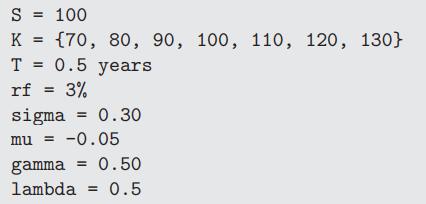

Question: (Requires Writing Code) Using the following parameters, price call options for a range of seven strike prices with the Merton jump model. Now with the

(Requires Writing Code) Using the following parameters, price call options for a range of seven strike prices with the Merton jump model.

Now with the seven option prices (one for each strike price), find out what the implied volatility is in the Black-Scholes model. You will need to write program code to find the implied volatility.

Once you have the seven corresponding implied volatilities, plot them against the strike prices. What shape does your options smile have?

Step by Step Solution

★★★★★

3.53 Rating (163 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

The Merton 1976 model needs to be programmed to ... View full answer

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock