ago, Eric bought 100 units of a one-year 45-strike European call

Question:

Assume the Black-Scholes framework. Four months ago, Eric bought 100 units of a one-year 45-strike European call option on a nondividend-paying stock. He immediately delta-hedged his position with shares of the stock, but has not ever re-balanced his portfolio. He now decides to close out all positions.

You are given:

(i)

(ii) The continuously compounded risk-free interest rate is 5%.

(iii) The volatility of the stock is less than 50%.

(a) Calculate the volatility of the stock.

(b) Calculate the four-month holding profit for Eric.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

For simplicity we let four months ago be time 0 and the current time be time 13 a We u...View the full answer

Answered By

Lisper Wanja

I am an experienced and highly motivated writer with a passion for the skills listed. I have a proven track record of my expertise and my aim is to deliver quality, well-detailed and plagiarism free projects. My genuine passion for writing combined with my ongoing professional development through school and research makes me an ideal candidate within for any assignment.

233+ Reviews

388+ Question Solved

Related Book For

Question Posted: