Bart, Ps sole shareholder, creates P on January 1 of Year 1. P purchases all of S1s

Question:

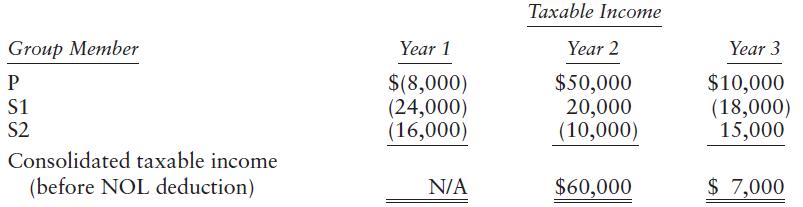

Bart, P’s sole shareholder, creates P on January 1 of Year 1. P purchases all of S1’s and S2’s stock on September 1 of Year 1, after both corporations are in operation for about six months. P, S1, and S2 Corporations comprise the P-S1-S2 affiliated group and file separate tax returns for Year 1. The P-S1-S2 affiliated group then elects to file consolidated tax returns starting in Year 2. The group reports the following results:

Ignore the Sec. 382 loss limitation that might apply to the acquisitions of S1 and S2, assume that P’s purchase of S1 and S2 does not qualify as a reverse acquisition, and assume that Year 1 is a post-2017 year.

a. What is Year 2 consolidated taxable income?

b. What is Year 3 consolidated taxable income?

c. What NOL carryovers are available in Year 4?

d. How would your answer to Parts a through c change if Bart instead created P, S1, and S2 as an affiliated group on January 1 of Year 1?

Step by Step Answer:

a Year 2 consolidated taxable income is 32000 The group must use S2s 10000 loss to offset Ps and S1s Year 2 taxable incomes Ps year 1 NOL is not a SRL...View the full answer

Federal Taxation 2021 Corporations, Partnerships, Estates & Trusts

ISBN: 9780135919460

34th Edition

Authors: Timothy J. Rupert, Kenneth E. Anderson, David S. Hulse