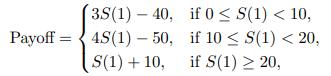

The payoff of a derivative contract maturing in one year is given by where S(1) is the

Question:

The payoff of a derivative contract maturing in one year is given by

where S(1) is the one-year price of the underlying nondividend-paying stock. You are given:

(i) The continuously compounded risk-free interest rate is 5%.

(ii) The current stock price is 15.

(iii) The price of a 10-strike 1-year call option is 5.52.

(iv) The price of a 20-strike 1-year call option is 0.38.

Calculate the fair price of the above derivative.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

To calculate the fair price of the derivative we need to find the expected value of its payof...View the full answer

Answered By

Cristine kanyaa

I possess exceptional research and essay writing skills. I have successfully completed over 5000 projects and the responses are positively overwhelming . I have experience in handling Coursework, Session Long Papers, Manuscripts, Term papers, & Presentations among others. I have access to both physical and online library. this makes me a suitable candidate to tutor clients as I have adequate materials to carry out intensive research.

1538+ Reviews

3254+ Question Solved

Related Book For

Question Posted: