Question: Consider the following model: R t = β 0 + β 1 M t + β 2 Y t + u 1t Y t =

Rt = β0 + β1Mt + β2Yt + u1t

Yt = α0 + α1Rt + α2 It + u2t

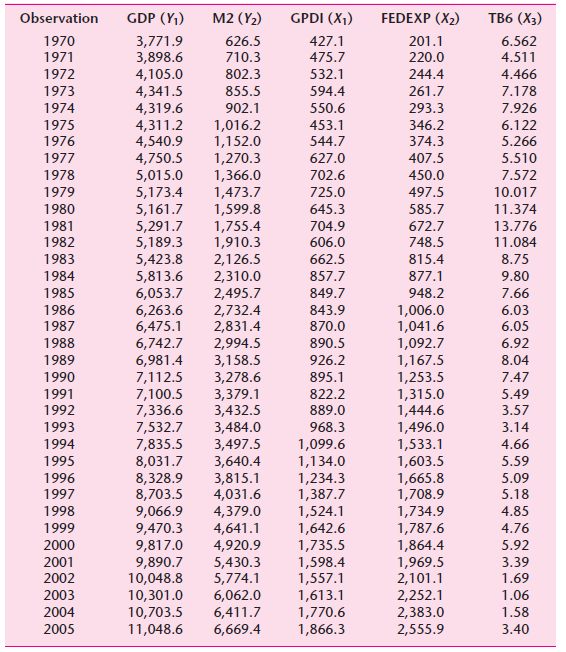

where the variables are as defined in Exercise 20.8. Treating I (domestic investment) and M exogenously, determine the identification of the system. Using the data given in the following table, estimate the parameters of the identified equation(s).

GDP (Y1) 6 (X) Observation M2 (Y2) GPDI (X1) FEDEXP (X2) 3,771.9 3,898.6 4,105.0 4,341.5 4,319.6 4,311.2 4,540.9 4,750.5 5,015.0 5,173.4 5,161.7 5,291.7 5,189.3 5,423.8 5,813.6 6,053.7 6,263.6 6,475.1 6,742.7 6,981.4 7,112.5 7,100.5 7,336.6 7,532.7 7,835.5 8,031.7 8,328.9 8,703.5 9,066.9 9,470.3 9,817.0 9,890.7 10,048.8 10,301.0 10,703.5 11,048.6 427.1 475.7 201.1 1970 626.5 6.562 1971 710.3 220.0 4.511 1972 802.3 532.1 244.4 4.466 1973 7.178 855.5 594.4 261.7 1974 902.1 550.6 293.3 7.926 346.2 374.3 1,016.2 1,152.0 1,270.3 1,366.0 1,473.7 1,599.8 1,755.4 1,910.3 2,126.5 2,310.0 2,495.7 2,732.4 2,831.4 2,994.5 3,158.5 3,278.6 3,379.1 3,432.5 3,484.0 3,497.5 3,640.4 3,815.1 4,031.6 4,379.0 4,641.1 4,920.9 5,430.3 5,774.1 6,062.0 6,411.7 6,669.4 1975 453.1 6.122 1976 5.266 544.7 1977 627.0 407.5 5.510 702.6 1978 450.0 7.572 1979 725.0 497.5 10.017 1980 645.3 585.7 11.374 1981 704.9 672.7 13.776 1982 606.0 748.5 11.084 1983 662.5 815.4 8.75 877.1 1984 857.7 9.80 7.66 1985 849.7 948.2 1986 843.9 1,006.0 1,041.6 1,092.7 1,167.5 1,253.5 1,315.0 1,444.6 1,496.0 1,533.1 1,603.5 1,665.8 1,708.9 1,734.9 1,787.6 1,864.4 1,969.5 2,101.1 2,252.1 2,383.0 2,555.9 6.03 1987 870.0 6.05 890.5 1988 6.92 1989 926.2 8.04 1990 895.1 7.47 1991 822.2 5.49 1992 889.0 3.57 1993 968.3 3.14 1994 1,099.6 1,134.0 1,234.3 1,387.7 1,524.1 1,642.6 1,735.5 1,598.4 1,557.1 1,613.1 1,770.6 1,866.3 4.66 1995 5.59 1996 5.09 1997 5.18 1998 4.85 1999 4.76 2000 5.92 2001 3.39 2002 1.69 2003 1.06 2004 1.58 2005 3.40

Step by Step Solution

3.33 Rating (153 Votes )

There are 3 Steps involved in it

Here both the equations are exactly identified One can us... View full answer

Get step-by-step solutions from verified subject matter experts

Document Format (2 attachments)

1529_605d88e1dc179_666531.pdf

180 KBs PDF File

1529_605d88e1dc179_666531.docx

120 KBs Word File