(Repeat for puts) On December 1, the S&P 500 index (SPX) is trading at 1396.71. The prices...

Question:

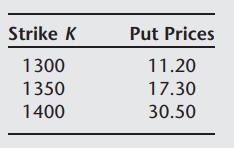

(Repeat for puts) On December 1, the S&P 500 index (SPX) is trading at 1396.71. The prices of put options on the index expiring on March 16 (i.e., a little over three months) are as follows:

Assuming the interest rate for that period is 4.88%, and the annual dividend rate on the SPX is 1.5%, compute the implied volatility for each of the options using the BlackScholes formula. Are these volatilities the same? Explain. Also, are these volatilities the same as that obtained from the previous question? Should they be? Explain.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Using the above inputs we get the following implied volatilities We can see that ...View the full answer

Answered By

Carly Cimino

As a tutor, my focus is to help communicate and break down difficult concepts in a way that allows students greater accessibility and comprehension to their course material. I love helping others develop a sense of personal confidence and curiosity, and I'm looking forward to the chance to interact and work with you professionally and better your academic grades.

12+ Reviews

21+ Question Solved

Related Book For

Question Posted: