You are the asset manager for an international fund. Suppose you enter into an unhedged currency swap

Question:

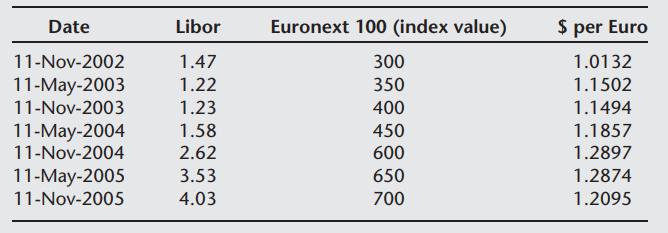

You are the asset manager for an international fund. Suppose you enter into an unhedged currency swap in which you receive the return on the Euronext 100 index and pay the Libor rate. The swap is on a half yearly basis for three years and is unhedged, i.e., payments will reflect current exchange rates. The following is the experience of the

Assume that the convention on the interest rates is Actual/360 and the swap has a variable notional principal. Prepare a table showing the payments and receipts on this swap. The notional principal at inception is $100,000.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

The following table computes the net dollar values of the payments on the swap Date Libor Euronext 1...View the full answer

Answered By

Joseph Ogoma

I have been working as a tutor for the last five years. I always help students to learn and understand concepts that appears challenging to them. I am always available 24/7 and I am a flexible person with the ability to handle a wide range of subjects.

1+ Reviews

10+ Question Solved

Related Book For

Question Posted: