Question: Following Friedmans permanent income hypothesis, we may write Y i = α + βX i where Y i = permanent consumption expenditure and X i

Following Friedman€™s permanent income hypothesis, we may write

Yˆ—i = α + βXˆ—i

where Yˆ—i = €œpermanent€ consumption expenditure and Xˆ—i = €œpermanent€ income. Instead of observing the €œpermanent€ variables, we observe

Yi = Y*i + ui

Xi = X*i + vi

where Yi and Xi are the quantities that can be observed or measured and where ui and vi are measurement errors in Yˆ— and Xˆ—, respectively. Using the observable quantities, we can write the consumption function as

Yi = α + β(Xi €“ vi) + ui

= α + βXi + (ui €“ βvi)

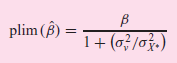

Assuming that (1) I(ui) = E(vi) = 0, (2) var (ui) = σ2u and var (vi) = σ2v, (3) cov (Y*i, ui) = 0, cov (X*i, vi) = 0, and (4) cov (ui, Xi*) = cov (vi, Y*i) = cov (ui, vi) = 0, show that in large samples β estimated from Eq. (2) can be expressed as

a. What can you say about the nature of the bias in β̂?

b. If the sample size increases indefinitely, will the estimated β tend toward equality with the true β?

plim () = 1+ (0} /of.) 1+ (a/a}.)

Step by Step Solution

3.42 Rating (155 Votes )

There are 3 Steps involved in it

a For Eq 2 we obtain from OLS Note For convenience we have omitted the ob... View full answer

Get step-by-step solutions from verified subject matter experts

Document Format (2 attachments)

1529_605d88e1d609c_665987.pdf

180 KBs PDF File

1529_605d88e1d609c_665987.docx

120 KBs Word File